2 July 2025

1300 794 893

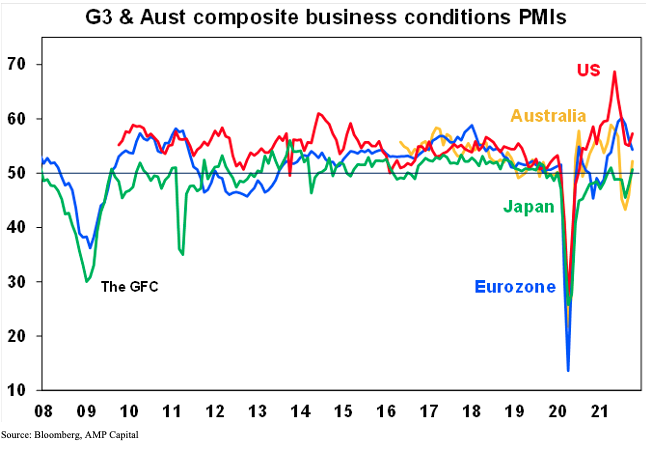

Business conditions PMIs fell back in Europe in October but rose in the US, Japan and Australia – partly reflecting relative movements in coronavirus cases. Price pressures remain high, reflecting bottlenecks.

Other US economic data was mostly strong. Industrial production and housing stats fell in September but both were impacted by poor weather, home sales rose solidly, the NAHB home builder conditions index for October was very strong, jobless claims are continuing to fall and while the composite business conditions PMI for manufacturing conditions in the Philadelphia region fell, they remain strong with increases in the new orders and employment components. Continuing unemployment claims have almost fallen back to pre-pandemic levels which should mean an increase in labour supply.

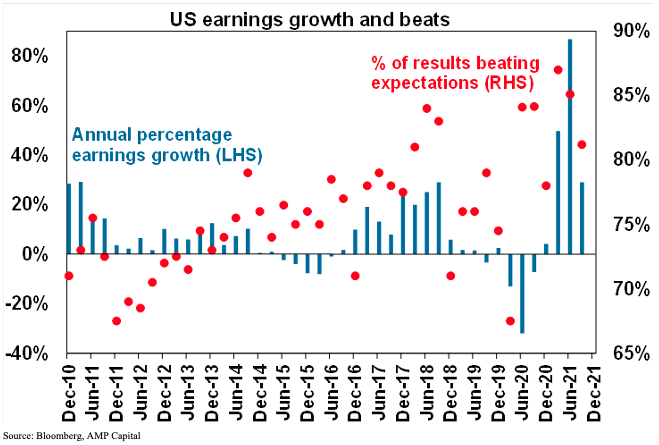

US earnings reports continuing to surprise on the upside. 81% of June quarter earnings reports to date have exceeded expectations with an average beat of 13%. This is down from the blow out recovery numbers seen in the previous few quarters but still above the norm which has seen 76% beat. So far only 23% of S&P 500 companies have reported though.

Japanese business conditions PMIs rose in October as coronavirus cases fell. While headline inflation rose on higher food & energy prices core inflation was unchanged at -0.5%yoy.

Chinese growth slowed further in the September quarter with GDP growth slowing a bit more than expected to 4.9%yoy as earlier policy tightening, coronavirus restrictions and weather all weighed. September monthly data was mixed though, with investment and industrial production down but retail sales accelerating as covid restrictions were eased. Average home prices fell for the first time since 2015 as property tightening measures hit. We expect some policy easing measures to boost consumer spending and investment.

Aussie economic events and implications

Australian business conditions PMIs rose in October consistent with reopening and the recovery underway in our Australian Economic Activity Tracker (see previous chart).

