6 July 2025

1300 794 893

Share markets were mixed over the past week – up in the US and Europe on strong US earnings results, but down in Japan, China and Australia. The Australian share market was hit by interest rate fears after a stronger than expected underlying inflation result and signs the RBA may be becoming more hawkish. Bond yields fell in the US and Europe but rose in Australia with the 10 year yield above 2% for the first time since March 2019 on rate hike expectations. Oil, metal and iron ore prices fell but expectations for earlier and more aggressive RBA tightening pushed the AUD up as the USD weakened.

Central banks diverging

Reflecting increasing concern about inflation, the Bank of Canada surprised some by ending its quantitative easing program and brought forward the expected lift off for rates from second half 2022 to the middle quarters of 2022. By contrast, both the ECB and Bank of Japan remained dovish - reflecting their lower starting points for inflation and subpar experience over the last decade. Given the Eurozone and Japan’s chronic underperformance on inflation pre pandemic its hard to see either raising rates before 2023.

Pressure building on the RBA

We now expect the first rate hike in a year’s time and the RBA to soften its rates guidance and abandon the 0.1% yield target (possibly as soon as Tuesday). Underlying inflation at 2.1% YoY in the September quarter came in well ahead of the RBA’s implied forecast of about 1.75% YoY. Of course, it’s well below the inflation rates being seen in some other comparable countries and the rise in inflation is narrowly based. But it can’t be ignored, and it has come at a time when the reopening in NSW and Victoria are occurring faster than expected with confidence and labour markets also stronger than expected.

This is all evident in a rapid rebound in our Australian Economic Activity Tracker (see below). The RBA won’t rush into a rate hike because it wants to see that “inflation is sustainably within the target range” and for this to occur it will want to see more evidence that the inflation pick up is moving beyond transitory distortions due to the pandemic, that the economic recovery is sustained, full employment is reached and wages growth is about 3% or more before hiking rates. However, with the economy recovering we believe that the conditions for the start of rate hikes will now be in place by late 2022 so we expect the first hike to be in November 2022 taking the cash rate to 0.25% followed by a 0.25% hike in December 2022, taking the cash rate to 0.5% by the end of next year.

What we expect from RBA

In the interim we expect the RBA: to bring forward its guidance for the first rate hike to 2023; to remove or weaken the 0.1% yield target for the April 2024 bond; and to further taper its bond buying in February next year to $2bn a week. With the RBA failing to defend the yield target in the last week its looking like it could be abandoned or changed on Tuesday along with a softening in forward guidance on rates. Interest rates will still be very low and monetary policy very easy into 2023 – just less easy than it has been. Allowing the yield target to die before the Board has taken a decision on it does strike me as surprising though and may have the effect of denting the RBA’s credibility a bit – if indeed that is what has happened!

However, money market expectations for the RBA to start hiking by mid next year and for at least four rate hikes over the next 12 months taking the cash rate to 1 to 1.25% look way over the top and I am conscious of the market’s tendency to be way too hawkish for most of the last decade e.g. it missed most of the 2019-2020 easing cycle.

Australian home price gains to slow further ahead of falls from late 2022 and through 2023. Further tapering and an end to the yield target will likely mean higher bond yields and higher fixed mortgage rates which combined with the deterioration in affordability and higher interest rate serviceability buffers points to a further slowing in home price gains over the year ahead and when combined with higher variable rates from late next year points to likely price falls into 2023.

US Democrats getting closer to a deal on Build Back Better. The deal looks likely to involve about $US1.8 trillion in new spending (over several years) financed by various revenue measures possibly including a minimum 15% corporate tax and a levy on multimillionaires and tax enforcement measures (often a favourite). This would probably mean a smaller hit to corporate earnings than expected and if agreed it should clear the way for passage of the infrastructure package and for moderate Democrats to support an increase in the debt ceiling.

Climate action

The Australian Government issued a plan to achieve zero net carbon emissions by 2050 ahead of the COP26 climate change meeting in Glasgow. Its reliance on investment and technology trends (some of which are unproven or yet to happen) suggest a far more modest impact on the economy from the plan compared to what would occur under a cap and trade carbon pricing system and a less certain outcome. A key risk is that investors will baulk at the lack of strong objectives for 2030 thereby slowing the necessary investment to facilitate the adjustment to a low carbon economy. The shift to a low carbon world will, if managed appropriately - including protecting those workers and communities adversely affected - result in more opportunities than it destroys ultimately resulting in a benefit to the economy. But the faster we move the easier the adjustment and the better the outcome for the environment. In the meantime the impact of climate change on the economy and the shift in global demand away from greenhouse gas emitting activities will continue to have a huge impact in the decades ahead and affect the availability of capital for countries not playing their part.

More epic songs

It was pointed out that I missed perhaps the most epic song of all – American Pie by Don McLean. It ran for 8.42 minutes. It relates to the 1959 plane crash which killed Buddy Holly, Ritchie Valens and The Big Bopper but also relates to the Baby Boomer generations’ disillusionment and loss of innocence by the early 1970s. Paul McCartney and Wings’ Band on the Run is another epic. At 5.09 it's one of McCartney’s longest songs, has three different sections and was recorded in Lagos but not before the demos were stolen.

Coronavirus update

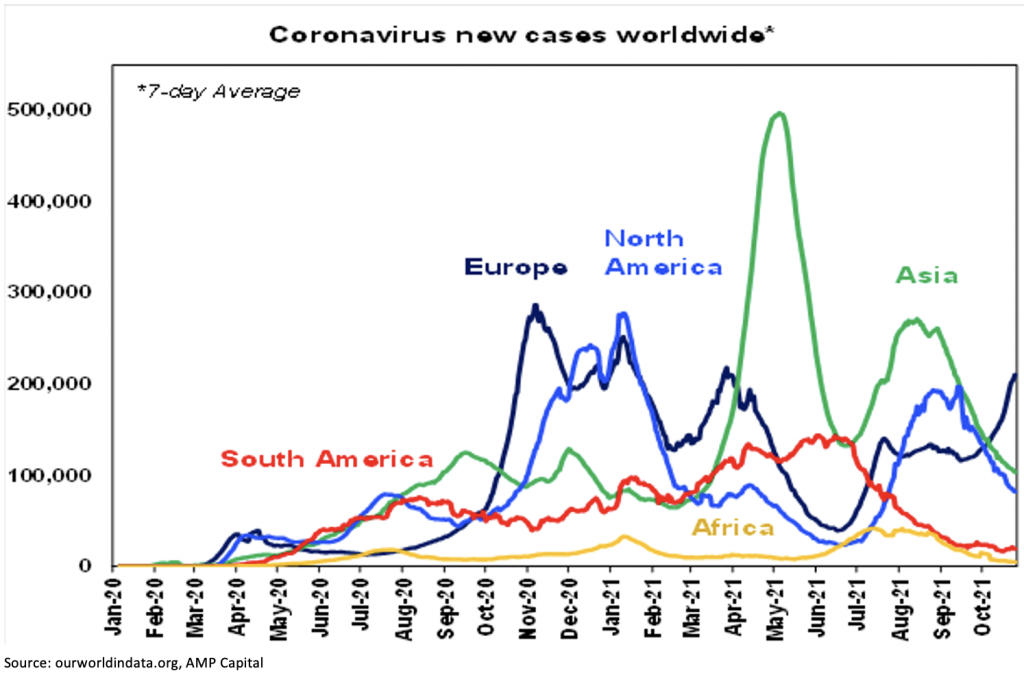

The decline in new global coronavirus cases appears to have bottomed as rising cases in Europe offset flat to declining trends in other regions (including the US).

