6 July 2025

1300 794 893

Global share markets fell over the last week, not helped by concerns about Chinese regulatory tightening, a likely slowing in tech sector earnings growth and ongoing worries about a resurgence in coronavirus cases. US shares fell -0.4%, Eurozone shares fell -0.2%, Japanese shares lost -1% and Chinese shares fell -5.5%. The Australian share market made it to a new high early in the week but ended the week flat. Bond yields mostly fell, helped in Australia by benign June quarter inflation. Oil and metal prices rose but the iron ore price fell. The $A fell despite a fall in the $US.

Risk of short-term correction

Shares remain at risk of a short-term correction or volatility as coronavirus cases rise globally, the inflation scare continues and as we come into seasonally weaker months, but surging company profits in the US and lower bond yields are providing support. And in any case, the rising trend in shares is likely to remain in place into next year as rising vaccination rates allow economic recovery to continue as interest rates and bond yields remain low.

Delta cases increase

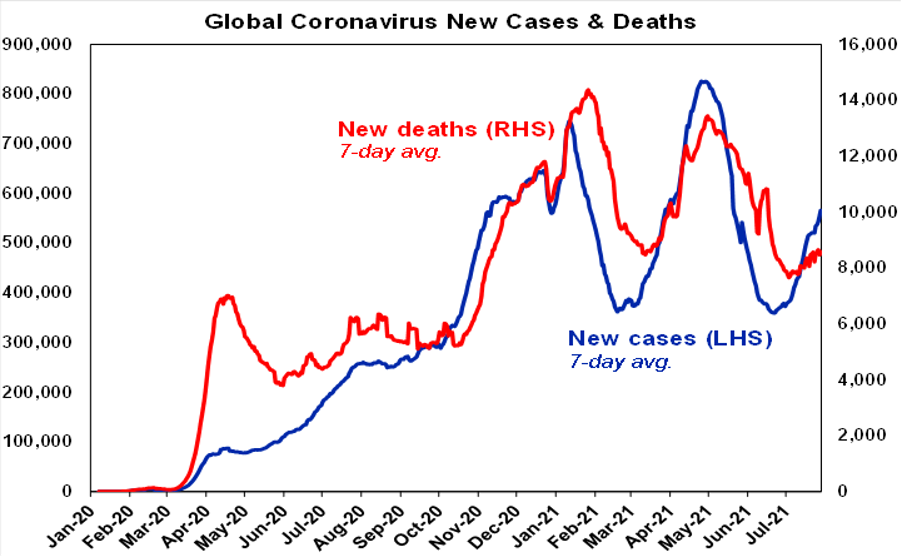

Global new coronavirus cases continued to rise over the last week, with the Delta variant being the main concern.

US infections up

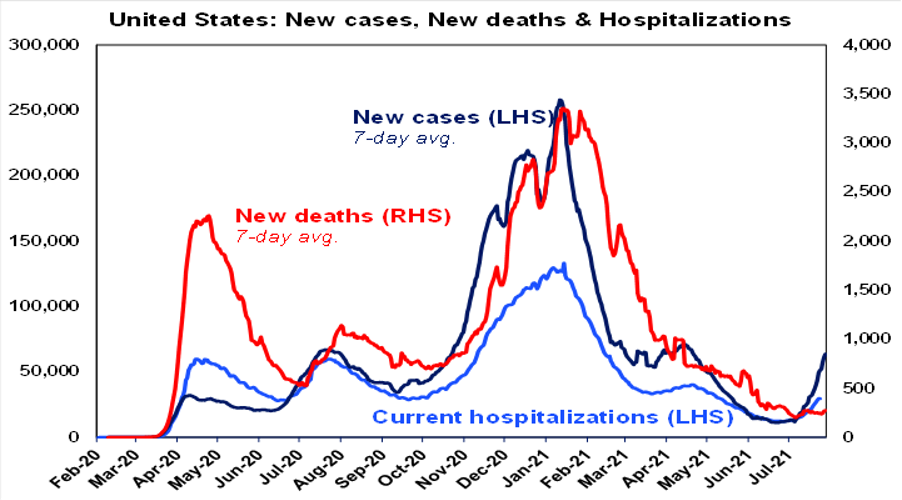

The resurgence of coronavirus in the US is now becoming more of an issue, with new cases and hospitalisations surging in many lowly vaccinated states, e.g. hospital admissions in Florida are now surpassing the peak in January, Arkansas has declared a public health emergency with its hospitals overwhelmed and Texas is running low on ICU beds. This is starting to see a return of restrictions mainly in terms of mask mandates along with delayed returns to the office along with increasing vaccination mandates for workers. The Delta variant is now accounting for more than 80% of new US cases. Even China is having problems with the Delta variant.

UK on the improve but…

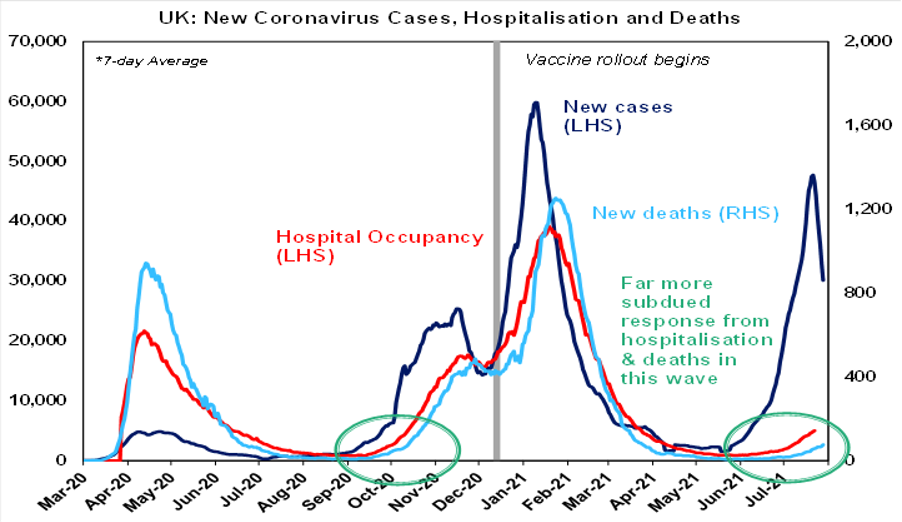

However, the UK which remains an important test case given its relatively high level of vaccination has continued to see hospitalisations and deaths remain far more subdued in the latest wave of new cases providing confirmation the vaccines are highly (90% plus) effective in preventing the need for hospitalisation and death. It’s the same story in Israel and Europe. And deaths remain subdued in the US. The UK has also seen a surprising fall in new cases, but it’s unclear whether this will be sustained or not, as the number of tests has declined but the positive testing rate is still rising and new cases have started to rise again in the last few days.

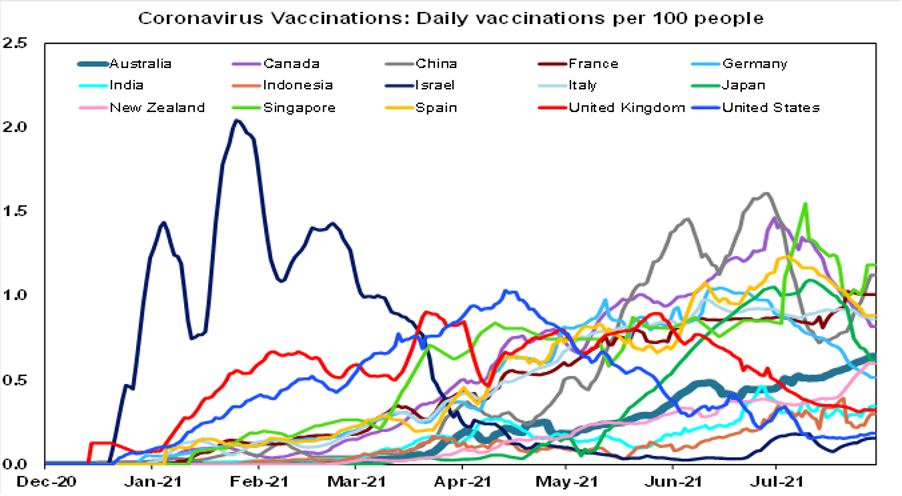

On the latest count, 29% of people globally and 57% in developed countries have had at least one dose of vaccine.

