2 July 2025

1300 794 893

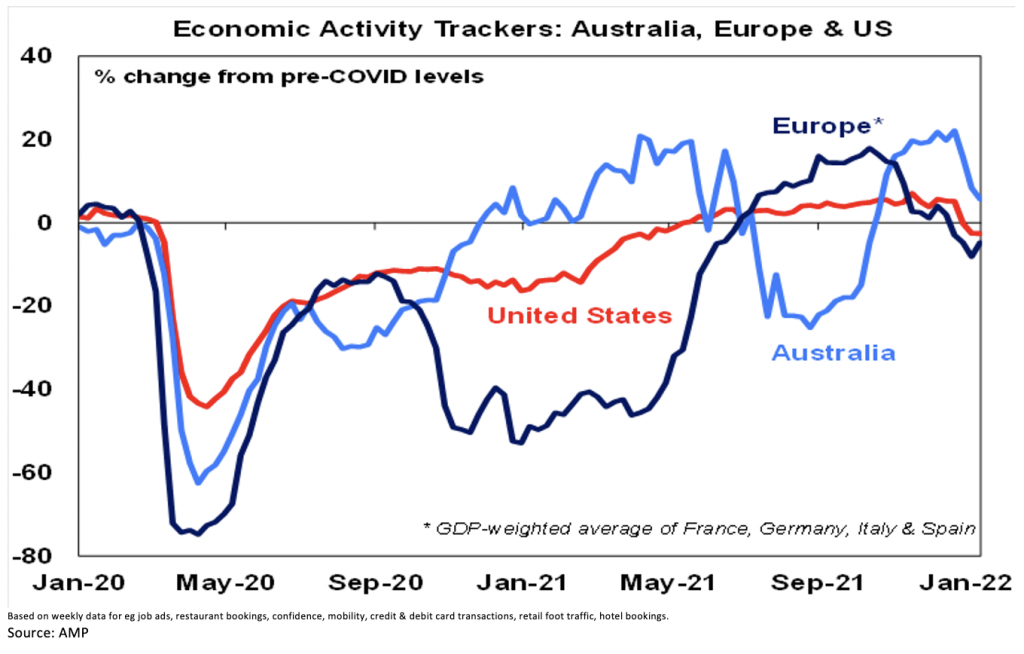

Our Australian Economic Activity Tracker fell further over the last week as the Omicron wave continued to disrupt economic activity. However, mobility has shown signs of improvement and with new cases rolling over Australian economic activity should start to improve in the weeks ahead. Our European and US activity trackers showed signs of stabilisation and improvement in the past week helped by a slowing in new coronavirus cases and are also expected to start improving.

Mixed US manufacturing data, housing strong.

US manufacturing conditions indexes for the New York and Philadelphia regions were mixed with the former down presumably as Omicron disrupted things but the latter up. The good news though is that price components in both surveys mostly fell and expectations and capex plans in the New York survey remained strong. Jobless claims rose again but with Omicron cases falling the impact is likely to be temporary.

Home builder conditions remained strong in January though and housing starts rose more than expected in December telling us the housing sector remains strong. Only 13% of US companies have reported December quarter earnings results but so far 78% of results have surprised on the upside with an average beat of 8%.

More inflation

UK and Canadian core inflation for December came in stronger than expected at 4.2% and 2.9% respectively, consistent with both countries central banks raising rates in the next two weeks. Producer price inflation in Germany rose to 24%yoy in Germany, mainly due to the surge in gas prices.

The Bank of Japan left monetary policy on hold and ultra-easy as expected consistent with inflation still around zero – core inflation was actually -0.7%yoy in December. But the BoJ did revise up its growth and inflation forecasts slightly.

Softish Chinese data, PBOC eases

While Chinese December quarter GDP growth was stronger than expected it still saw annual growth slow to 4%yoy and December retail sales growth slowed sharply. As a result, the PBOC cut various interest rates slightly – but only by about 0.1% - and signalled that further easing is likely. With Chinese growth having slowed after last year’s policy tightening, coronavirus posing a risk and inflation weak in contrast to the US, the PBOC is now in a very different point of the policy cycle to the Fed and other central banks. While Chinese growth will take a few months to pick up, with policy easing there could be support for commodity prices offsetting tightening elsewhere.