Jobs market starting to recover

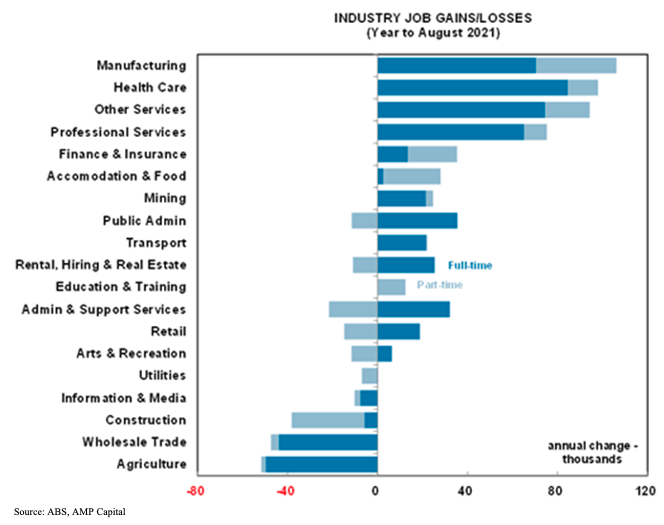

After falling for several months as a result of the lockdowns in south east Australia, payroll employment rose over the two weeks to 25 September with gains in NSW and the ACT and Victoria looking like its bottomed out. A further recovery is likely in the months ahead as a result of reopening. Meanwhile ABS data for the year to August shows that manufacturing and health care have seen the biggest gains in jobs whereas agriculture, wholesale trade and construction have seen the biggest losses with the surprise being that arts & recreation, retail and accommodation and food have been stronger than commonly perceived.

What to watch this week

In the US, September quarter GDP growth (Thursday) is expected to slow sharply to 3% annualised after 6.7% in the June quarter reflecting the impact of the Delta outbreak through July and August as well as supply constraints. In other data, expect strong gains in home prices and new home sales and a rise in consumer confidence (today), continued strength in underlying durable goods orders (Wednesday), a rise in pending home sales (Thursday), September quarter employment cost growth to pick up slightly to 0.8%qoq and core September private final consumption inflation to slow slightly to 0.2%mom but with annual inflation rising to 3.7%yoy (all Friday). The September quarter earnings reporting season will continue with the consensus being for 29% earnings growth on a year ago.

Various central bank meetings are expected to leave rates on hold in the week ahead. However, the Bank of Canada (Wednesday) is expected to be hawkish possibly announcing the end of QE and flagging rate hikes in the first half of next year, but the ECB and BoJ (Thursday) are expected to be dovish. The ECB will be monitored for any guidance it provides regarding asset purchases post the end of its pandemic bond buying program early next year and whether it pushes back against rising bond yields.

Eurozone September quarter GDP (Friday) is expected to rise 2.3%qoq reflecting reopening, and economic confidence data (Thursday) is expected to remain strong. CPI inflation for October (Friday) is expected to have increased further reflecting higher gas prices.

Japanese industrial production and jobs data is due Friday.

Outlook for investment markets

In Australia, the focus is expected to be on September quarter inflation data (Wednesday) which is expected to show a 0.8% rise in the quarter with annual inflation of 3.1%, compared to 0.8%qoq and 3.8%yoy in the June quarter. Key drivers are expected to be strong gains in prices for food, alcohol, clothing and furnishing, petrol prices (up around 6%) and a solid gain in rents but with the HomeBuilder subsidy keeping new dwelling purchase costs down and the underlying trimmed mean and median measures of inflation remaining at 0.5%qoq or 1.9%yoy. This would be only slight above RBA forecasts for underlying inflation so would be unlikely to have a significant impact on its forecasts. In other data, expect a 1.5% gain in September retail sales, a -5.1% fall in September quarter retail sales volumes and a further acceleration in housing credit growth (all due Friday).

Shares remain vulnerable to short-term volatility with possible triggers being coronavirus, global supply constraints and the inflation scare, less dovish central banks, the US debt ceiling and spending and tax plans and the slowing Chinese economy. But looking through the short-term noise, the combination of improving global growth and earnings, vaccines ultimately allowing a more sustained reopening and still low interest rates augurs well for shares over the next 12 months.

Expect the rising trend in bond yields to continue as it becomes clear the global recovery is continuing resulting in capital losses and poor returns from bonds over the next 12 months.

Unlisted commercial property may still see some weakness in retail and office returns but industrial is likely to be strong. Unlisted infrastructure is expected to see solid returns.

Australian home prices look likely to rise by about 21% this year before slowing to about 7% next year, being boosted by ultra-low mortgage rates, economic recovery and FOMO, but expect further slowing down of gains as poor affordability impacts, government home buyer incentives are cut back, listings return to more normal levels, fixed mortgage rates rise, macro prudential tightening slows lending and immigration remains down relative to normal.

Cash and bank deposits are likely to provide poor returns, given the ultra-low cash rate of 0.1%.

Although the $A could pull back further in response to the latest threats to global and Australian growth and weak iron ore prices, a rising trend is likely over the next 12 months helped by strong commodity prices and a cyclical decline in the US dollar, probably taking the $A up to about $US0.80.

Eurozone shares rose 0.6% on Friday while the US S&P 500 fell 0.1% on the back of some disappointing tech earnings and comments by Fed Chair Jerome Powell expressing more concern about inflation staying higher for longer. Despite the weak US lead ASX 200 futures rose 30 points, or 0.4%, pointing to a positive start to trade on Monday for the Australian share market.