A rise in new cases after reopening looks inevitable. The rise in new cases in the UK and Europe appears to reflect reopening and the rapid relaxation of distancing rules (notably in the UK), the start of cooler weather, vaccination rates stalling below 70% of the whole population, fading efficacy against new infection, a slow start to boosters and maybe a new Delta variant (AY.4.2). The US faces a similar risk with only 58% fully vaccinated. However, even gold standard Singapore with 83% fully vaccinated has seen a surge in new cases to over 3500 a day which saw the return of some restrictions to keep pressure on hospitals.

There appears to be little political support for a return to lockdowns, but this can’t be ruled out if hospitals are overwhelmed. The key to avoiding problems appears to be to get vaccination rates to very high levels, reopen and remove distancing restrictions gradually and quickly roll out booster shots to those whose last shot was 5 months or so ago.

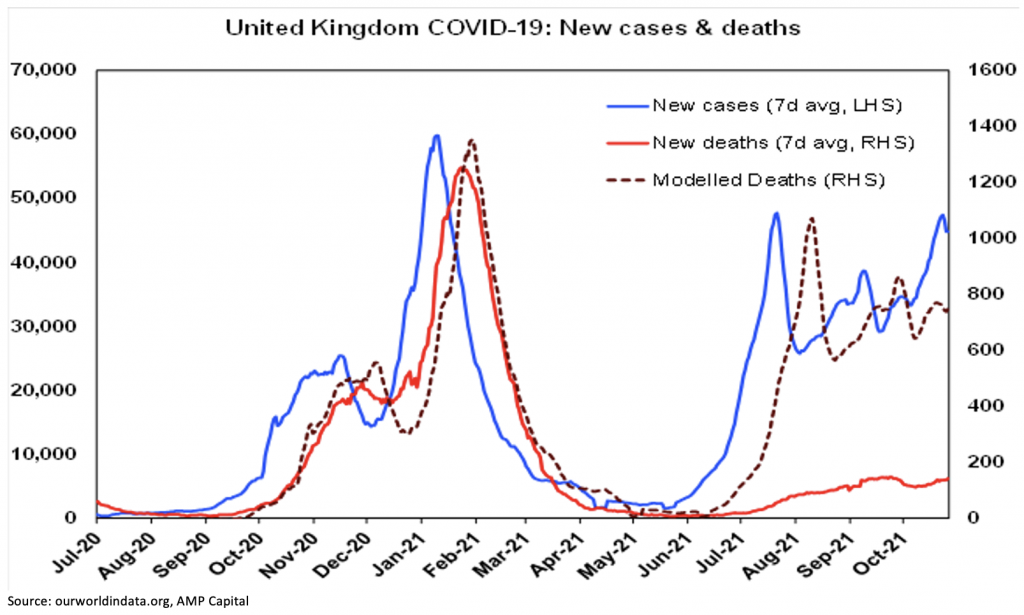

Key to watch will be whether vaccines remain successful in keeping hospitalisations manageable and deaths down. So far so good in Europe and the UK. Deaths in the UK are continuing to run at less than 20% of the level suggested by the December/January wave and hospitalisations remain subdued.