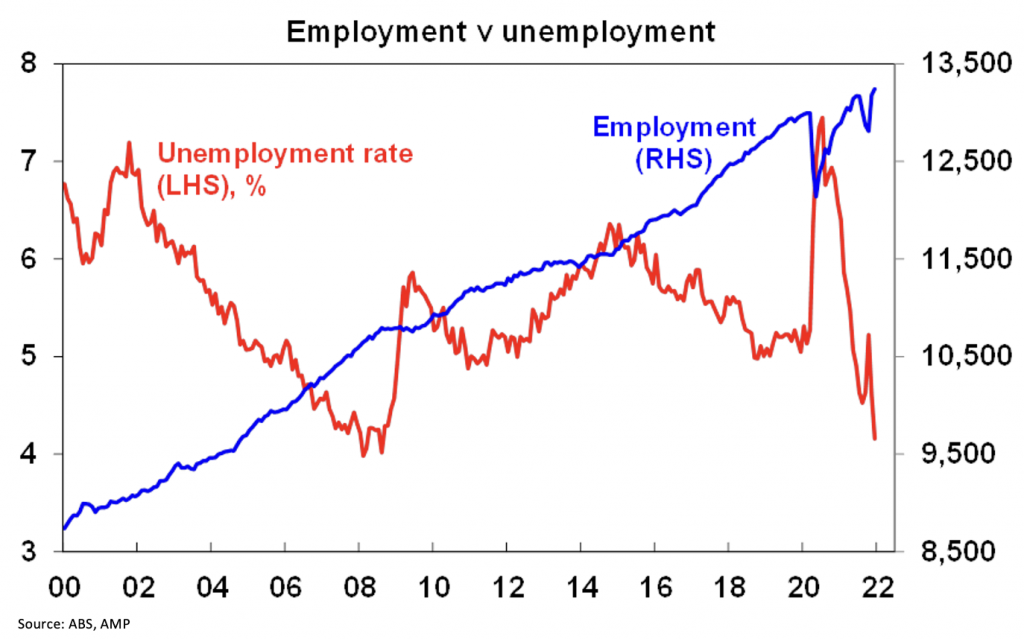

Strong jobs, but confidence down - but only a bit

The December jobs data is now a bit dated thanks to Omicron disruptions which will show up in January and February, but it showed that the jobs market was far stronger than expected at the end of last year: employment is at a record high and unemployment at 4.2% and labour market underutilisation are the lowest since 2008 and this is despite labour force participation being near a record high and above pre-pandemic levels.

While Omicron disruptions will hit employment and, much more so, hours worked in January and February, with Omicron already showing signs of peaking and employers likely keen to hang on to workers jobs market strength is likely to quickly resume pushing unemployment below 4% and annualised wages growth up to 3% in the second half of the year.

Meanwhile, consumer confidence only fell 2% in January and remains just above its long-term average suggesting only a modest impact from the Omicron wave and new house sales rose 11% in December and are well above pre coronavirus levels.

What to watch over the next week?

The main focus in the week ahead is likely to be the Fed on Tuesday which is expected to confirm the pivot to a more hawkish tone flagged in recent comments from various Fed officials with the focus shifting from boosting growth to controlling inflation. Inflation has now been above the 2% target for some time and jobs data indicates that its objective of maximum employment is likely to have been reached. While it’s not expected to raise rates, there is a good chance it will announce the end of quantitative easing this month and signal that the first rate hike will come in March followed by several more and the commencement of quantitative tightening later this year. We see the Fed hiking rates four or five times this year. The Bank of Canada also meets Wednesday and is likely to raise rates.

In Australia, the focus will be on December quarter inflation data (today) which is expected to show a 0.9% quarter-on-quarter increase pushing annual inflation up to 3.1%yoy from 3% year-on-year in September with the main drivers likely to be a 7% rise in petrol prices and a 3% rise in new dwelling costs. Underlying inflation is expected to rise 0.8% quarter-on-quarter partly reflecting bottleneck pressures in the economy which will push annual underlying inflation up to 2.4% year-on-year. This is consistent with the message provided by the Melbourne Institute’s Inflation Gauge. It’s above RBA expectations for a 2.25% year-on-year rise in underlying inflation and we expect a further rise in inflation pressures this year to be consistent with the start of RBA rate hikes in August. Meanwhile, the December NAB business survey (today) is expected to show reduced confidence on the back of rising covid cases.

Outlook for investment markets

Global shares are expected to return about 8% this year but expect to see the long-awaited rotation away from growth and tech-heavy US shares to more cyclical markets in Europe, Japan and emerging countries. Inflation, the start of Fed rate hikes, the US mid-term elections and China/Russia/Iran tensions are likely to result in a far more volatile ride than 2021, and we are already starting to see this. Mid-term election years normally see below-average returns in US shares and since 1950, have seen an average top-to-bottom drawdown of 17%, usually followed by a stronger rebound.

Australian shares are likely to outperform (at last) helped by stronger economic growth than in other developed countries, leverage to the global cyclical recovery and as investors continue to search for yield in the face of near-zero deposit rates but a grossed-up dividend yield of about 5%.

Still, very low yields and a capital loss from a rise in yields are likely to again result in negative returns from bonds.

Unlisted commercial property may see some weakness in retail and office returns, but industrial property is likely to be strong. Unlisted infrastructure is expected to see solid returns.

Australian home price gains are likely to slow with prices falling later in the year as poor affordability, rising mortgage rates, higher interest rate serviceability buffers, reduced home buyer incentives and rising listings impact.

Cash and bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.1%.

Although the AUD could fall further in response to coronavirus and Fed tightening, a rising trend is likely over the next 12 months helped by still-strong commodity prices and a decline in the USD, probably taking it to about $US0.80.

Eurozone shares fell 1.8% on Friday and the US S&P 500 lost another 1.9% as fears regarding the impact of monetary tightening continue to weigh, particularly on tech stocks with Nasdaq down another 2.7%. Reflecting the poor global lead ASX 200 futures fell 49 points or -0.7% pointing to further falls in the Australian share market when it reopens on Monday.