Percentage of population that’s been vaccinated

| % one dose | % two doses | |

| Global | 29 | 15 |

| Developed countries | 57 | 45 |

| Emerging countries | 31 | 12 |

| Rest of world | 9 | 5 |

| Canada | 73 | 58 |

| Singapore | 76 | 56 |

| UK | 70 | 57 |

| US | 58 | 50 |

| Europe | 58 | 47 |

| Japan | 38 | 27 |

| Australia | 32 | 14 |

Source: ourworldindata.org, AMP Capital

How is our vaccination rate?

Australia’s vaccination rate – see the thick line in the next chart – is continuing to accelerate reaching 1.15 million doses over the last week reflecting increased vaccine availability and a sharp fall in vaccine hesitancy in the face of the latest outbreaks and lockdowns. According to a Melbourne Institute Survey the proportion of the adult population that is unwilling to get vaccinated has fallen to 11.8% (just 7.6% in NSW) from 18% at the end of May. The pace of vaccination is also now reportedly rising again in previously vaccine resistant US states in the face of rising cases.

Australian governments have agreed a national plan that would see a move from the current “suppression” of the virus phase to a “transition” phase with less restrictions and less city and state lockdowns, once 70% of the adult population is vaccinated and then to a “consolidation” phase with only targeted lockdowns and greater international travel, once 80% of the eligible adult population is vaccinated. There is reason to be sceptical given we have seen a few reopening plans since the initial lockdown last year and of course new variants could throw it off. But it makes sense to tie the removal of restrictions and a transition to learning to live with the virus in the community to the level of vaccination – because it will be only once a sufficient degree of herd immunity is reached through vaccination that outbreaks don’t risk putting undue pressure on the healthcare system causing a surge in deaths. As such its only safe way to be confident of being able to return to a more normal life (and a more normal economy) without the threat of a new surge in cases necessitating an endless cycle of lockdowns.

But how long will it take?

At the rate of 1.15 million doses a week Australia should be able to reach 70% of the adult population fully vaccinated in December and 80% in January, from 14% now. If it rises to 1.5 million doses a week consistent with rising supply helped along by the adoption of carrot and stick measures to further reduce vaccine hesitancy, we should be able to reach 70% in November and 80% by year end. Of course, there is a strong argument that the targets are too low (eg Singapore has been seeing problems despite having around 70% of its adult population fully vaccinated) and that herd immunity will actually need 80% or more of the whole population to be fully vaccinated. If this is the case at the current rate of vaccination it will take us to around February assuming a sufficient portion of the population is willing.

So, we have a way to go yet. In the meantime, we have little choice but to continue with restrictions and snap lockdowns to limit pressure on the hospital system and prevent deaths following outbreaks. But the key is that the lockdowns be implemented hard and early to ensure that they are short with minimal economic impact.

