US data

was mixed. ISM business conditions indexes fell back in April, but they remain

very strong and jobless claims fell sharply. Against this though payroll jobs

rose by a far less than expected 266,000 in April with unemployment rising

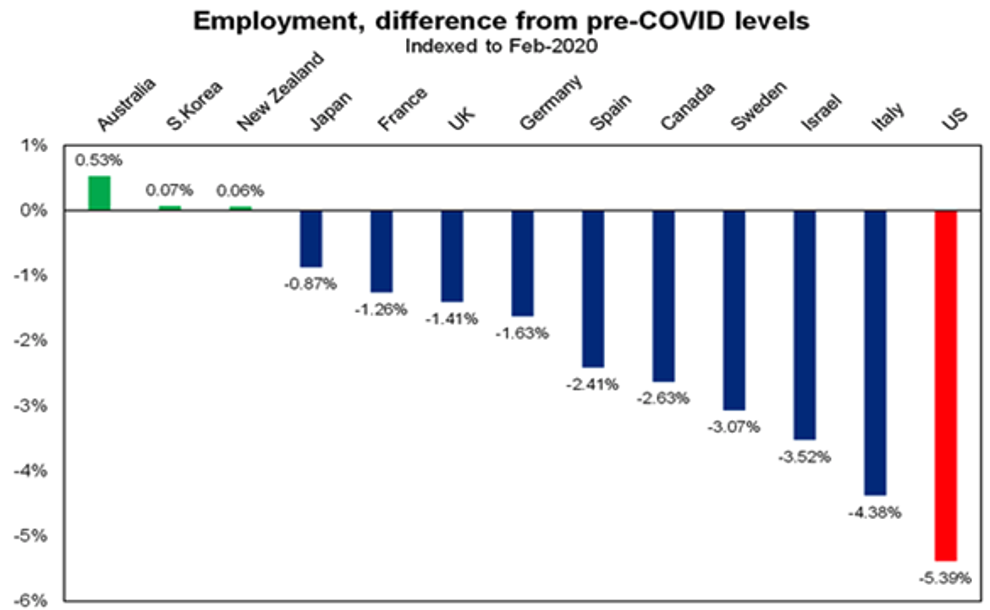

slightly to 6.1%. Only 62% of US payroll jobs lost in the pandemic have been

recovered leaving employment in the US 5.3% below its pre pandemic level which

is a far worse outcome than seen in many comparable countries. See the next

chart.

Source: Bloomberg, AMP Capital

April’s disappointing payroll result could mean

that:

The US economy is actually weaker than expected – but this is unlikely as virtually all other data is very strong;

Employers can’t find suitable workers with temporarily enhanced unemployment benefits of $300 a week keeping some at home because they will get less working in some jobs – but then employment in leisure and hospitality where average pay is the lowest rose by 331,000 with other higher paying sectors falling. And participation actually rose in April which is why unemployment rose.

It’s just statistical noise – it’s common to see odd jobs reports every so often.

Given all this and that its dangerous to read too

much into one month’s data I think it’s probably best to not read too much into

the April jobs data. In the meantime, it will serve to keep the Fed

dovish.

Looking more broadly at the US, strong demand at

the same time as higher raw material costs and supply chain bottlenecks are

continuing to boost inflation pressures though with the ISM prices paid indexes

at their highest since 2008. While Treasury Secretary Yellen stated the obvious

in saying interest rates may have to rise to prevent overheating, she

subsequently clarified that this was not a forecast and numerous Fed officials

downplayed the risk of overheating and indicated that there is a long way to go

to meet the Fed’s goals.