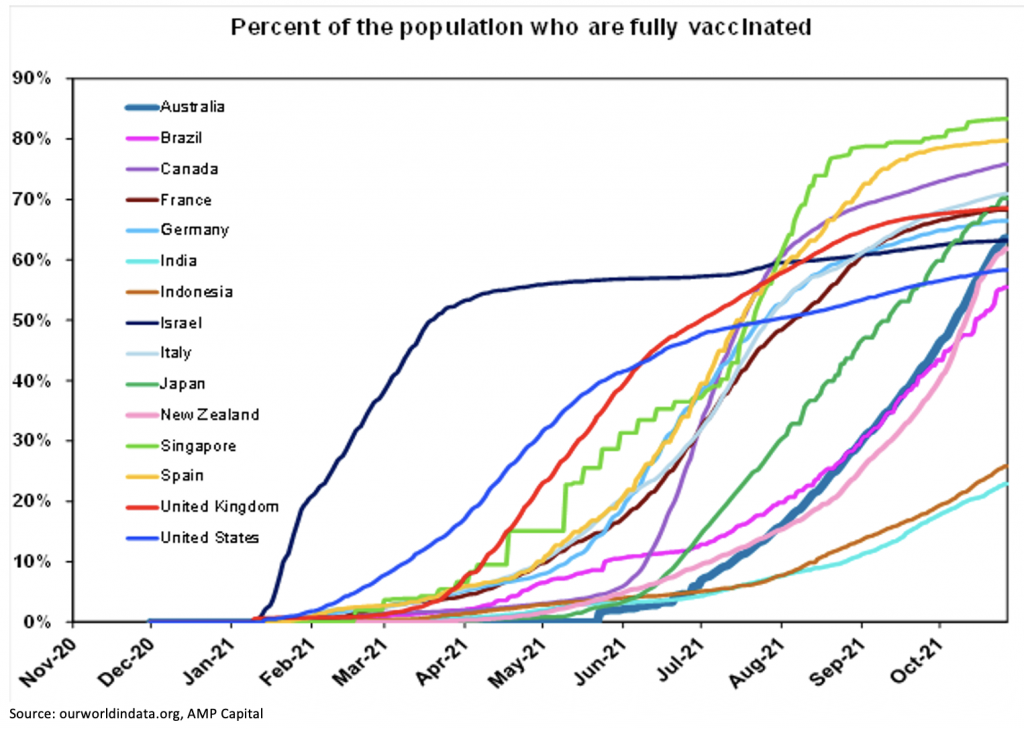

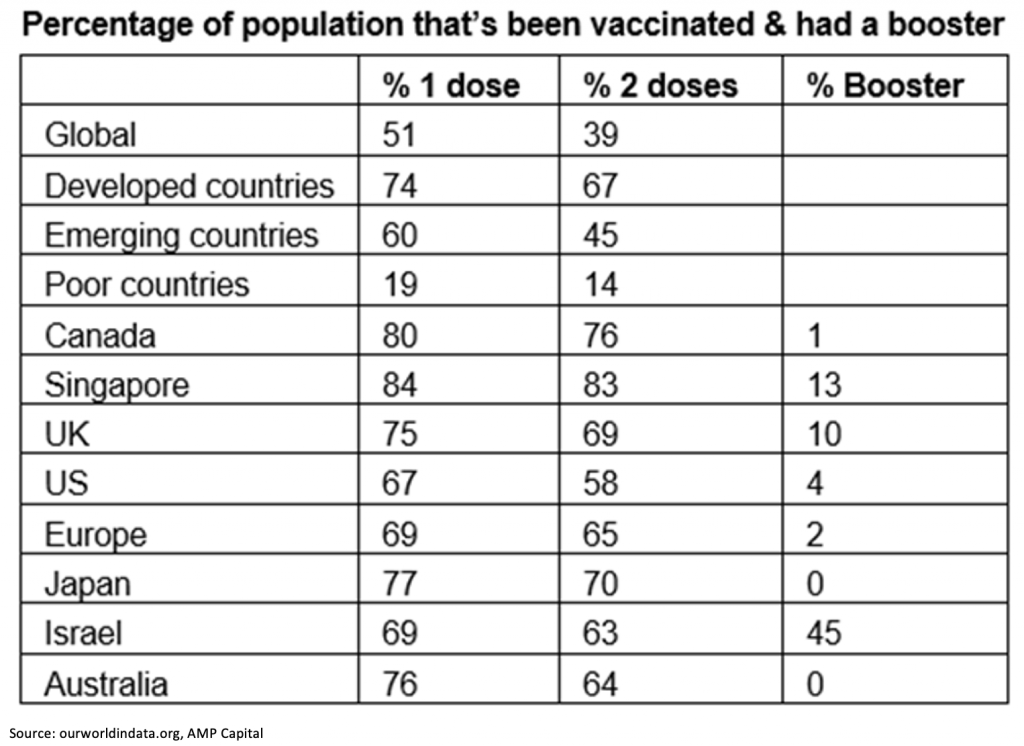

51% of people globally have now had one dose of vaccine and 39% have had two doses.

