2 July 2025

1300 794 893

Almost every small-cap investor knows the pain of investing in the next big thing, only to find their stock remains resolutely that: a small cap.

Or even worse, the company ceases to be altogether, providing fodder for the ever-booming insolvency industry.

Even more annoying is the regret of investors losing patience with a serial plodder, only for the company to come good after they’ve sold out.

So in this June tax selling period, we highlight three industrial stalwarts that have long lost the patience of investors but look to be coming good.

Don’t bail on them just yet.

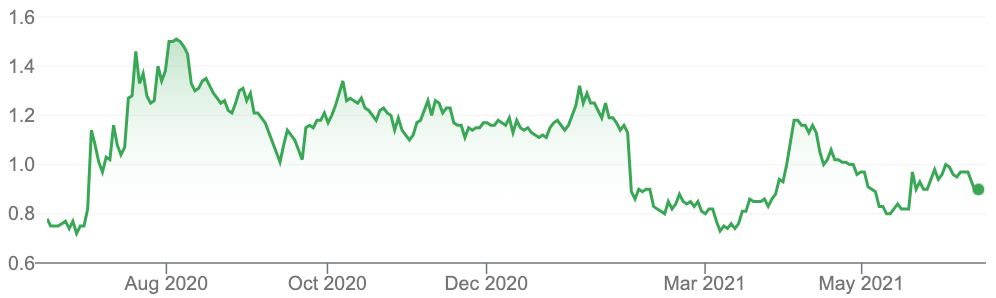

1. TZ Limited (TZL)

A leader in self-service technology, TZ should have surfed the boom in ecommerce but the company became enveloped in corporate dramas after it listed in 1999.

Notably, a $6.25 million fraud carried out between 2006 and 2008 resulted in the jailing of two directors, Andrew Sigalla and John Falconer.

The company’s profile was elevated after entrepreneur Mark Bouris – then host of The Apprentice and founder of Wizard home Loans – joined as executive chair in mid 2009 (he departed in 2017).

Nowadays the joint is run by entrepreneur Scott Beeton, whose first day involved sending everyone home on the first day of the Covid lockdowns in March last year.

Beeton also radically cut costs (including executive salaries) and rejigged the products and sales channels.

“We overpromised and underdelivered for too long,” he says. “We overspent on our tech to get to where we are.”

TZ’s core product is a lightweight ‘smart’ lock product that enables remote monitoring. The company also makes money out of the subscription software that enables the surveillance, as well as hosting and the physical lockers themselves.

Vaunted applications are larger cabinets for items like scooters and gun cabinets for police departments and the military.

TZ’s clients include Google, Amazon, Microsoft, Singapore Post, well-known US universities and Westpac (which has 26,000 corporate day lockers).

“Not many Australian small caps will service the biggest tech, postal companies and banks in the world,” Beeton says.

In a May 28 update, management said new contracts would take TZ’s recurring revenue base to $3 million in the 2021-22 year. “My goal is to get that to $10 million by 2022-23,” Beeton says.

The company cites $US8.6 million ($11.1m) of additional US orders, a “significant share” of which will be recognised in the 2021-22 year

Locally, TZ expects to sign contracts for $2 million of gear to fit out 6,000 lockers, with $150,000 a year of annuity revenue over three years.

In late May, TZ said it had secured a $1 million upgrade services agreement with global logistics company DSV South Africa. The company has previously supplied $3 million of lockers to the global logistics company.

In April this year, the company bolstered its anaemic financial position with a $2.58 million placement and launched a $7.06m one-for-two rights issue, both at 12 cents apiece. The latter is expected to attract subscriptions of $4.5-5m, with management confident of placing the shortfall.

TZ’s prospects have been weighed down by an $11.75 million debt facility with its biggest shareholder First Samuel, repayable at the end of July.

Most of the proceeds from the raising will be used to repay the debt, with First Samuel also agreeing to take up its $1.25 million rights allocation.

TZ shares traded at 3 cents a year ago. In an unexplained blip they jumped from 17 cents to 36 cents on April 21.

With a repaired balance sheet, TZ can lock in a brighter future.

TZ Limited (TZL)

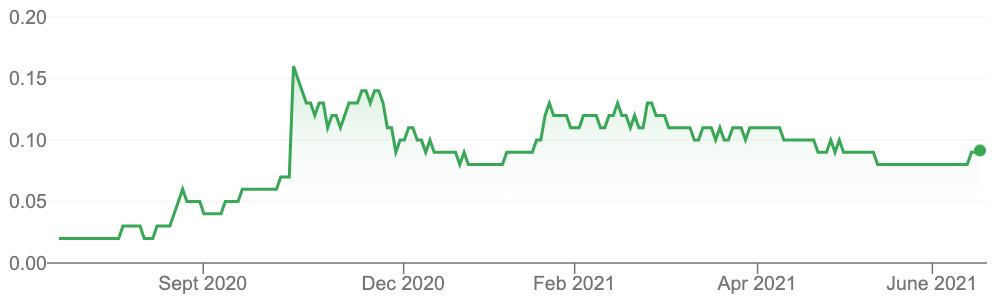

2. Orbital Corporation (OEC)

Having been listed on the ASX for close to four decades, the fuel-delivery technology group looked to have run out of juice well before the pit stop but its engine is still running.

The Perth-based Orbital has had numerous iterations over the years and it certainly now has nothing to do with the orbital engine made famous by its founder Ralph Sarich.

After being snubbed by the car industry, Orbital turned to the burgeoning market for military drones, or tactical military unmanned aerial vehicles (TUAVs).

Orbital’s injection method keeps the fuel and oil separate, with a fine mist sprayed directly into the combustion chamber. The Orbital-powered drones can stay in the air longer – up to 20 hours – and require less maintenance.

As is always the case with selling to the military, suppliers need an ‘in’ with the military bigwigs.

Orbital’s production is underpinned by a deal with drone maker Insitu, a division of Boeing. It also has a less formative development and supply agreement with Lycoming (an arm of Textron Systems) and a research and development contract with Northrop Grumman to build a hybrid propulsion system.

Worth up to $350 million, the five-year Insitu agreement involves manufacturing and servicing five different motors, three of them Orbital designed and two of them Insitu-designed.

Orbital chalked up revenue of $19 million in the first half to December 2020, with an operating profit of $600,000 compared to a previous $1.9m loss.

Management has guided to turnover of $30-40 million for the full year, compared with $34 million previously. This flat expectation stems from Boeing tapering back orders, presumably temporarily, because of “prevailing market conditions.”

Orbital shares have enjoyed a strong run since early March. As with the drones, profits need to fly stronger for longer before long-standing investors can be convinced the epic 36 year journey has been worthwhile.

Orbital Corporation (OEC)

3. Funtastic (FUN)

In June 23, Funtastic holders will file into their (virtual) EGM to vote on changing the serial laggard’s moniker to Toys’R’Us ANZ Ltd.

A name switcheroo has been a measure of last resort for many a straggler and, in isolation, tends not to help (just ask shareholders of One Steel/Arrium).

But in Funtastic’s case, the proposed new identity stems from last year’s reverse takeover of Louis Mittoni’s The Hobby Warehouse Group, which provides a firmer online presence via the local rights to the Toys’R’Us name, as well as the newer Babies’R’Us.

Funtastic also acquires the Mittoni Ltd distribution business, which imports consoles and other e-gaming paraphernalia.

Funded by a $33 million placement, the deal saw Mr Mittoni installed as CEO and new ways prevailing.

In the past, Funtastic has failed to turn a quid despite holding the rights to kiddie favourites including Lego, Bob the Builder, Thomas the Tank Engine and Pillow Pets.

With the Hobby Warehouse deal completed in late November 2020, Funtastic reported a $1.01 million profit for the half year to January 2021, compared with a $4.2m loss previously.

Revenue gained 15% to $16.2 million but if the acquired business had been part of the company for the whole period, turnover would have been $31m despite a falling contribution from Funtastic’s legacy business-to-business arm.

Funtastic (FUN)

tim@independentresearch.com.au

Disclaimer: The companies covered in this article (unless disclosed) are not current clients of Independent Investment Research (IIR). Under no circumstances have there been any inducements or like made by the company mentioned to either IIR or the author. The views here are independent and have no nexus to IIR’s core research offering. The views here are not recommendations and should not be considered as general advice in terms of stock recommendations in the ordinary sense.