2 July 2025

1300 794 893

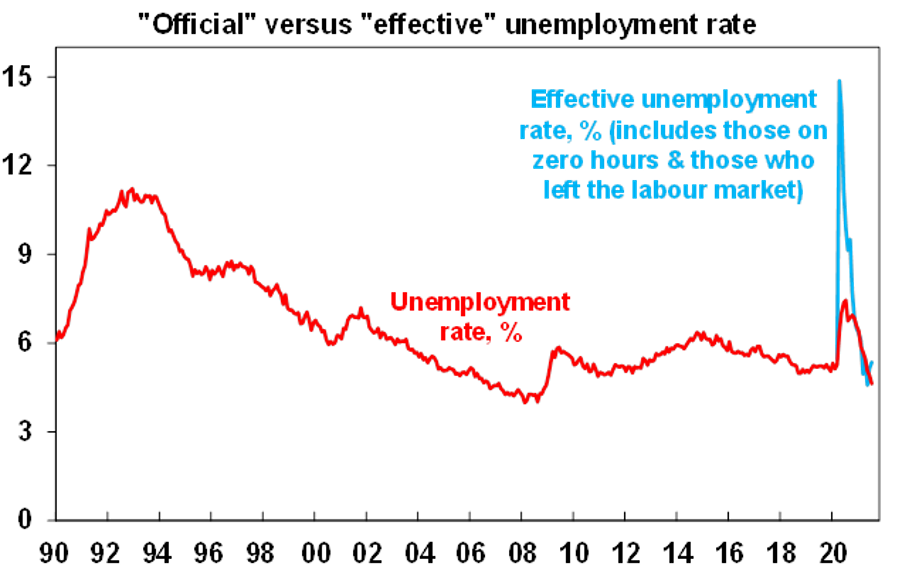

In Australia, jobs data surprised on the upside in July, but is set to fall in the months ahead, before rebounding. The timing of the July labour market survey benefitted from Victoria’s June reopening but mostly missed the impact of the NSW lockdown and Victoria’s July lockdown. Allowing for a fall in participation and an increase in those working zero hours indicates that “effective unemployment” actually rose to around 5.5%. Official unemployment is likely to rise to around 5.5-6% in August and September due to the lockdowns, but hours worked are likely to take the bulk of the hit. Meanwhile wages growth remained soft in the June quarter with only “small pockets of wage pressure” flowing from international border closures. The immediate impact of the lockdowns and the set back in the achievement of full employment means that the 3% or so wages growth necessary is still a long way off.

