6 July 2025

1300 794 893

Major global economic events and implications

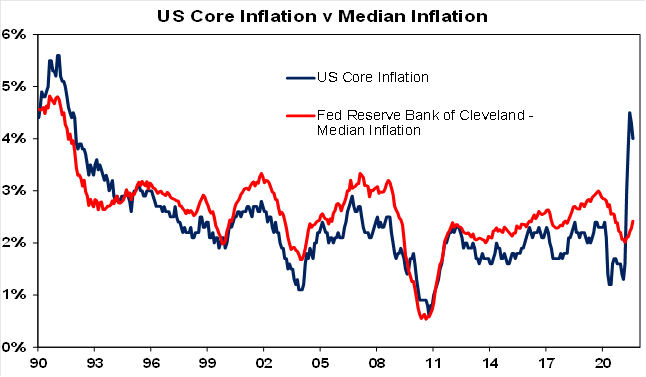

Mostly strong US activity data, but a breather for the Fed on inflation. Retail sales rebounded in August, regional business conditions and small business confidence rose as did industrial production. CPI inflation came in weaker than expected in August as price increases in reopening sectors reversed putting paid to a September taper announcement. However, tapering is still on track for later this year as supply bottlenecks remain, price components in business surveys remain very high and median inflation has been edging up.

Chinese activity data for August slowed more than expected reflecting a combination of coronavirus restrictions, earlier policy tightening and regulatory action in property and steel production. Property price growth also slowed further. While regulatory action will continue against some industries – with Macau’s gaming industry being the latest – we expect macro policy to start becoming more supportive in the months ahead as will an easing in covid restrictions.

Australian economic events and implications

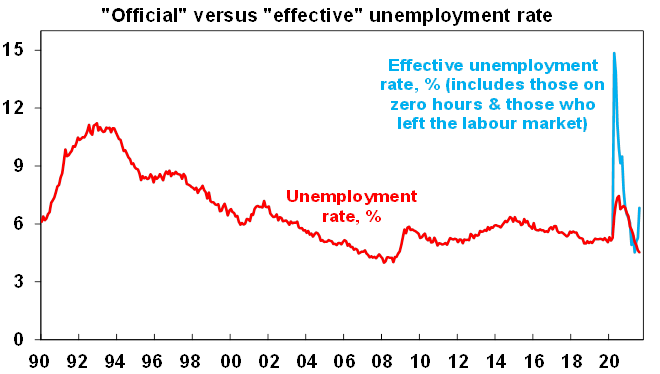

Jobs take a hit. The bad news is that the lockdowns are now hitting the jobs market with a sharp fall in employment and hours worked in August with more to come this month as the full impact of the Victorian lockdown shows up. While unemployment surprisingly fell to 4.5%, this was due to a plunge in participation in NSW as people gave up looking for work. Adjusting for the collapse in participation and a sharp rise in those working zero hours, “effective” unemployment has now risen to 6.8% from a low of 4.5% in May. Perversely reopening may see unemployment rise a bit as participation rebounds.

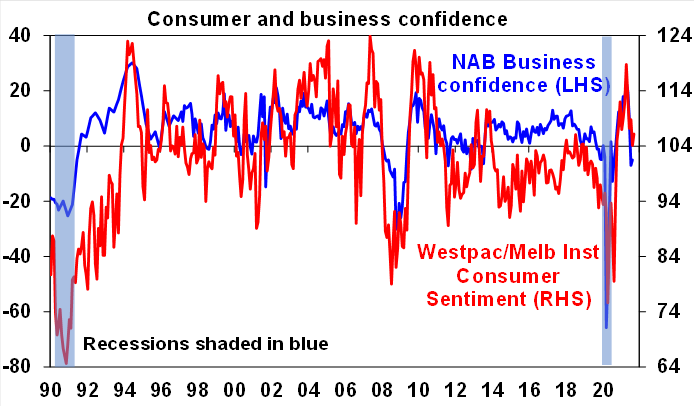

The good news though is that consumer and business confidence are proving resilient compared to last year likely reflecting more confidence that government support will work, people having found better ways to work and live with lockdowns and the rapid rise in vaccinations and reopening roadmaps providing hope. Consistent with this, job listings and hiring plans are holding up well suggesting that employment may bounce back reasonably quickly once lockdowns end.

Australia’s population takes a breather. ABS data showed that population growth over the year to the March quarter was just 0.1% as net immigration went backwards. And with the border closures this will likely continue into next year. This is bad news for our long-term growth potential, aging population and dynamism. But it also provides a potential breather for the hot property market (as confirmed by ABS data showing a 16.8% rise in property prices over the year to the June quarter) as it means at least a halving in underlying demand for housing, which when combined with continuing strong home building may eventually lead to an oversupply of property.

What to watch over the next week?

In the US, the Fed (Wednesday) is likely to provide advance notice that it’s on track to formally announce a tapering in its bond buying later this year, conditional on further improvement in the jobs market. Perhaps the main risk is that the Fed’s dot plot of officials’ interest rate expectations may see the median dot move to a rate hike in 2022. On the data front, expect modest gains in housing starts (today) and new home sales (Friday). Business conditions PMIs for September (Thursday) may rise slightly as Delta fears have faded a bit.

Eurozone business conditions PMIs for September (Thursday) are likely to have remained strong.

The Bank of Japan (Wednesday) is expected to leave monetary policy unchanged and to remain dovish. Japanese inflation data (Friday) is expected to remain weak.

The BoE (Thursday) is likely to leave monetary policy on hold.

In Australia, it’s hard to see the minutes from the last RBA meeting (today) adding anything new after RBA GovernorLowe’s speech explaining RBA views. Business conditions PMIs (Thursday) for September are expected to improve slightly reflecting reopening optimism and the ABS will release payroll jobs and June quarter household wealth data (also Thursday).

Outlook for investment markets

Shares remain vulnerable to a short-term correction with possible triggers being coronavirus, the inflation scare and US taper talk, likely US tax hikes and a debt ceiling standoff and the slowing Chinese economy. But looking through the short-term noise, the combination of improving global growth and earnings helped by more fiscal stimulus, vaccines ultimately allowing a more sustained reopening and still low interest rates augurs well for shares over the next 12 months.

Expect the rising trend in bond yields to resume as it becomes clear the global recovery is continuing resulting in capital losses and poor returns from bonds over the next 12 months.

Unlisted commercial property may still see some weakness in retail and office returns but industrial is likely to be strong. Unlisted infrastructure is expected to see solid returns.

Australian home prices look likely to rise by around 20% this year before slowing to around 7% next year, being boosted by ultra-low mortgage rates, economic recovery and FOMO, but expect a progressive slowing in the pace of gains as poor affordability impacts, government home buyer incentives are cut back, fixed mortgage rates rise, macro prudential tightening kicks in and immigration remains down relative to normal.

Cash and bank deposits are likely to provide poor returns, given the ultra-low cash rate of 0.1%. The setback from coronavirus lockdowns could push the first rate hike back into 2024.

Although the $A could pull back further in response to the latest coronavirus outbreaks, the threats posed to global and Australian growth and falling iron ore prices, a rising trend is likely over the next 12 months helped by strong commodity prices and a cyclical decline in the US dollar, probably taking the $A up to around $US0.80.