1 July 2025

1300 794 893

The minutes from the Fed’s last meeting provided no real surprises – it looks to be planning a $US15 billion reduction a month in bond buying starting in the next couple of months and ending mid next year. Of course, tapering is not tightening, and while rate hikes are getting closer, they still look at least a year off.

US economic data was mostly strong. Retail sales rose more than expected in September, New York region manufacturing conditions fell back in October but are still strong, job openings fell in August but remain high and paired with falling jobless claims, indicate a continuing strong labour market. 80% of June quarter earnings reports to date have exceeded expectations but so far only 41 S&P 500 companies have reported.

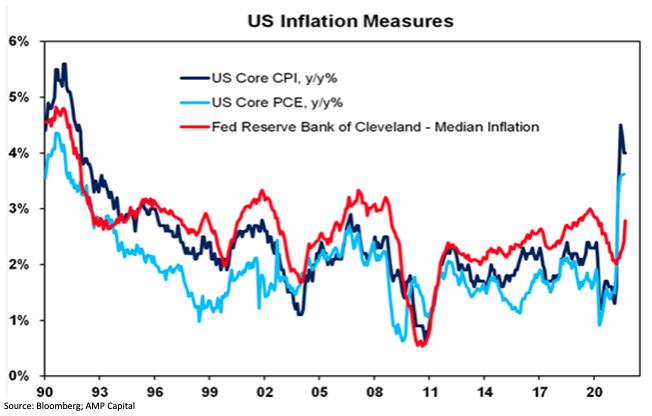

US inflation pressures broadening

While core US inflation in September was in line with market expectations at 0.2%mom and 4% YoY, price increases have been broadening with median inflation rising to 2.8% YoY as supply constraints along with the recovery in rents impact. And producer price inflation accelerated further to 8.6% YoY. Ultimately, we see this settling down as the pandemic recedes, more workers return to work and consumer spending rotates back to services from goods but that may still take another 6-12 months.

Japanese producer price inflation accelerated further to 6.3% YoY in September reflecting global pressures although so far there is not much pass through to Japanese consumers.

Similarly, in China where producer price inflation rose to 10.5% YoY in September, but CPI inflation fell to 0.7% YoY and core inflation was unchanged at 1.2% YoY, posing no major constraint for the PBOC in reinvigorating Chinese growth. Although Chinese exports surprise on the upside, in September imports slowed more than expected and credit growth was weaker than expected consistent with a continual slowing in growth. Of interest to Australia: while iron ore import volumes are down -12% YoY, coal import volumes are up 76% YoY.

Australian economic events and implications

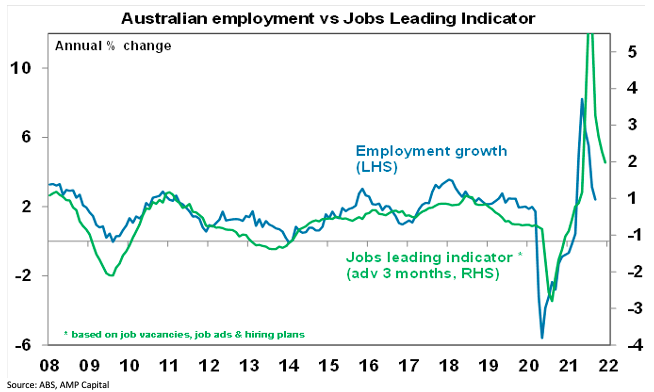

Jobs down, but it's history now. There were no surprises with employment down another 138,000 in September reflecting the lockdowns in Victoria, NSW and the ACT. From its June pre lockdown high, employment has fallen by -330,000 but thanks to a plunge in participation, the workforce has fallen by -281,000 such that unemployment has actually fallen to 4.6% from 4.9%. Allowing for those working zero hours and the decline in participation “effective unemployment” has actually risen to around 7.6%.

The good news though is that with NSW now reopening and Victoria set to follow, employment is likely to start recovering (although the ABS jobs survey may not pick this up till November). The relative resilience in job vacancies through these lockdowns compared to last year as reflected in our Jobs Leading Indicator is a positive sign in this regard. The bad news, of course, is that with the reopening, labour force participation will rebound probably back to where it was in June which should see unemployment move up to about 5% by year-end before it resumes its downtrend through next year.

Solid confidence, home building strong

While confidence readings were mixed in the last week – with business confidence up according to the NAB survey and consumer confidence up according to the ANZ/Roy Morgan survey but down according to the Westpac/MI survey – all are near reasonable levels and well above last year’s lows which augurs well for recovery. After the adjustment from the HomeBuilder boost, new home sales for the six months to September were up 9.3% on the same period in 2019. A 23% jump in dwelling commencements in the June quarter points to a big pipeline of dwelling construction (albeit construction shutdowns in the last few months in NSW and then Victoria will delay some of this).

What to watch this week

In the US, flat September housing starts (today) after a solid rise in August, a rise in existing home sales (Thursday) and a continuing solid reading for the October composite PMI (Friday) with the focus likely to be on supply constraints and price pressures. The September quarter earnings reporting season will start to ramp up with the consensus being for 28% earnings growth on a year ago.

European business conditions PMIs for October (Friday) are also likely to remain solid, albeit with the focus on supply constraints.

Chinese September quarter GDP data is likely to confirm its growth slowdown with its 0.4% QoQ or 5% YoY reflecting earlier monetary tightening and coronavirus restrictions in August. September data for industrial production and investment is also likely to show some further loss of momentum but retail sales growth is expected to pick up following the relaxation of covid controls.

Japanese business conditions PMIs for October are likely to improve following the decline in coronavirus cases but core inflation for September is likely to have remained around -0.5% YoY with both due Friday.

Australian business conditions PMIs for October (Friday) are likely to bounce as reopening in NSW and the prospect of reopening in Victoria boosts confidence. RBA Governor Lowe will participate in a panel discussion (Friday) on central bank independence, mandates and policies that may be of some interest in light of a likely upcoming review of the RBA.

Outlook for investment markets

Shares remain vulnerable to short-term volatility with possible triggers being coronavirus, global supply constraints & the inflation scare, less dovish central banks, the US debt ceiling and spending and tax plans and the slowing Chinese economy. But looking through the short-term noise, the combination of improving global growth and earnings, vaccines ultimately allowing a more sustained reopening and still-low interest rates augurs well for shares over the next 12 months.

Expect the rising trend in bond yields to continue as it becomes clear the global recovery is continuing resulting in capital losses and poor returns from bonds over the next 12 months.

Unlisted commercial property may still see some weakness in retail and office returns but industrial is likely to be strong. Unlisted infrastructure is expected to see solid returns.

Australian home prices look likely to rise by about 21% this year before slowing to about 7% next year. The gains are being propped up by ultra-low mortgage rates, economic recovery and FOMO, but expect a progressive slowing in the pace of gains due to poor affordability, government home buyer incentives being cut back, listings returning to more normal levels, fixed mortgage rates rising, macro prudential tightening slows lending and immigration remains down relative to normal.

Cash and bank deposits are likely to provide poor returns, given the ultra-low cash rate of 0.1%.

Although the $A could pull back further in response to the latest threats to global and Australian growth and weak iron ore prices, a rising trend is likely over the next 12 months helped by strong commodity prices and a cyclical decline in the US dollar, probably taking the $A up to about $US0.80.

Eurozone shares rose 0.8% on Friday and the US S&P 500 rose 0.7% helped by solid US earnings results and better than expected US retail sales. Reflecting the positive US lead, ASX 200 futures are up 31 points, or 0.4%, pointing to a positive start to trade on Monday for the Australian share market.