15 July 2025

1300 794 893

Global shares mostly fell over the last week on growth concerns. US shares fell -0.6% not helped by the usual volatility associated with the expiry of option and futures contracts on Friday, Eurozone shares lost -0.9% and Chinese shares fell -3.1% with concerns about the Evergrande Group also weighing. Japanese shares managed a 0.4% gain. Australian shares fell but only by -0.04% with solid gains in energy and property shares offset by sharp falls in mining stocks on the back of the plunge in iron ore prices. Bond yields rose as did oil prices rose, but metal and iron ore prices fell. The $A fell as the $US rose.

Shares remain at risk of a short-term correction. As noted last week, September has on average been the weakest month of the year for US and Australian shares over the last 35 years. The US share market has fallen 5 of the last 10 Septembers and the Australian share market has fallen 7 of the last 10 Septembers. So far, the direction setting US share market has found support at its 50-day moving average but key risks relate to coronavirus, central banks slowing stimulus, the need to raise the US debt ceiling, the passage of Biden’s remaining stimulus and tax hikes, global supply constraints and inflation, and the slowing Chinese economy with credit risks around Evergrande Group. These could all result in further weakness in share markets in the near term. However, we would see this as just a correction as the likely continuation of the economic recovery beyond near term interruptions, vaccines ultimately allowing a more sustained reopening and tight monetary policy being a long way off augurs well for shares over the next 12 months.

How worried should Australia be about the 50% plunge in iron ore prices (Australia’s largest export)? Basically, alert but not alarmed. Since July the iron ore price has more than halved reflecting Chinese constraints on steel production, the slowdown in its economy and recent concerns about the flow on to construction related demand from property developer China Evergrande Group’s problems. But bear in mind that the iron ore price has fallen from levels no one ever thought it would get to and is still very high and well above cost. This will dent Australia’s national income and current account surplus and add a new blow out in the Federal Budget deficit (which along with lockdown support payments may end up closer to $150bn this year than the $107bn in the May Budget). But against this most other commodity prices are surging – including coal & gas (our 2nd and 4th largest exports), aluminium and copper – with most commodity price indexes near past mining boom levels. In fact, there is good reason to believe a new commodity super cycle (ex iron ore) has begun, which should benefit Australia.

The difficulties at Evergrande are worth watching more broadly though – as at about 6.5% of total Chinese property sector debt and 10% of its high yield offshore market its collapse and liquidation could have a systemic impact like that of Lehman Brothers in 2008 in terms of a flow on to the Chinese property and financial sectors and its economy. For this reason, a government directed restructuring is more likely but there could be a few big bumps along the way.

Coronavirus update

I gave coronavirus its own section so hopefully one day I can get rid of it!

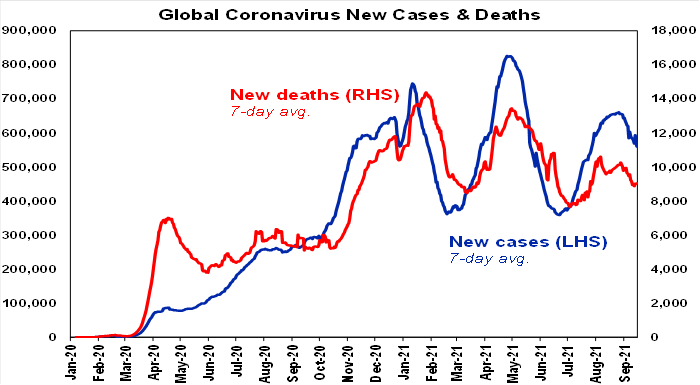

The good news is that new global coronavirus cases are continuing to decline again. (For those into charting the pattern in new cases looks like a head and shoulders – we just need to break down below the neckline!)

Asia, South America and Africa are trending down. Europe looks to have a least stabilised and the US looks to have rolled over as the surge in the lowly vaccinated South slows. China has seen some more clusters (in Fujian) but numbers are low.