A risk remains that poor countries are lowly vaccinated which increases the risk of mutations.

Australia’s daily vaccination rate has slowed but remains high at about 0.9% of the population and the proportion of the total population that has had one dose (76%) has now surpassed many other developed countries and will soon do so for two doses.

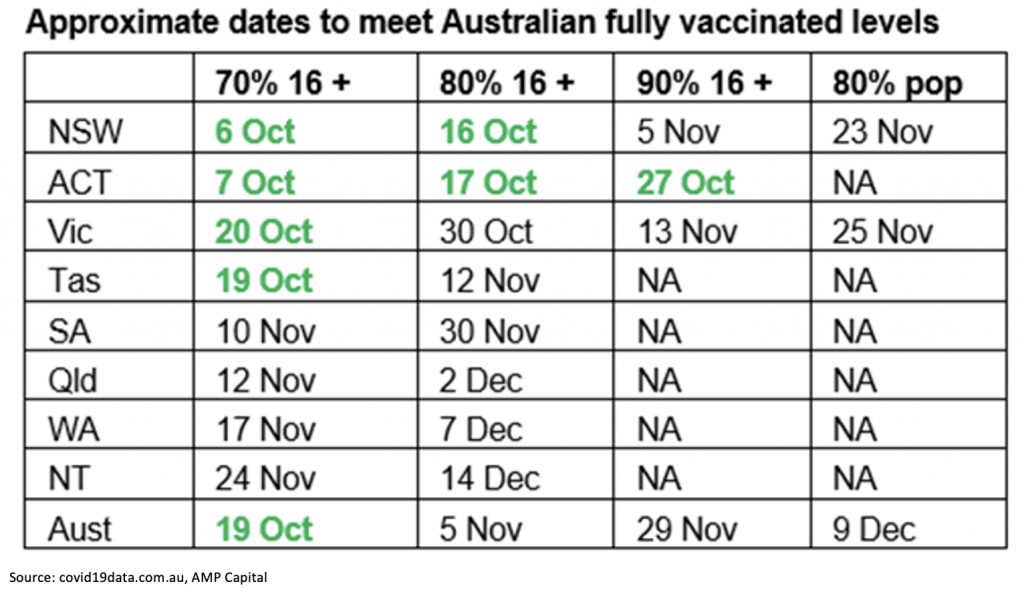

NSW has seen a slowing in first doses but has done well to get above 93% of adults with one dose and the ACT is at 99%. First doses will likely continue to drift up if vaccination is approved for 5 to 12 year-olds though. Allowing for current trends and the average gap between 1st and 2nd doses the following table shows approximately when key vaccine targets will be met.

The ACT, NSW, Victoria and Tasmania are leading the charge. Other states should hit the 70% of adults double vax target near mid-November. On current trends, Australia will average 90% of the adult population fully vaccinated by the end of November. And booster shots are on track to be rolled out from the next week or so.

The faster than expected uptake of vaccines is seeing a faster than expected reopening including earlier than expected moves to reopen some state borders and to allow Australians to travel overseas.