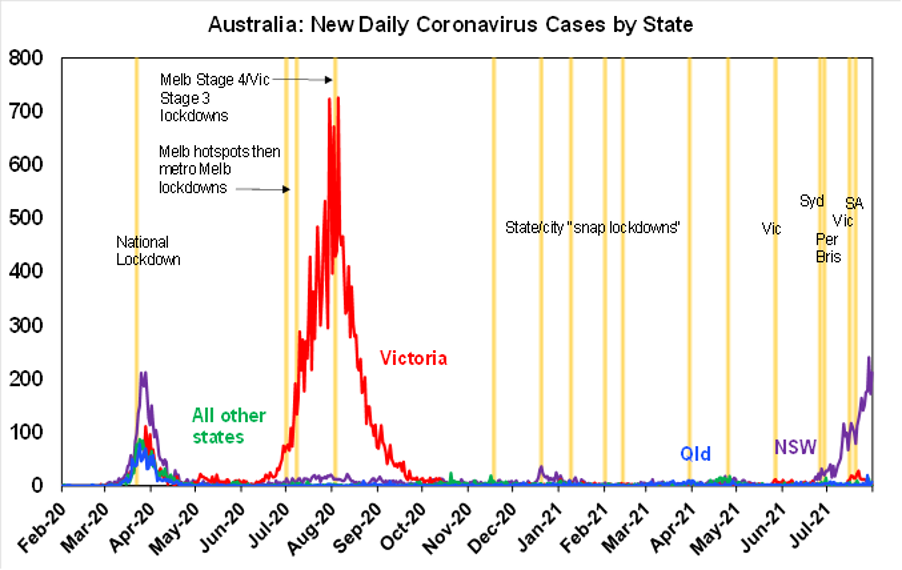

On the lockdown front in Australia, there has been good news and bad over the last week. The good news is that the lockdowns in Victoria and South Australia have worked in controlling new cases and have now ended demonstrating yet again that lockdowns that start hard and early (when new cases are running at around 1 to 10 a day) still work quickly against the Delta variant even in the absence of high levels of vaccination and so can be short with minimal damage to the economy. This has been and rightly remains the strategy in most states.

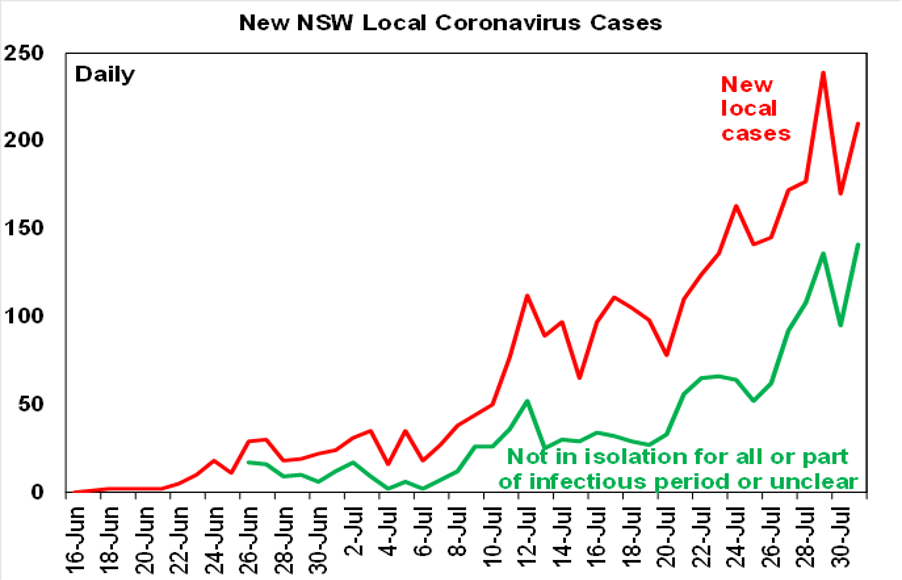

The bad news is that South East Queensland is back in a new 3-day lockdown following 6 linked local cases and new daily local cases and new local cases that are infectious in the community (however defined) rose to a new high in NSW in the past week and its lockdown has been extended for another four weeks and tightened in some hotspot areas. Unfortunately, NSW is continuing to pay the price for not going hard and early enough when it started its lockdown (although I admit its easy to say that in hindsight – but it’s worth remembering next time when a state announces a snap lockdown with just a few cases like Brisbane has just done).

Lesson for NSW

Putting that aside the message from Victoria and SA for NSW is that lockdowns still work against Delta – it’s just that having started later in terms of the flow of new cases and easier it’s now going to take longer in NSW to reach the objective of new cases that are infectious in the community being close to zero. Some modelling is pointing to September and of course the faster we can move on vaccines the more that will help too.