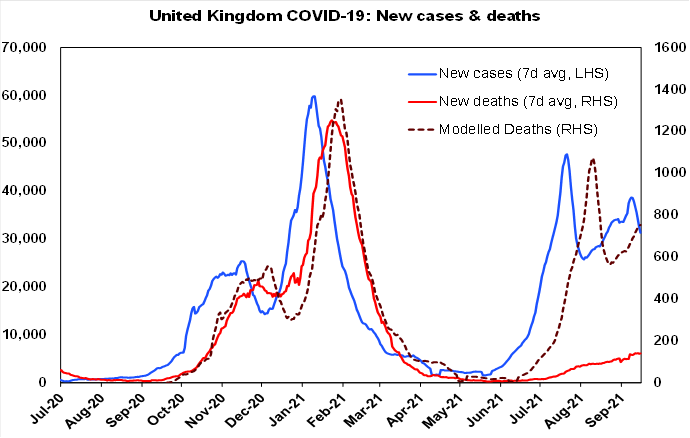

Hospitalisations and deaths remain relatively low compared to previous waves in the UK, Europe and Canada – consistent with vaccines remaining highly effective at around 90% in preventing serious illness. Deaths in the UK (the red line in the next chart) are continuing to run well below the level predicted on the basis of the previous wave (dashed line). And Israel is seeing a slowing in new cases, hospitalisations and deaths, likely helped by booster shots.

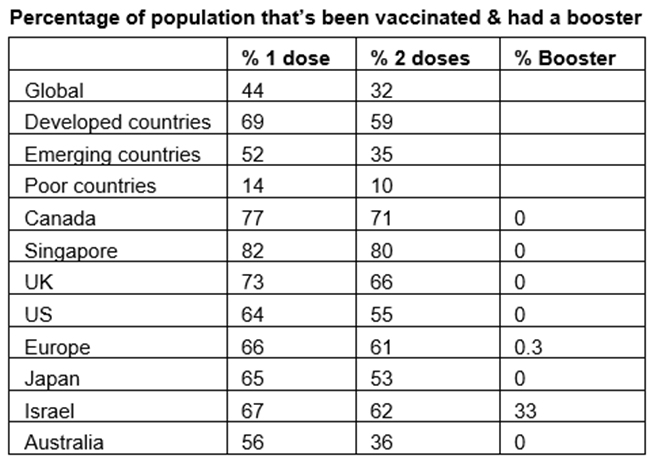

44% of people globally and 69% in developed countries have now had at least one dose of vaccine.

The main issues of concern are: the very low coverage in poor countries; that 35% or so in developed countries are still unvaccinated posing risks coming into the northern winter; the vaccines provide only around 60-80% protection against infection; indications of declining vaccine efficacy against infection after six months (particularly for Pfizer and maybe Moderna) requiring booster shots; and the risk of mutations resulting in eg a more deadly version of Delta. This all suggests it will be a long hard slog to fully get control of coronavirus and the more that are vaccinated the better. Ideally rich countries should be paying to vaccinate poor countries as it’s in their own interest to do so in order to head off mutations coming back into the rich world. Against all this though the vaccines are providing a way out in terms of heading off serious illness, booster shots are on the way in many countries and providing reopening is sensible we should be able to avoid a return to hard broad-based lockdowns.

