12 July 2025

1300 794 893

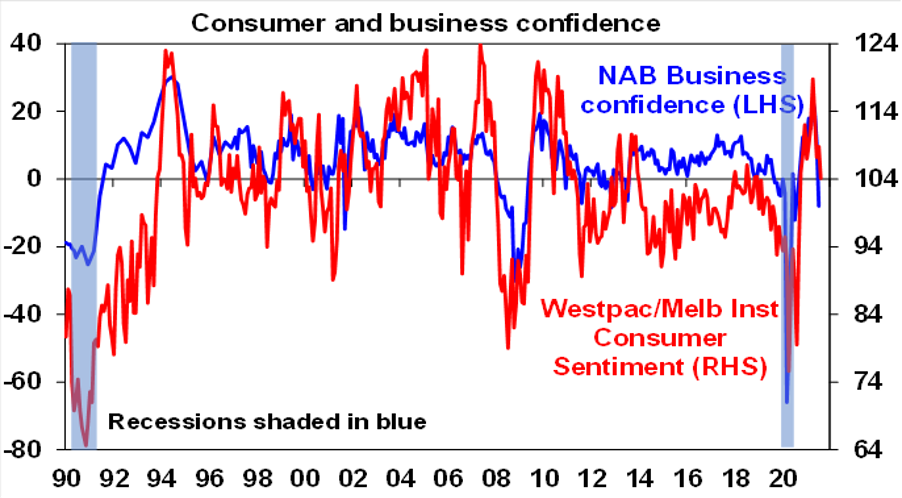

In Australia, new home sales as measured by the HIA fell sharply and business and consumer confidence fell reflecting the impact of the lockdowns. Fortunately, confidence has held up far better so far than was the case early last year and this likely reflects the fact that not all of Australia is in lockdown, there is more confidence this time around that government support will work and the economy will bounce back, people have found better ways to live and work with lockdowns and the vaccines are now providing hope.