Our economic tracker

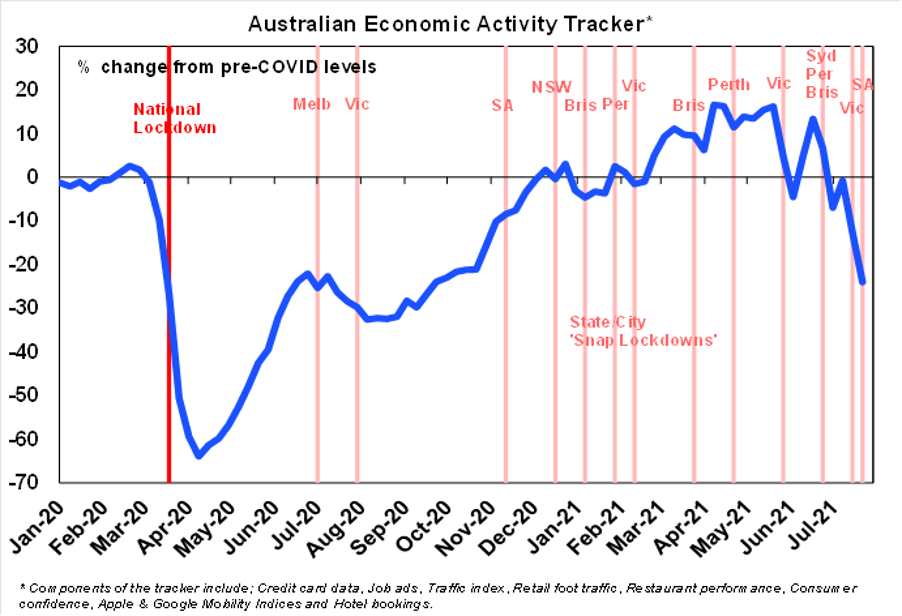

The economic impact of the lockdowns continues to be evident in another fall in our Australian Economic Activity Tracker over the last week reflecting falls in all of its components. With NSW likely having fallen about as far as it’s going to go and Victoria and South Australia reopening, it may soon bottom out if the latest Queensland lockdown is just three days and if there are no further problems in other states. Of course, that is a big “if”!

With the NSW lockdown now extended to the end of August and South East Queensland back in a three-day lockdown (which will cost around $260 million), the total direct cost of the lockdowns since end May has now been pushed out to around $14 billion and with less time to now rebound at the end of the current quarter. The further boost to government support costing about $1bn a week – with bigger payments to NSW businesses contingent on them maintaining their workforces and payments to workers who have seen their hours of work reduced by at 20 hours a week equivalent to what they would have received from JobKeeper in the middle of last year – will help but will mainly serve to enable the economy to bounce back quickly. Even though other states are likely to keep growing (helped by the ending of the Victorian and South Australian lockdowns) GDP is now expected to contract by around -2% or so this quarter. That said providing the lockdown ends this quarter (and the Victorian and SA experience highlight that lockdowns do still work against the Delta variant) we should see a strong rebound in the economy in the December quarter aided by pent up demand from another round of government support payments. This will leave growth through the course of 2021 at around 3% year on year, albeit down from our forecast prior to all the latest outbreaks of 4.8%yoy. Assuming only short snap lockdowns from next quarter and then the attainment of herd immunity through increased vaccination early next year allowing an end to lockdowns through 2022, then 2022 growth is likely to be about 1% stronger than previously expected at around 4% compensating for weaker growth this year. But that’s a long way off!

In the meantime, the set back to growth this quarter is likely to push unemployment back up to around 5.25-5.5% in August and September which will keep the RBA cautious and likely to delay the tapering of its bond buying program. Of course, the longer the lockdown drags on the great the risk of the December quarter GDP contracting too. But at this stage we continue to put the risk of a fall back into recession at just 25%. Fortunately, enhanced government support has helped offset the increased risk posed by the extension of the lockdown.