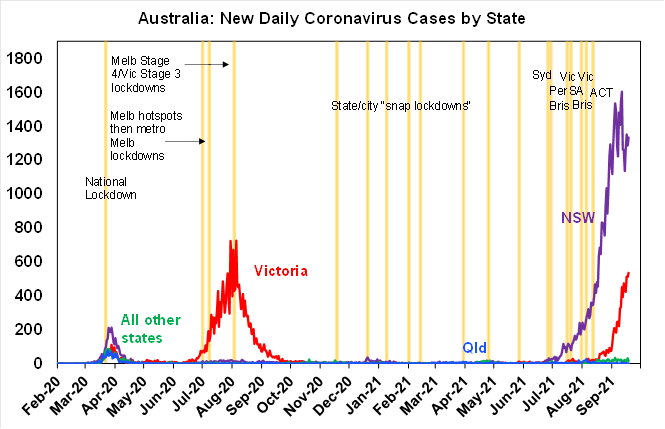

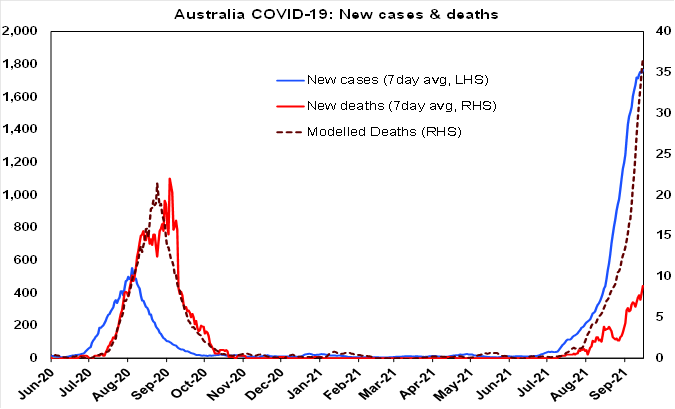

Better news in Australia - while Victoria is continuing to see a rising trend in new cases, the ACT looks to have stabilised and NSW is looking like it may have peaked helped by rising vaccinations and the lockdown. NSW’s estimated effective reproduction rate has also fallen below 1, which if sustained points to a decline in new cases.

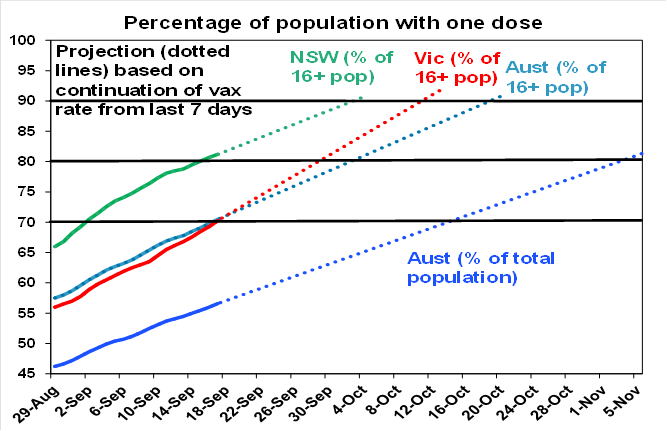

56% of Australia’s whole population has now had at least one vaccine dose. The past week saw the pace of vaccination pick up to 1.89 million people a week and with supply picking up its likely to remain high as vaccine mandates provide a powerful incentive to get vaccinated or otherwise stay at home. The next chart shows a projection of when NSW, Victoria and Australia will meet vaccination targets for one dose based on an extrapolation of the average daily vaccination rates seen in the last 7 days. Note that for first doses for those aged 16 and over, NSW is through 80%, Victoria through 70% and Australian on average through 70%.

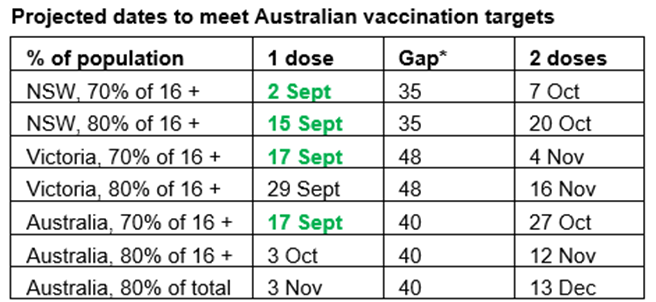

On the basis of this projection the following table shows roughly when key double dose vaccination target dates will be met based on the current lag between 1st and 2nd doses. NSW will hit the 70% of adults target around 7th October, Victoria around 4th November (although I think it will speed up from here) and Australia on average around 27th October. At the current rate NSW could hit 90% of adults with a single dose by 3rd October, with 2 doses 35 days later – given the risks with Delta this is closer to what we should be aiming for!

Meanwhile, the vaccination of older people appears to be continuing to help keep the level of hospitalisations and deaths more subdued in this wave. Deaths (the red line in the next chart) are running around one quarter of the level predicted on the basis of the previous wave (dashed line).