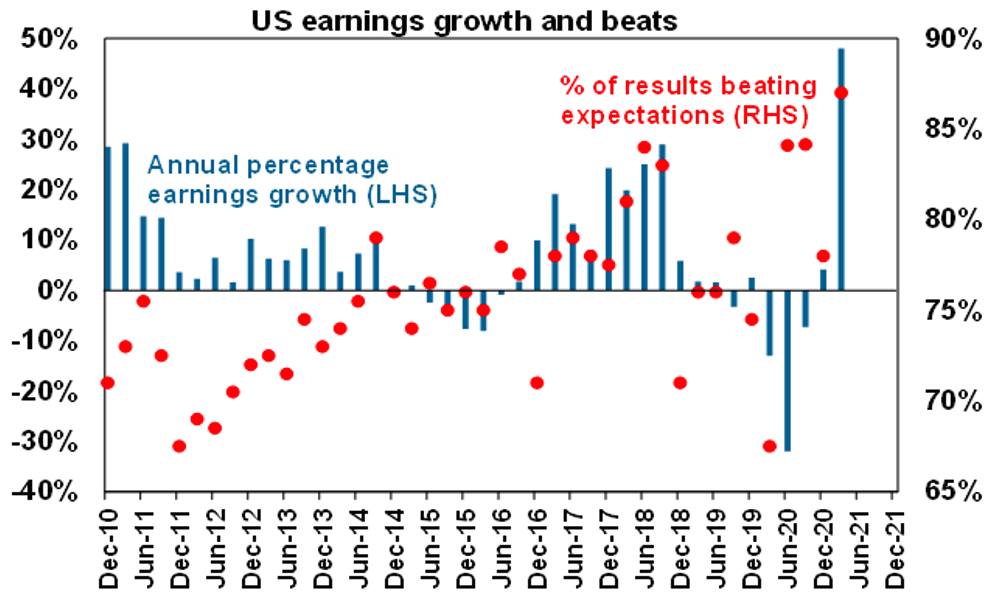

The US

March quarter earnings reporting season has remained very strong and is now nearly

90% complete. 87% of companies have beaten earnings expectations by an average

+23% and 71% have beaten revenue expectations. Consensus earnings expectations

for the quarter have now risen to +48% year on year, from +21% three weeks ago.

Tech sector earnings are up 43%, but consumer discretionary is up 186%,

financials are up 137% and materials are up 61%.

Source: Bloomberg, AMP Capital

Australian economic events and implications

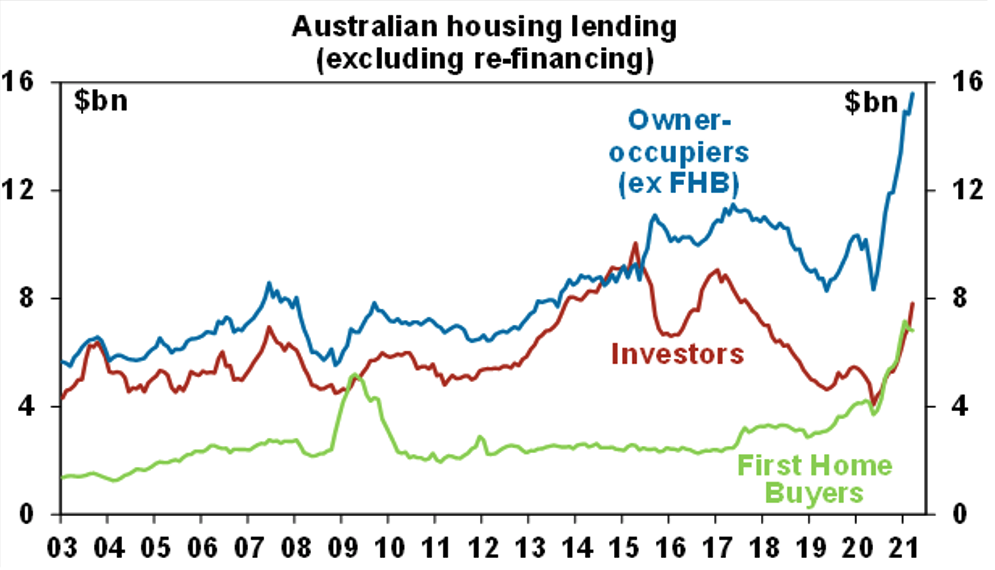

Australian data remained strong with booming home

prices, housing finance and approvals along with very strong PMIs, surging job

ads, a sharp jump in vehicle sales and the MI Inflation Gauge showing a pick-up

in inflation pressure.

Source: RBA, AMP Capital

While home price growth slowed a bit in April it remains very strong with record high housing finance commitments and still very strong auction clearance rates on the back of ultra-low mortgage rates, government incentives and economic recovery pointing to further gains ahead. More Government incentives in the Budget to enable more home buyers to get in with lower deposits will help maintain upwards pressure on prices and result in higher debt levels.

