4 July 2025

1300 794 893

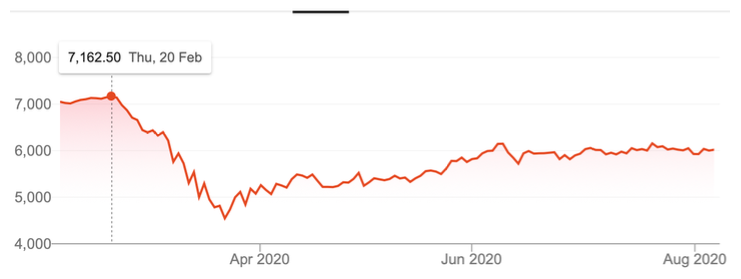

One of the hardest commodities to ‘sell’ is common sense! And when a person’s nest egg or super is involved, it’s even harder. After years of financial advice and financial education, I know using common-sense is the best approach to building wealth. But try telling that to the inexperienced and the nervous that it’s OK to lose capital for a certain period, when all they see is their hard-earned income disappear. This happened between February 20 and March 23 this year with the Coronavirus crash. I’m talking a 36.5% loss of capital, which has comeback but it’s still down 19% from before the fall.

S&P/ASX 200

So, if you retired late last year and had $1 million in your super fund, you could now have a little over $800,000 but you hear or read me saying that it’s OK. Before you call me an idiot and go back to reading stuff about the Coronavirus, high fashion and footie scores, give me a chance to explain.

In trying to preserve capital and make money at the same time, we put our clients into mixed portfolios of assets, with different exposures to growth assets (like stocks) and more defensive assets (like bond funds, hybrids, term deposits and so on). However, apart from term deposits, the value of these ‘defensive’ assets can be risky. And because term deposits were paying less than 1% before the Coronavirus crash, clients had to be more exposed to riskier defensive assets.

And they didn’t like it when their bond fund that had been paying 5% a year saw its unit price fall because it was listed on the stock market. Markets can do crazy things. We see this all the time when we see funds that have a real value or NTA (net tangible asset value) that is greater than what the market is prepared to pay for it.

So in many ways, unless you’re in term deposits, you are stuck with what sometimes mad, bad and dangerous financial markets want to do. And these suckers can play havoc with good quality assets and therefore your money. But it’s only a time thing, so what you have to learn to accept is that sometimes you’ll be relatively poorer for a time but then you’ll get richer, until the next crash comes along.

That takes guts and an understanding of what you lose when you want to avoid losing capital.

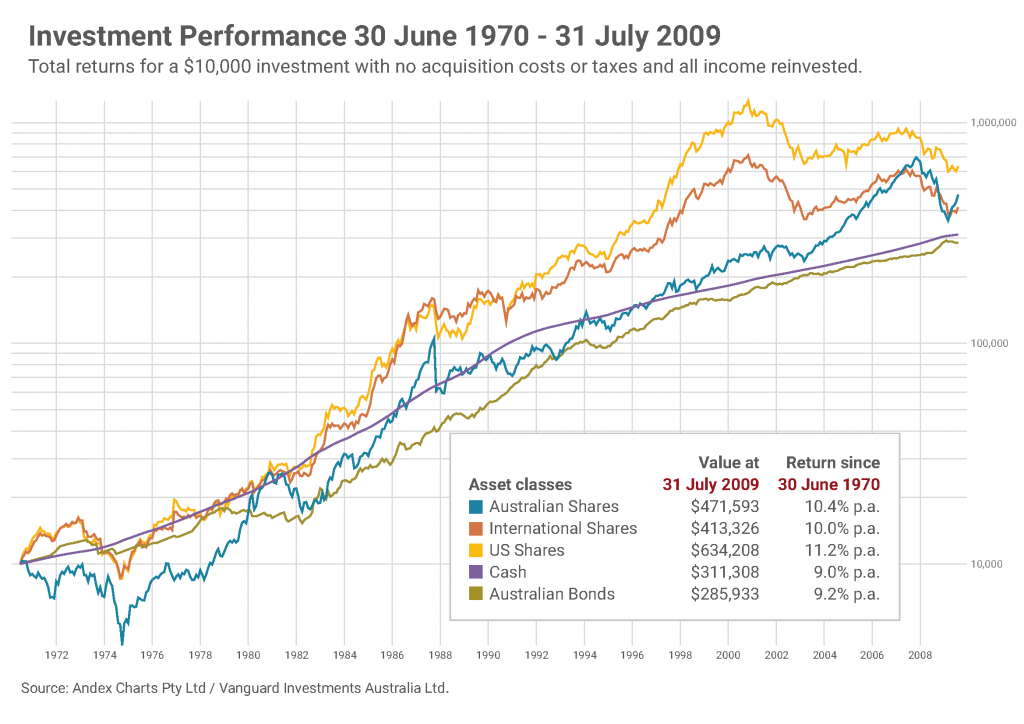

Before I show you that, have a look at what happens to your capital when you retire and you’re fully invested in the stock market.

The blue line shows how $10,000 of capital invested in 1970 went up and down over 30 years to 2009 and grew to $471,593 — that was one year after the stock market crashed 50% with the GFC.

In a perfect world, a great adviser would be able to get you out ahead of a crash and then get you back in at the bottom of the market. But let me tell you with all honesty, that’s easier said than done.

Sure, there are plenty of exotic strategies that can minimise your fall and maximise your rise but they all involve gambling, timing and hoping that someone like Donald Trump doesn’t create a trade war.

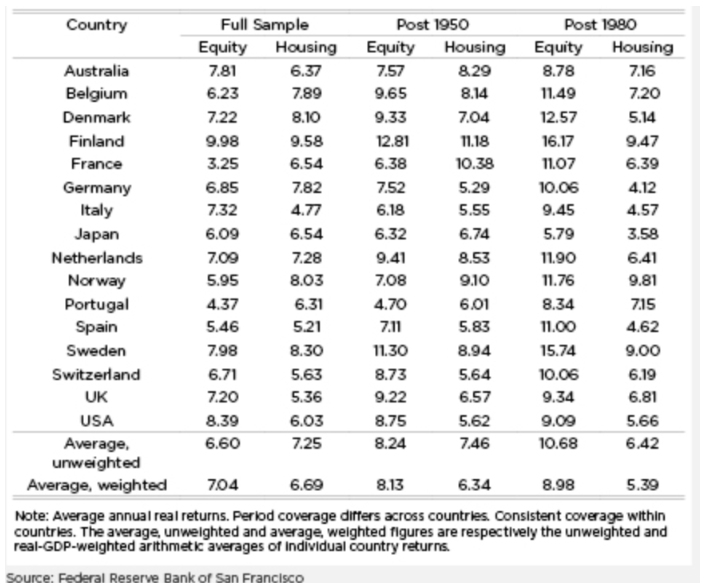

A better strategy is to explain to wealth-builders that stock markets return around 10% a year (including franking credits) over a 10-year period. And about half of that comes from dividends and franking credits for us here in Australia, where we pocket those tax giveaways. The Federal Reseve Bank of San Francisco produced a paper entitled: The Rate of Return on Everything and you can see what equities (shares) and housing have delivered over time.

The Federal Reseve Bank of San Francisco produced a paper entitled: The Rate of Return on Everything and you can see what equities (shares) and housing have delivered over time.

If you could get someone in Australia to commit to Australia’s best companies with at least 30 stocks in the portfolio and you biased them towards good dividend-payers, then you could actually get a stream of income around 5% on average.

And even though dividends will be reduced over the next two years, they will make a comeback as the economy improves. Those investors who play the dividend game have a game plan that works.

Consider this example. Someone retires with $2 million in their share super fund (with their partner). By the way, two teachers who were in teaching from 1975 could be in such a situation! They want $120,000 to live off, which means they need a 6% return. Generally, along with franking credits, that should be easily achieved and if a strategy is put in place to siphon off income when the stock market has ripper years, then a buffer could be created to help you see that $120,000 when dividends are beaten up. A buffer of say $80,000 might be needed to ensure that in bad years for dividends, the buffer can kick in money to top up what’s needed for a $120,000 life a year.

Ultimately, it’s the income that has to be managed. You’d only have to do some juggling in bad years when recessions and pandemics upset the apple cart. By playing too much defence, you bring a 10% return from stocks down to say 6%, which means your money doubles every 12 years. If you leave yourself exposed to the stock market, your money would double every 7 years.