Other key developments

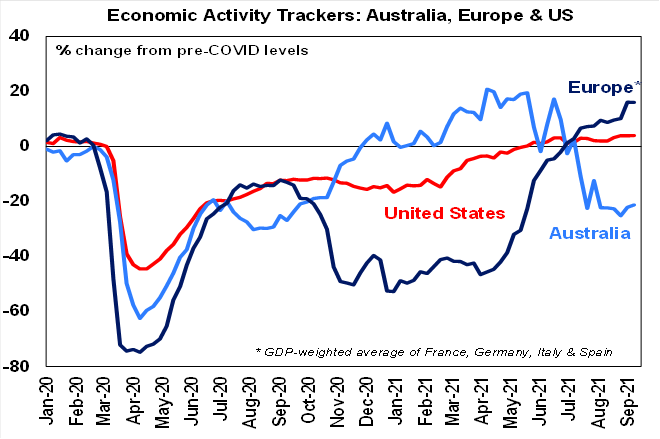

Our US and European Economic Activity Trackers have held up despite recent Delta outbreaks, with our European Tracker well above pre coronavirus levels.

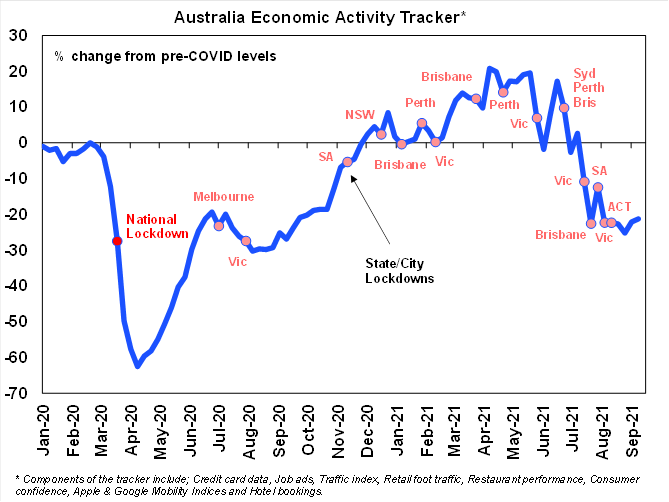

While our Australian Economic Activity Tracker is well down from its June high, it edged up again over the last week. With NSW and Victoria about as low as they are going to go, Australian economic activity has probably bottomed with reopening on track to drive the start of a recovery next quarter.

RBA Governor Lowe upbeat – but pushes back against market expectations for the start of rate hikes next year and has no plans to raise rates to cool the housing market. None of this is surprising or even new. With the Delta setback to the level of economic activity its hard to see full employment being reached next year, which means that the 3% plus wages growth necessary for sustained 2 to 3% inflation and hence rate hikes is likely still a few years away. And the RBA has to set interest rates for the average of the economy, not just the housing sector which is why last decade in the absence of being able to raise rates it used macro prudential controls to slow the property market. We think it should be doing the same again. And I tend to agree with Governor Lowe that if we want to address issues around poor housing affordability – and we should be – the way to go is through structural policies. My shopping list on this front includes: removing the capital gains tax discount; speeding up constraints on land supply; replacing stamp duty with land tax or GST; and most importantly enabling more decentralised living. Sure, low rates have enabled people to borrow more and hence pay more for housing, but lots of countries have low or even lower mortgage rates but far more affordable housing!

Should the RBA be reviewed? Calls for a review of the RBA seem to come from two perspectives – that rates have been too high (and hence the RBA has undershot its inflation and full employment objectives) or that rates are too low (which has caused unaffordable housing). These are contradictory. On the former I would have agreed two or three years ago but it has now changed its approach to be more focussed on achieving full employment and actual inflation sustained at target - so it’s fixed itself! And on housing the real issues are structural as pointed out in the last paragraph. Meanwhile there is no case to change the full employment objective, the 2-3% inflation objective is about right and adding more objectives will just make them unachievable given the limited levers the RBA has. And it communicates its views so much that to do more will just add to the noise and national obsession with interest rates in Australia. That said one area arguably could be improved – to put more monetary policy experts on the RBA Board, more people from a social perspective and maybe less business people. And no, I am not looking for a position on the Board!

America. A few years back I went to see The Beach Boys again (this was around the LTCM crisis and I needed good vibrations) and they were also performing with America who I didn’t really know much about (apart from an 80s hit called You Can Do Magic) but these guys just wheeled out one fantastic song after another. Sister Golden Hair and I Need You are my favourites. The latter is such a classic that even Andy Williams cut a version, that’s up there with the original.