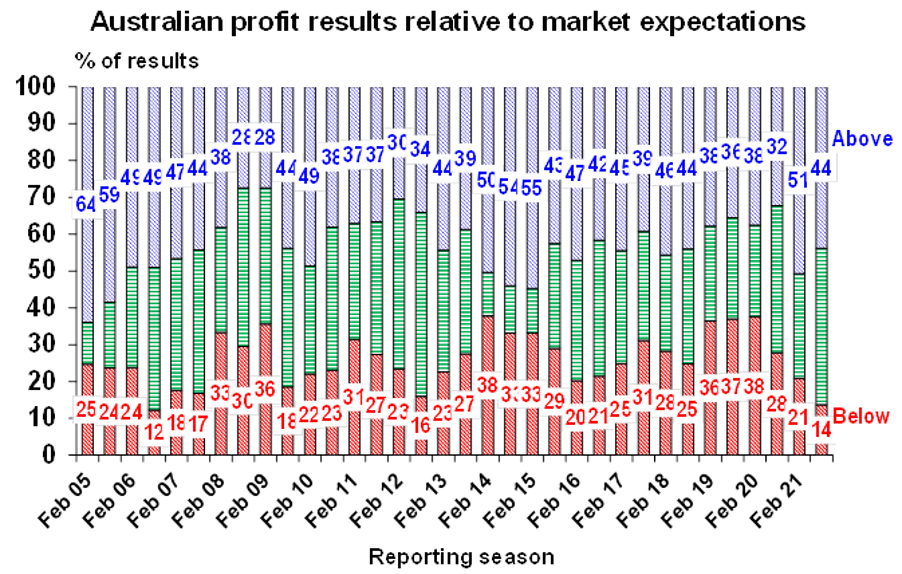

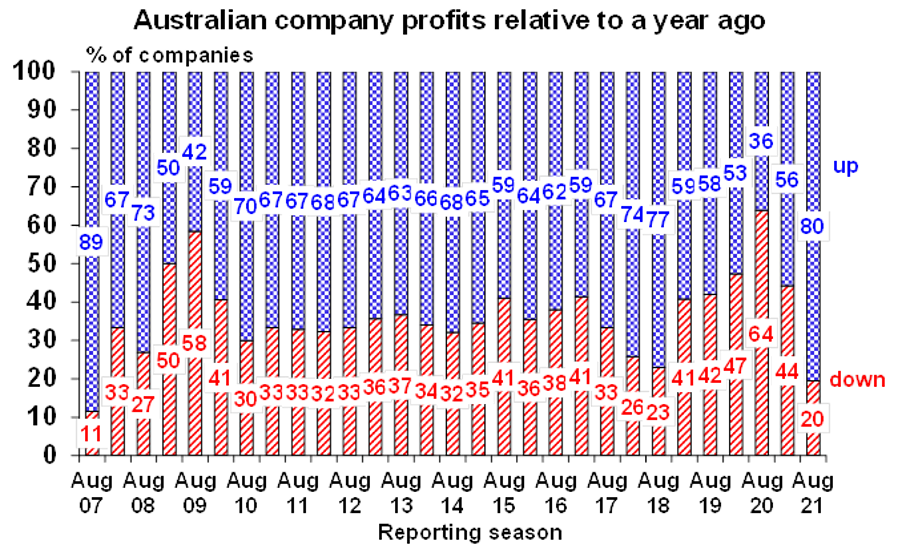

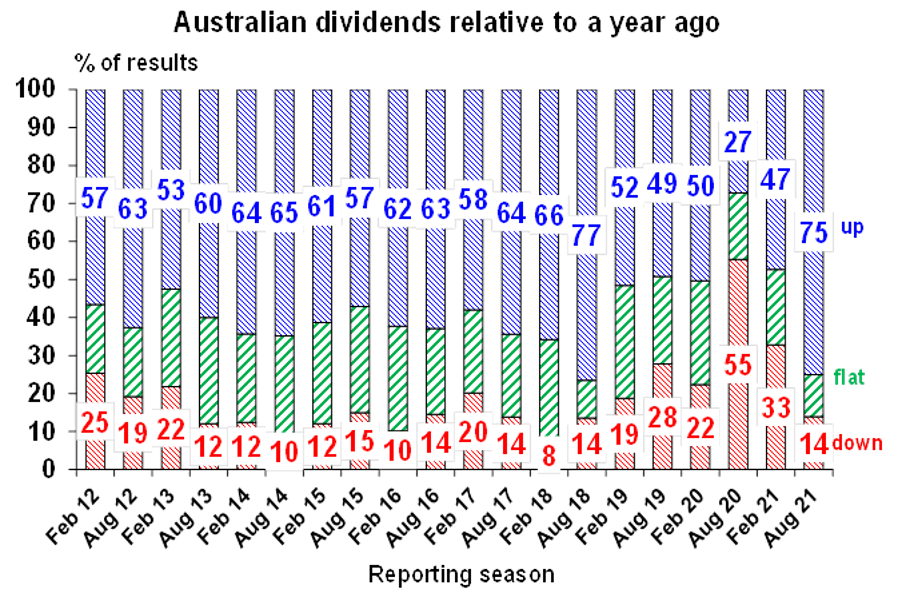

The Australian June half earnings reporting season is now about half done in terms of companies and two thirds done in terms of market capitalisation. While the lockdowns are weighing on outlook statements with many companies providing no guidance, the results have been strong. So far 44% of results have surprised on the upside, which is about normal, but 80% have seen earnings up on a year ago & 75% have increased dividends. The return of capital to shareholders will be big with dividend payments on track for a record $30bn which will exceed the August 2019 record of $27bn and adding to this is about $18bn in buybacks. Consensus earnings growth expectations for the last financial year have now increased to +50.5% from +49.1% at the start of the reporting season and those for the current financial year have only fallen from +8.6% to +8.2%. Resources are seeing a doubling in earnings and bank profits are expected to be up by nearly 60%. Dividend growth is coming in at around 57%.

What to watch over the next week

In Australia, expect lockdowns will drive a further decline in August business conditions PMIs and an 8% fall in July retail sales (Friday). June quarter construction and business investment data (due tomorrow and Thursday) are both expected to show 3% gains with construction helped by strong homebuilding and tax incentives helping capex. However, the lockdowns may impact business investment intentions to be released with the capex data.

The Australian June half profit reporting season will see another big week ahead with 100 major companies reporting comprising about 26% of the share market’s capitalisation. This includes Ansell and Boral (today), Nine, Seven and Worley (tomorrow), Blackmores, IOOF and Qantas (Thursday) and Wesfarmers and Village Roadshow (Friday). Outlook statements are likely to remain cautious given the uncertainty posed by lockdowns.

Outlook for investment markets

Shares remain vulnerable to a short-term correction with possible triggers being the upswing in global coronavirus cases, the inflation scare and US taper talk, likely US tax hikes and a debt ceiling standoff and geopolitical risks. But looking through the short-term noise, the combination of improving global growth and earnings helped by more fiscal stimulus, vaccines ultimately allowing a more sustained reopening and still low interest rates augurs well for shares over the next 12 months.

Expect the rising trend in bond yields to resume as it becomes clear the global recovery is continuing resulting in capital losses and poor returns from bonds over the next 12 months.

Unlisted commercial property may still see some weakness in retail and office returns but industrial is likely to be strong. Unlisted infrastructure is expected to see solid returns.

Australian home prices look likely to rise by around 20% this year before slowing to around 5% next year, being boosted by ultra-low mortgage rates, economic recovery and FOMO, but expect a progressive slowing in the pace of gains as poor affordability impacts, government home buyer incentives are cut back, fixed mortgage rates rise, macro prudential tightening kicks in and immigration remains down relative to normal. The lockdowns have increased short term uncertainty though.

Cash and bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.1%. The setback from Delta coronavirus lockdowns could push the first rate hike back into 2024.

Although the $A could pull back further in response to the latest coronavirus outbreaks, the threats posed to global and Australian growth and falling iron ore prices, a rising trend is likely to remain over the next 12 months helped by strong commodity prices and a cyclical decline in the US dollar, probably taking the $A up to around $US0.80 over the next 12 months (revised down from $US0.85).