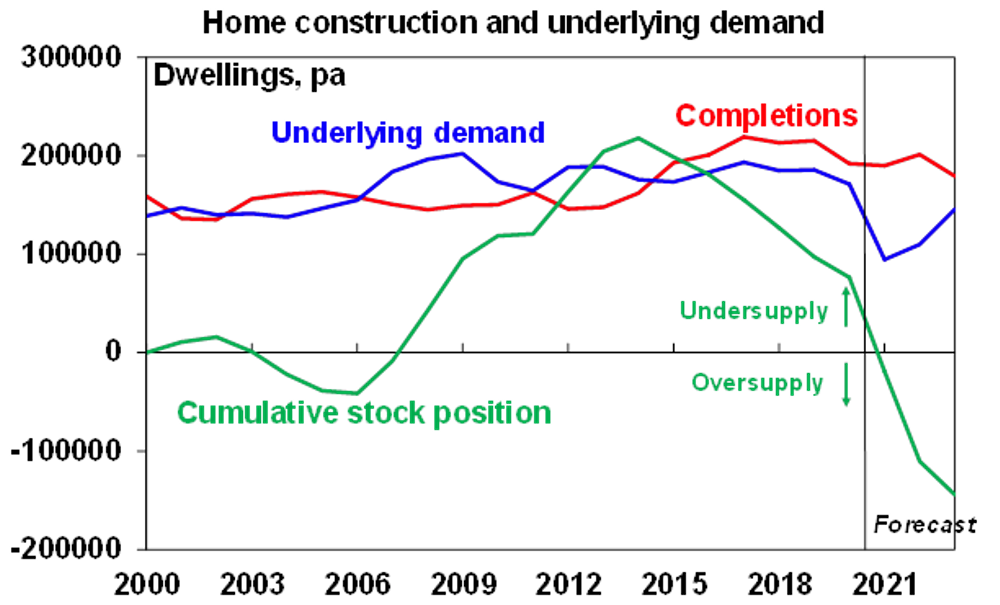

However, the pace of home price gains is likely to

slow from 15% this year to 5% next year and then to a likely modest fall in

prices in 2023 as fixed mortgage rates head higher, the RBA and APRA move

to tighten lending standards sometime in the next six months and the surge in

building approvals at a time of collapsed population growth leads over the next

couple of years to an oversupply of property relative to underlying

demand.

Source: ABS, AMP Capital

What to watch over the next week?

In Australia, the main focus will be on the Federal

Budget (Tuesday) which is expected to provide further stimulus to help boost

the economy with the aim of pushing unemployment below 5%, with fiscal

austerity pushed off into the future. Key elements (some of which have already

been announced) are likely to include:

an upgrade to GDP growth forecasts to 4.75% for the next financial year with unemployment expected to fall to 4.75% by June next year;

extra spending on aged care, childcare, disability and mental health, targeted industry support, climate, infrastructure and skills;

measures to help boost women’s’ economic security including changes to help women bolster their superannuation balances;

an extension of the Low and Middle Income Tax Offset (LMITO) to cover the next financial year;

spending and tax breaks to support the digital economy;

some possible tax reforms and deregulation;

more assistance for home buyers via the First Home Loan Deposit Scheme with a Family Home Guarantee to help 10,000 single parents into their own home with just a 2% deposit, another 10,000 places under the New Home Guarantee and a possible lifting of the home price caps; and

much lower budget deficits of $155bn this financial year and $65bn next financial year. The faster than expected economic recovery which means lower than expected welfare spending and increased revenue along with the higher iron ore price means that the starting point for the budget deficit is now much lower. However, we are assuming that more conservative Government forecasts, around $15bn in extra stimulus for the next financial year and a desire to leave some scope for surprise in the bag will see deficits of $155bn and $65bn reported on Budget night for this financial year and next.

On the data front in Australia, expect ABS retail sales data (Monday) to confirm the preliminary estimate of a 1.4% gain in March, with real retail sales down -0.4% in the quarter. Weekly payrolls data will also be released on Tuesday. The NAB business survey for April (also Monday) is likely to show continuing strong business conditions and confidence and weekly payrolls data will be released Tuesday.

Outlook for investment markets

Shares remain at risk of further volatility with possible triggers being a resumption of rising bond yields, coronavirus related setbacks, US tax hikes and geopolitical risks. But looking through the inevitable short-term noise, the combination of improving global growth and earnings helped by more stimulus, vaccines and still low interest rates augurs well for shares over the next 12 months.

Australian shares are likely to be relative outperformers helped by: better virus control enabling a stronger recovery in the near term; stronger stimulus; sectors like resources, industrials and financials benefitting from the rebound in growth; and as investors continue to drive a search for yield benefitting the share market as dividends are increased resulting in a 5% grossed up dividend yield. Expect the ASX 200 to end 2021 at a record high of around 7200 although the risk is on the upside.

Still ultra-low yields and a capital loss from rising bond yields are likely to result in negative returns from bonds over the next 12 months.

Unlisted commercial property and infrastructure are ultimately likely to benefit from a resumption of the search for yield but the hit to space demand and hence rents from the virus will continue to weigh on near term returns.

Australian home prices are likely to rise another 15% or so over the next 18 months being boosted by record low mortgage rates, economic recovery and FOMO, but expect a slowing in the pace of gains as government home buyer incentives are cut back, fixed mortgage rates rise, macro prudential tightening kicks in and immigration remains down relative to normal.

Cash and bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.1%.

Although the $A is vulnerable to bouts of uncertainty and RBA bond buying will keep it lower than otherwise, a rising trend is likely to remain over the next 12 months helped by strong commodity prices and a cyclical decline in the US dollar, probably taking the $A up to around $US0.85 by year end.

Eurozone shares rose 0.8% on Friday and the US S&P 500 rose 0.7% as April’s softer than expected US payroll report was interpreted by investors as helping to keep the Fed accommodative. Despite the positive US lead ASX 200 futures fell 4 points, or -0.1%, point to a softish start to trade on Monday for the Australian share market.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.Ok