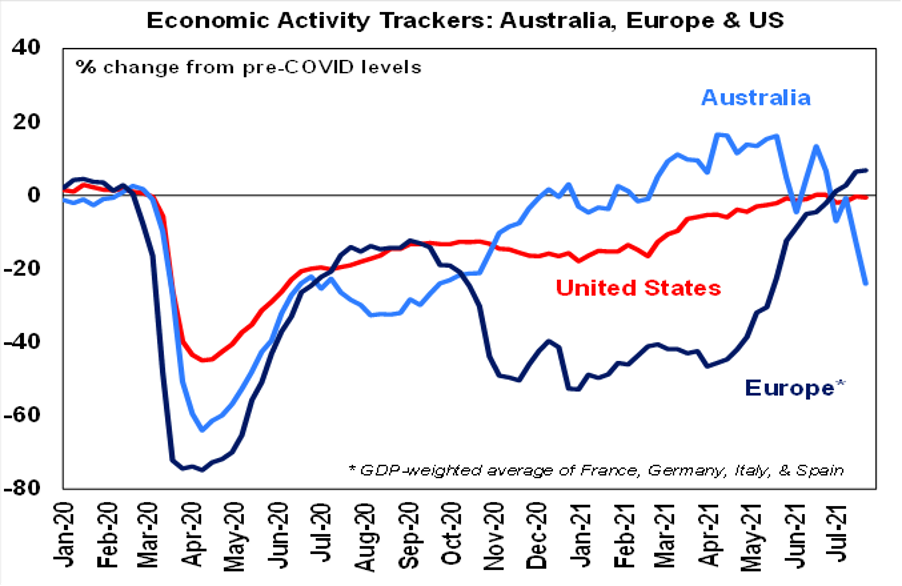

Our US Economic Activity Tracker remains little changed since May. Our European Tracker is pushing further above pre coronavirus levels. Its Europe’s turn to shine!

How big a threat is China’s regulatory crackdown? For some time, China has been cracking down hard on its tech stocks. This then moved on to private education (or tutoring) and property companies with talk it may also move on to medical services. Global investors became concerned on the grounds that it will depress the earnings of Chinese companies in which they are invested, and it also fed long held concerns that western countries might start ramping up the regulation of their own technology companies. China’s moves are consistent with a desire to ease the financial burden on lower and middle income households and to support the three child policy. They tap into an element of resentment towards mega rich moguls. They are also consistent with greater Government involvement and control in the Chinese economy which has been evident under the current leadership. But they don’t look designed to threaten long term growth and industrialisation in China. The long term nature of China’s social welfare goals indicate that the regulatory crackdown could continue for a while yet, but Chinese authorities have indicated they are aware of investors’ concerns and have moved to calm market fears, so it may take a short term pause.

More US infrastructure stimulus on the way but should we worry about the debt ceiling which expires on 1 August? Our assessment remains that argy bargy over the debt ceiling could cause investor nervousness and contribute to a correction but it’s unlikely to derail shares for long. Treasury can use various reserves to keep going into mid-September after which it will default on payments unless the ceiling is raised. As we saw in 2011 and 2013 there could be brinkmanship, but such disruptions are unpopular with voters and the Republicans are not as anti-debt as they used to be so 10 Republican senators can probably be found to get the 60 votes needed to raise the ceiling. If not, the Democrats can include it in their upcoming budget reconciliation bill and pass it with a simple majority. This will be necessary to implement the remaining $US3.5 trillion in President Biden’s American Jobs and Families Plans into law, assuming the $US550bn bipartisan deal covering traditional infrastructure is passed into law, which looks likely.

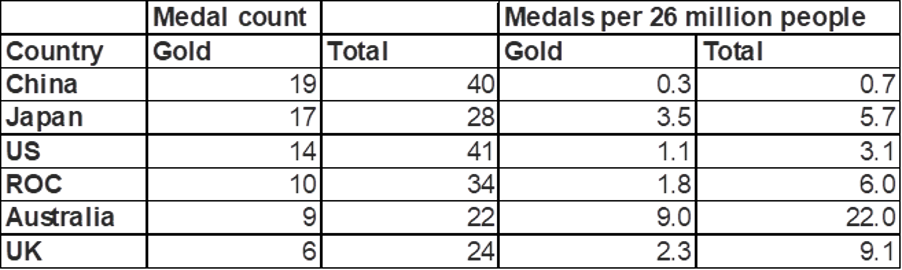

Our Olympic medal score

Australia is off to a good start at the Olympics – population adjusted it looks even better compared to the other countries in the top 6!

Olympic Medal Comparison

After the success of the 1968 NBC TV “Comeback” special (which received half of the US TV audience on the night it aired) Elvis resolved to get his career back on track. In 1969 he managed to release another 3 films – but while The Trouble With Girls was like many of his other films, Charro was a western with no songs beyond the title and Change of Habit saw a more mature Elvis with Mary Tyler Moore, resulting in one of his best films. But Elvis also made it back into serious music with sessions at American Sound Studios in Memphis resulting in such classics as In the Ghetto and Suspicious Minds and returned to live performing in Las Vegas. Two of the great songs from the American sessions were also Kentucky Rain and Rubberneckin’. The first is a rare live recording and the latter is a remix from a few years ago overlayed on his performance of it in Change of Habit.