9 July 2025

1300 794 893

Investment markets & key developments

Global share markets saw another rough week as concerns about inflation and monetary tightening intensified against the backdrop of ongoing Russian tensions over Ukraine and Omicron disruptions. However, there was a decent bounce in US, Australian and Japanese shares at the end of the week from oversold conditions helped by an Apple earnings beat.

The bounce in US shares saw them rise 0.8% for the week, but Eurozone shares lost 2.3%, Japanese shares fell 2.9%, Chinese shares lost 4.5% and Australian shares fell 2.6%. From their highs to their lows US and Australian shares have now had 10% falls, Eurozone shares have had an 8% fall and global shares have had a 9% fall.

Speculative and interest-sensitive areas have generally been hit the hardest with falls to their lows of 17% in Nasdaq, 31% in Australian IT shares and nearly 50% in Bitcoin and SPAC IPOs getting pulled. Long term bond yields mostly rose, although the rise has been capped by haven demand. Oil and iron ore prices rose but metal prices fell although they remain resilient. The USD rose further as expected Fed rate hikes increased and this saw the AUD fall.

Monetary tightening fears are continuing to intensify – led now by the Fed

The Fed left rates on hold but indicated that it will end bond buying in March, likely start raising rates in March and will then commence quantitative tightening (or QT) by letting its bond holdings run down. Fed Chair Powell’s comments pointing to a possibly faster tightening cycle than in 2015-2019 (due to higher inflation and lower unemployment) and not ruling out a rate hike at every meeting added to market nervousness, though not how high interest rates will rise. We expect the first Fed rate hike in March, four or five rate hikes this year (in line with market expectations) and QT to commence in the June quarter. QT could add to upwards pressure on bond yields – but this could be positive to the extent that it helps maintain a positive yield curve making it easier to avoid a recession.

Other central banks also moving to tighten

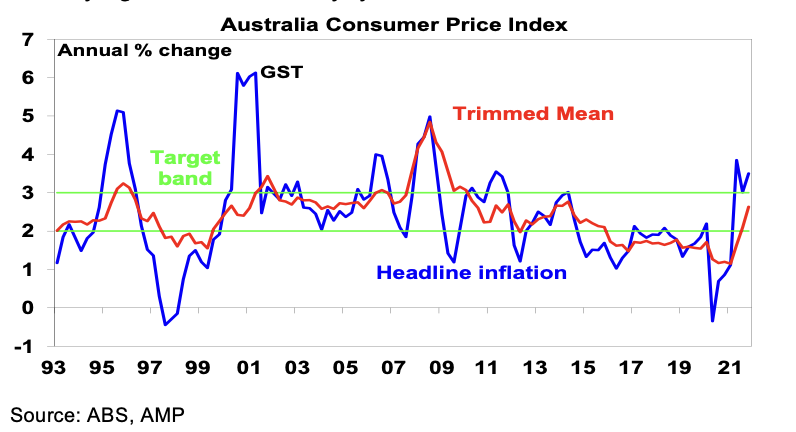

The Bank of Canada left rates unchanged but is on track to hike in March. And a rise in inflation to 5.9%yoy in New Zealand suggests its central bank could raise rates by 0.5% in February, In Australia, inflation surprised on the upside yet again in the December quarter at 3.5%yoy with sharp rises in petrol prices and new dwelling costs but broad-based gains on the back of supply disruptions and strong demand driving a rise in underlying inflation to 2.6%yoy.

Reflecting the plunge in December unemployment and higher than expected underlying inflation for the second quarter in a row the RBA will likely stop bond buying at its meeting in the week ahead and like other central banks pivot hawkish on rates. RBA forward guidance that a rate hike is unlikely until 2024, possible in 2023 but not in 2022 was based on “data and forecasts” that the conditions for a rate hike – namely inflation sustainably in the target range, full employment and wage growth of 3% or more - would not be met this year.

As it turns out, key data for jobs and inflation have been far stronger than expected and its forecasts for both will likely have to be revised up so its guidance on the start of rate hikes will have to be brought forward. Wages growth is not yet at the 3 points; something that the RBA would like to see, but unemployment is on track to fall below 4% in the second half which will push wages growth up to the desired pace in the second half and underlying inflation is now comfortably in the target range and likely to run above it.

Our base case remains for the first hike to come in August followed by another in September taking the cash rate to 0.5%. But if December quarter wages data due in three weeks shows an acceleration in wages growth or the RBA decides to ditch its focus on wages then the first rate hike could come in May or June (probably June given the RBA would prefer to avoid getting politicised in the midst of a likely Federal election campaign in May).

Don’t be too critical of the RBA

Forecasting is always hard and those in glass houses shouldn’t throw stones. Particularly in a pandemic that has blown economic data and forecasts every which way and caused massive dislocation to supply and demand. And don’t forget that the RBA’s shift to focussing on actual inflation, as opposed to forecast inflation, and to dovish guidance was designed to break Australia out of the very low inflation and low wages growth trap it has been in for the last six or seven years and for which many criticised it for being too hawkish.

And it's not as if inflation is now out of control in Australia. Underlying inflation is in the middle of the target range and headline inflation is half what it is in the US. And at 3.5%yoy, inflation in Australia is well below that in many comparable countries, viz 7% in the US, 6% in Europe, 5.4% in the UK, 4.8% in Canada and 5.9% in NZ.

How far will interest rates rise in Australia?

Given the cross currents, this will be hard to pick. But I do know that the RBA will not be on autopilot mindlessly raising rates to some level based on where rates were in the past when inflation was this high and crashing the economy and property market in the process. Very high household debt to income ratios compared to when rates last went up (in 2009-10) and particularly when inflation was last a big problem mean much smaller rate hikes will be necessary than in the past as they will now be more potent in slowing spending.

For example, the threefold increase in the household debt to income ratio since the late 1980s means a 0.25% rate hike today is equivalent to a 0.75% rate hike back then. An increase in the use of fixed-rate mortgages arguably works the other way in initially protecting borrowers who are locked in but as best we can tell they are still only around 30% of total mortgage debt outstanding so the high level of household debt is likely to ultimately dominate in constraining how much the RBA will need to raise rates.

So, the RBA will move in small increments – probably two steps at a time and pause to see what happens before doing more but rates will not rise to nosebleed levels. That said rising rates will be another factor along with poor affordability slowing the housing market this year and driving a peak in dwelling prices sometime in the second half.

Monetary tightening and the uncertainty about how far rates will rise could push shares even lower in the short term and will likely drive continuing volatility. However, we still don’t see monetary tightening this year being enough to end the economic recovery and cyclical bull market: