11 July 2025

1300 794 893

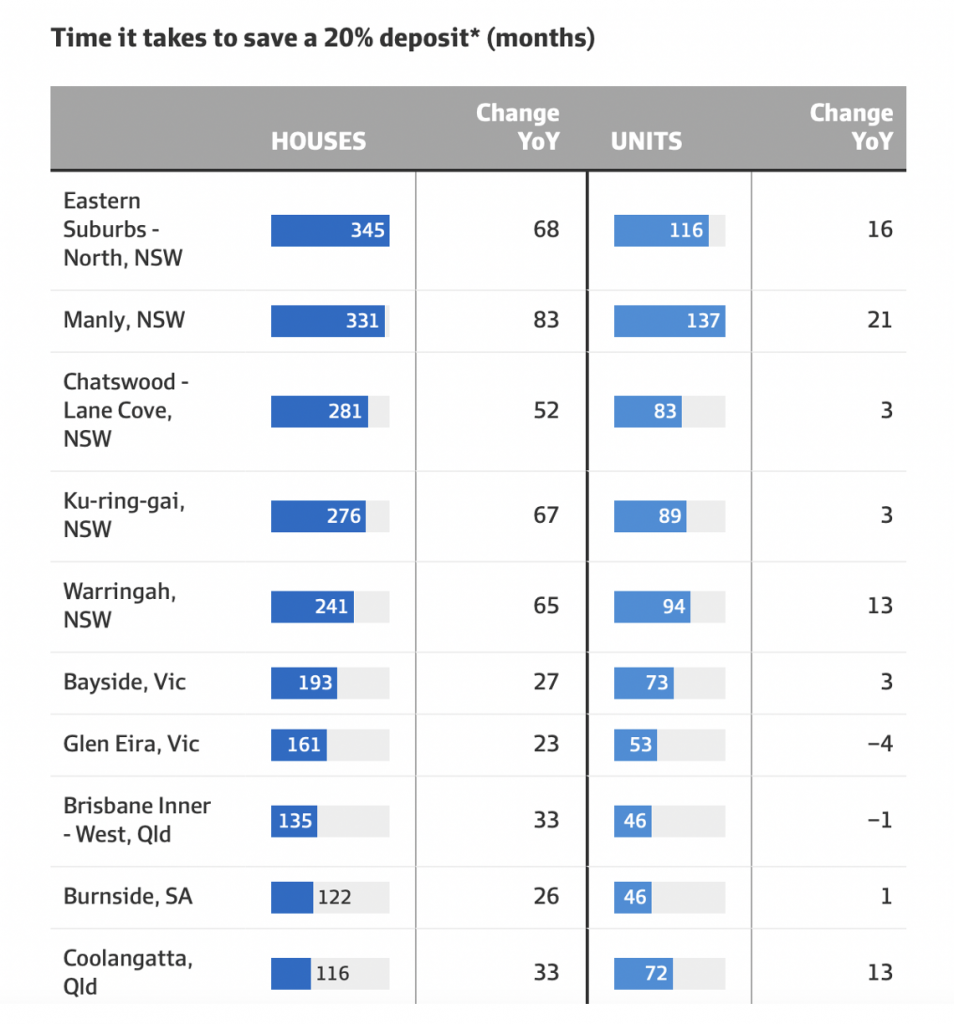

The one unquestioned fear most parents might have is about how their kids will ever be able to afford to buy a home and live near their family. And Domain’s annual First Home Buyer report actually shows how many months a couple needs to save up for a deposit to buy an entry-level property within our capital cities.

It's not great reading for young couples and makes it essential that they learn to use their super to make it happen quicker. And if the polls are right, then future Labor Ministers — Jason Clare on housing, Matt Thistlethwaite on super and would-be Treasurer Jim Chalmers (with whom I had lunch yesterday at an ACCI/Business Sydney event) really need to think outside the square to help Aussies access their bricks and mortar dream.

The numbers above on the months of saving that a couple needs to put in show the problem in stark reality.

For a couple to save to live in the Warringah area in Sydney, we’re talking 241 months of saving; Glen Eira in Victoria, 161 months; and Coolangatta in Queensland, 116 months of saving.

For Sydney’s East, forget it, where it takes 116 months for a home unit or 9.66 years, and for a house 28.75 years! Did I say forget it, unless you come from a rich family, you work for an investment bank, you start a tech company or have a great credit rating at the bank of mum and dad.

The reason I wanted to do this story was that I assumed that the method used to work out how long it takes to save for a home actually makes the story even scarier than it has to be. And I was right in assuming that the report was based on what most couples do to save the deposit, which is what has to change.

The report is findable here and outlines the method for arriving at these numbers: “The time required to save a deposit is based on a dual income, with each person saving 20 per cent of post-tax income on a monthly basis that is deposited in a standard online savings account (interest earned is taxed at the individuals’ tax rate).

But if a couple accesses help from the Federal government, then these numbers can be substantially reduced.

First, there is the First Home Loan Deposit Scheme (FHLDS), which allows a first-home buyer to secure a home loan with as little as a 5% deposit, without incurring the added cost of mortgage lender’s insurance. The impact of this was explained by the report: “Utilising this scheme supercharges the speed to market, reducing the savings time to less than two years for an entry-priced house across all capital cities, with Perth recording the quickest time to save at only 10 months.”

Second, the First Home Super Saver Scheme (FHSSS) allows individuals to save $30,000 under the scheme, or $60,000 for a couple (this is set to increase in the next financial year). This scheme doesn’t allow couples to access their compulsory 10% super payments but if they use salary sacrifice, they can save up to $27,500 minus their boss’s compulsory super payment.

So if the boss puts $10,000 into super, an individual could throw in $17,500 a year, which could be withdrawn for a deposit. This would have the dual benefits of a 15% tax on that income and it would grow faster, as super returns are generally better than bank deposits.

“On average across the cities, 2 years and 10 months were shaved from a house deposit saving time, and 2 years and 9 months for units,” the report revealed.

Both these schemes (i.e the First Home Loan Deposit Scheme and the First Home Super Saver Scheme) reduce the saving time by just under five years or 60 months.

Future governments need to increase the supply of affordable housing, reduce the taxes on developers actually building homes and allow greater access to super to help reduce the time it takes a young couple to get the deposit together for a home.

Rules could be applied e.g. if the house is sold and no new one is bought, the money that left super to bankroll the deposit should be recontributed into super.

The question is: could a Labor government talk their friends at industry super funds (which were a smart product of the union movement) to part with money from members of the funds to help those members buy a home?

Of course, if ScoMo shocks us again and wins in May, his team needs to not only get more homes built over the next three years, they also need to improve their saving schemes to reduce the years needed to get a young couple into a home ASAP.

And young people need to be more interested in money such that they access and use these saving schemes. I bet a hell of a lot of young people don’t know about and/or use these schemes.

The money education process of all Aussies needs to be lifted.