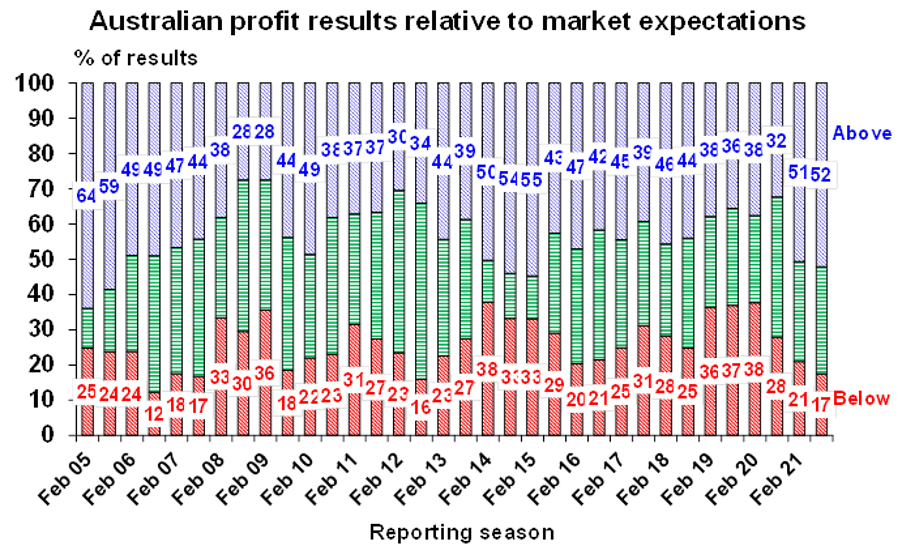

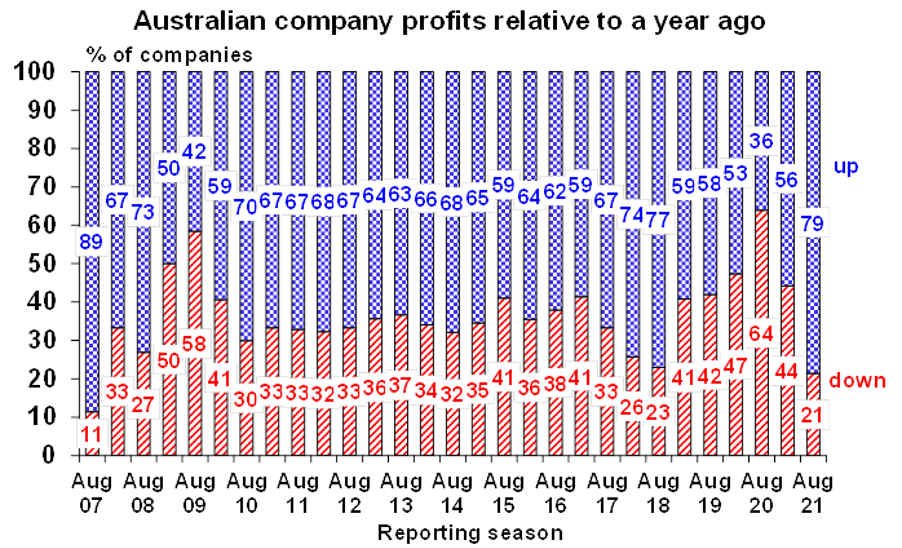

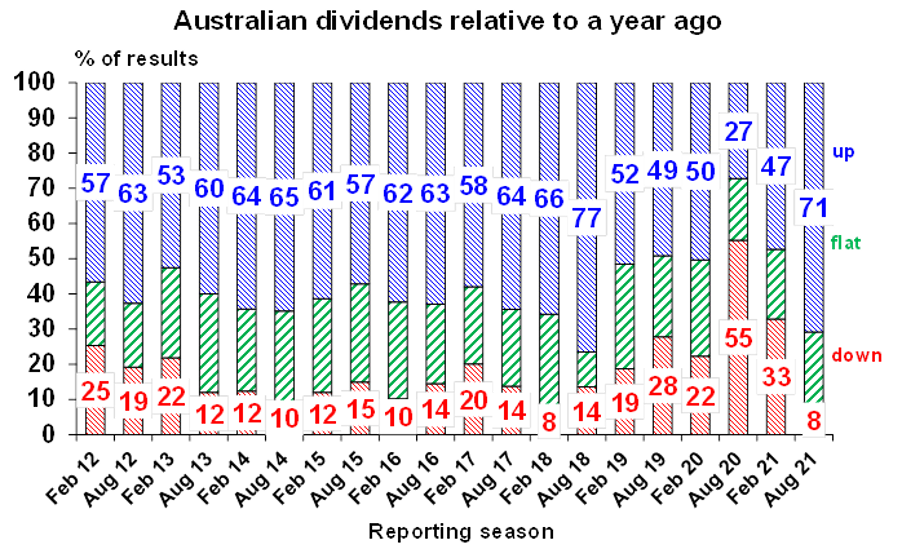

The Australian June half earnings reporting season has picked up and while the lockdowns are weighing on the outlook, so far this seems to have been swamped by reports of strong earnings growth and a huge return of capital to shareholders via dividends and buybacks notably by Rio, CBA and Telstra. Its early days yet as only about 35 major companies have reported so far and there is a tendency for good news results to come out early in the reporting period, but so far 52% of results have surprised on the upside, 79% have seen earnings up on a year ago & 71% have increased dividends.

What to watch over the week

In Australia, jobs data for July on Thursday will be the first big data release to show some impact of lockdowns in response to recent Delta outbreaks. However, it may not fully show up due to the timing of the ABS’ reference period for July so as a result we only expect a loss of 50,000 jobs mainly driven by NSW with unemployment rising to 5% (from 4.9%), but with a much bigger impact showing up in August. Ultimately employment is expected to fall by around 300,000. This is less than the -857,000 jobs lost in April and May last year as not all of Australia is in lockdown, businesses may be less inclined to lay off this time around given the rebound seen last year and only recent talk of labour shortages, and business confidence and job ads don’t seem to have fallen as rapidly as seen last year. However, there will likely be a bigger hit to hours worked. June quarter data is expected to show a 0.5% lift in wages (tomorrow) taking annual wages growth to 1.8%.

The Australian June half profit reporting season will really start to ramp up with about 90 major companies comprising about one third of the share market’s capitalisation reporting in the week ahead. This includes BHP and Woodside (today), Amcor, Coles and CSL (tomorrow), ASX, South 32 and Treasury Wine Estates (Thursday) and Cochlear and Stockland (Friday). Consensus earnings growth expectations are for a 50% rise in earnings for 2020-21 and a 56% rise in dividends. The resources sector is expected to see a doubling in profits followed by 58% growth in bank earnings. Outlook statements are likely to be cautious though given the uncertainty posed by recent coronavirus outbreaks and lockdowns.

Outlook for investment markets

Shares remain vulnerable to a short-term correction with possible triggers being the upswing in global coronavirus cases, the inflation scare and US taper talk, likely US tax hikes and a debt ceiling standoff and geopolitical risks. But looking through the short-term noise, the combination of improving global growth and earnings helped by more fiscal stimulus, vaccines allowing reopening once herd immunity is reached and still low interest rates augurs well for shares over the next 12 months.

Expect the rising trend in bond yields to resume as it becomes clear the global recovery is continuing resulting in capital losses and poor returns from bonds over the next 12 months.

Unlisted commercial property may still see some weakness in retail and office returns but industrial is likely to be strong. Unlisted infrastructure is expected to see solid returns.

Australian home prices look likely to rise by around 20% this year before slowing to around 5% next year, being boosted by ultra-low mortgage rates, economic recovery and FOMO, but expect a progressive slowing in the pace of gains as poor affordability impacts, government home buyer incentives are cut back, fixed mortgage rates rise, macro prudential tightening kicks in and immigration remains down relative to normal. The lockdowns have increased short term uncertainty though.

Cash and bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.1%. We remain of the view that the RBA won’t start raising rates until 2023.

Although the $A could pull back further in response to the latest coronavirus outbreaks and the threats posed to global and Australian growth, a rising trend is likely to remain over the next 12 months helped by strong commodity prices and a cyclical decline in the US dollar, probably taking the $A up to around $US0.85 over the next 12 months.