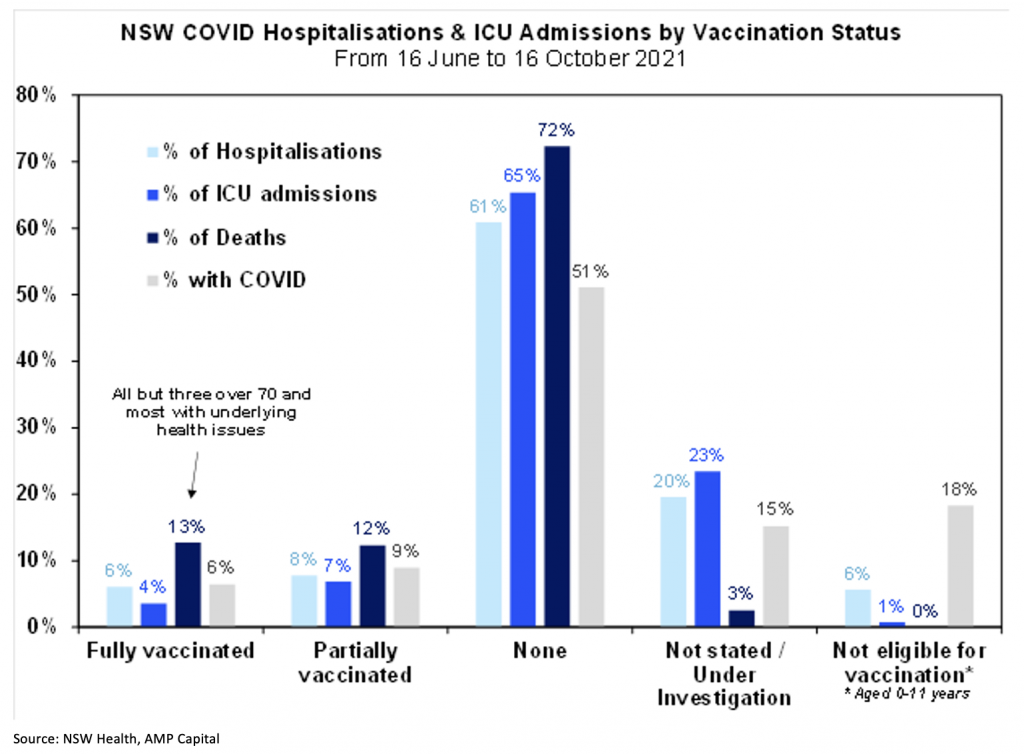

Vaccination is continuing to keep serious illness down. Coronavirus case data for NSW shows that the fully vaccinated continue to make up a low proportion of cases, hospitalisations and deaths and the level of deaths is running about 20% of the level predicted on the basis of the previous wave.