That’s a big difference! The defensive stance really undermines your potential to grow your wealth in retirement. With us increasingly living longer, we need to play a more aggressive game. That’s why I prefer quality companies that are important for driving the stock market and have a great history of paying dividends.

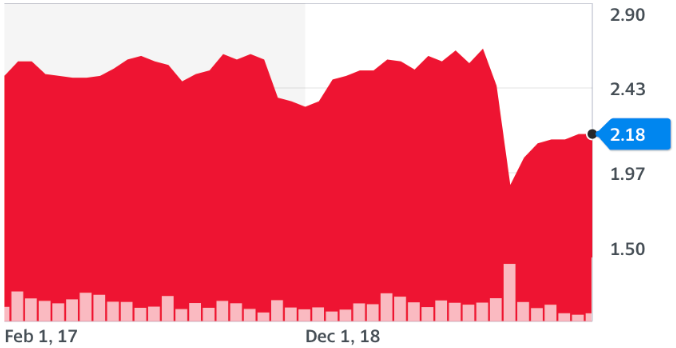

Take a look at my Switzer Dividend Growth Fund, which was listed in late February 2017.

SWTZ

It wasn’t designed to shoot the lights out but supply a reliable income flow as term deposit interest rates fell and too many self-funded retirees were too exposed to five quality dividend paying stocks — the big four banks and Telstra. We rope these together into what we call the Mum & Dad Index.

I recently asked the fund manager Contango Asset Management (that manages SWTZ) to work out what dividend stream it has paid over the time it has been listed. SWTZ listed at $2.50 and crawled to $2.70 (with Donald Trump’s trade war and the Hayne Royal Commission no help to the capital growth of a fund with exposure to financial stocks among its 30-odd collection in the fund).

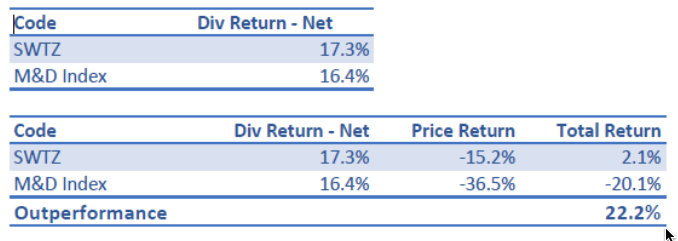

This is how we did over that time compared to the Mum & Dad Index:

You’ll see the the big banks plus Telstra did OK, delivering 16.4% over that time. But via diversification and investing in more dividend-payers than just five companies, we paid out 17.3% since listing.

Meanwhile, our capital loss thanks to Donald + Hayne + COVID-19 was 15.2% compared to 36.5% for the Mum & Dad stocks. So we’ve done what we set out to do. I know the total return for SWTZ is only plus 2.1% but it’s better than the negative 20.1% for the Mum & Dad crew.

But the more important point is that for the three years or so, SWTZ delivered net dividend income of 17.3%, while the Mum & Dad stocks returned 16.4%. That leaves out franking, so it would be more if we add in the tax ‘gift’ from the Government.

That’s a little less than 6% income a year for SWTZ and a little more than 5% for Mums & Dads, which considering the trying times makes a good case for chasing dividends as a core strategy.

Over coming years, capital gain will kick in. And when that happens, some shares can be sold and a buffer can be built up. If you go back to my second chart (which showed how the Australian stock market trends higher over time) as long as you are set to receive a good flow of dividends in great quality companies you don’t have to worry about what the crazy stock market decides to do to your capital or nest egg in the short term.

When you can’t get a decent return out of safe term deposits, it’s best to be diversified into a large range of quality companies/assets that pay reliable income.

SWTZ won’t do as well for income in the year ahead, as banks reduce or kill their dividends. But that’s why my fund has 38 stocks in it. Most of these companies won’t be forced to cut dividends because they’re not a part of the Government’s rescue strategy. This means that unlike what they’re telling the banks to do, APRA won’t be ordering most of the companies in my fund to cut their dividends! I love capital gain but I know it’s not reliable year to year, while dividends are much more dependable. That said, over a decade, capital gain historically is a pretty good giver.

Click here to take a free 21-day trial to the Switzer Report, a leading investment newsletter and website for self-directed investors.