2 July 2025

1300 794 893

Australian data remained strong over the last week with retail sales up 1.4% in March after snap lockdowns depressed sales in February and business conditions PMIs for April rising again to very strong levels and new home sales down from recent highs but also remaining strong. With strong PMIs, companies are also reporting rising input and output prices consistent with rising inflation.

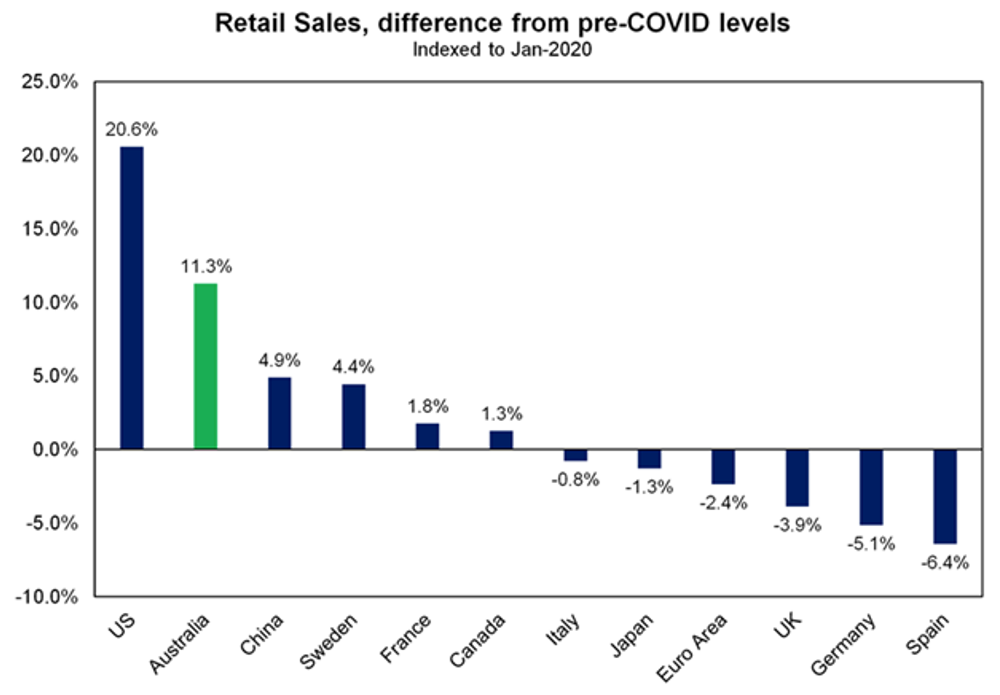

Australian retail sales compared to pre-pandemic levels have been far stronger than seen in most major countries – the exception being the US where stimulus checks totalling $2,000 so far this year for most adults have provided a huge boost.

While real retail sales look to have fallen in the March quarter detracting from consumer spending this may partly reflect a rotation in spending back downwards services as a result of relaxing social restrictions and this is likely to continue. We expect consumer spending growth (which includes retail sales and other services) to remain strong this year reflecting the recovery in jobs, strong levels of consumer confidence, low interest rates, positive wealth effects from gains in house prices and shares and pent-up demand evident in high saving rates.

What to watch over this week

The focus here will be on the March quarter CPI (tomorrow) which is expected to show a rise of 0.9% quarter on quarter or 1.4% year-on-year, reflecting a 9% rise in petrol prices (which alone will contribute +0.3 percentage points to inflation), a strong increase in new dwelling costs along with modest rises in rents and seasonal increases in health and education costs. Underlying inflation measures are likely to be more subdued at 0.5% quarter-on-quarter or 1.2% year-on-year, but this would still be at a stronger pace than implied by the RBA’s forecasts back in February. March quarter producer price inflation will be released Friday and private credit growth for March (also Friday) is expected to show a slight acceleration in housing credit growth.

What’s ahead for investment markets?

1. Shares remain at risk of further volatility, with possible triggers being a resumption of rising bond yields, coronavirus related setbacks, US tax hikes and geopolitical risks. But looking through the inevitable short-term noise, the combination of improving global growth helped by more stimulus, vaccines and still low interest rates augurs well for growth shares over the next 12 months.

Global shares are expected to return around 8% over the next year but expect a rotation away from growth heavy US shares to more cyclical markets in Europe, Japan and emerging countries.

Australian shares are likely to be relative outperformers helped by:

2. Still ultra-low yields and a capital loss from rising bond yields are likely to result in negative returns from bonds over the next 12 months.

3. Unlisted commercial property and infrastructure are ultimately likely to benefit from a resumption of the search for yield but the hit to space demand and hence rents from the virus will continue to weigh on near term returns.

4. Australian home prices are likely to rise another 15% or so over the next 18 months to 2 years being boosted by record low mortgage rates, economic recovery and FOMO, but expect a slowing in the pace of gains as government home buyer incentives are cut back, fixed mortgage rates rise, macro prudential tightening kicks in and immigration remains down relative to normal.

5. Cash and bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.1%.

6. Although the $A is vulnerable to bouts of uncertainty and RBA bond buying will keep it lower than otherwise, a rising trend is likely to remain over the next 12 months helped by rising commodity prices and a cyclical decline in the US dollar, probably taking the $A up to around $US0.85 by year end.