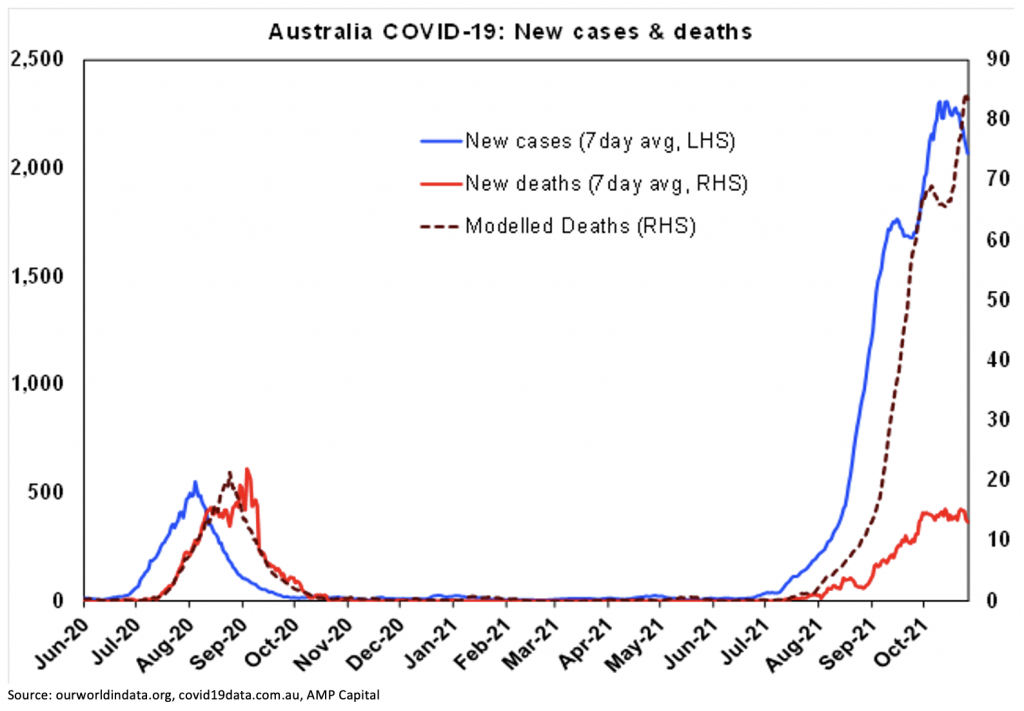

The main risk in Australia is a resurgence in new cases after reopening - like several other countries have seen - which threatens to overwhelm the hospital system necessitating some reversal in reopening. Key to watch will be hospitalisations and deaths – in terms of whether the hospital system is coping. So far so good – with hospitalisations and deaths remaining subdued relative to new cases compared to past waves - but it's only early days in the reopening process.

Economic activity trackers

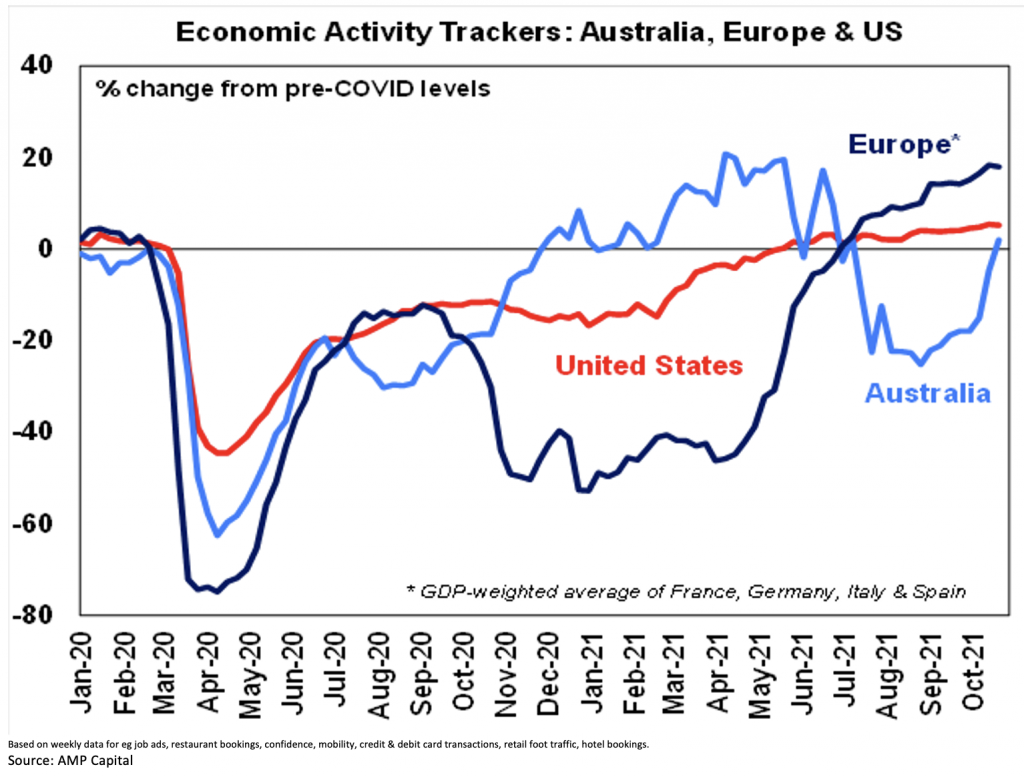

Our Australian Economic Activity Tracker surged higher again over the last week as Victoria joined reopening, with broad based improvement but particularly in restaurant and hotel bookings, card transactions and mobility. It's now back above 2019 levels and has almost caught up to the US. It’s likely to move higher in the months ahead as reopening continues although risks around reopening driving increased cases and possible setbacks could constrain it at times. Our European & US Economic Activity Trackers are little changed.

Based on weekly data e.g. job ads, restaurant bookings, confidence, mobility, credit & debit card transactions, retail foot traffic, hotel bookings.

Major global economic events and implications

US GDP slowed sharply but other US data was mostly strong. US September quarter GDP slowed to a 2% annualised pace reflecting the Delta outbreak and supply constraints but September data points to a rebound. Consumer confidence, underlying durable goods orders, new home sales rose and house prices all rose and jobless claims fell.

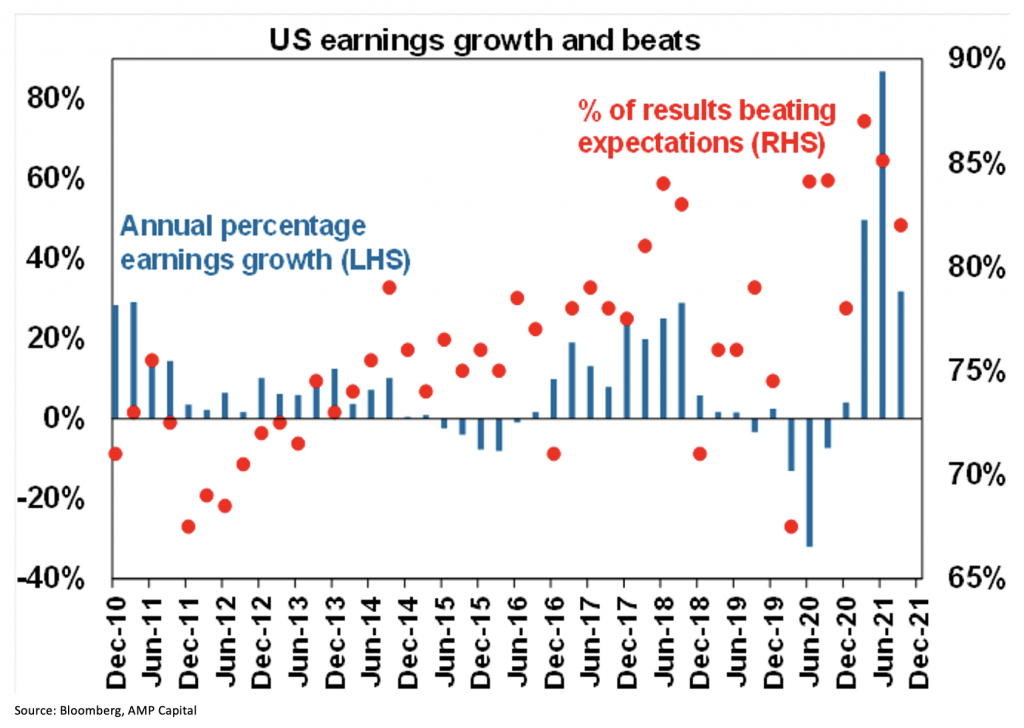

US earnings reports continue to surprise on the upside. 53% of S&P 500 companies have now reported September quarter earnings and 82% have exceeded expectations with an average beat of 10%. This is skewed towards financials with an average beat of 20% as loan loss reserves are released but the rest of the market is beating by a still strong average of 9%. Earnings growth expectations for the quarter have now risen to 32% YoY and are likely to end up about 38% YoY.

Japan saw a sharp fall in industrial production but a stronger than expected rise in retail sales rose and okay jobs data.