1 July 2025

1300 794 893

While Japanese shares rose over the last week, US, European and Chinese shares fell on concerns about the impact of rising bond yields on equity market valuations, particularly for high PE tech stocks. Australian shares were boosted early in the week to their highest level in nearly a year by strong earnings results, but reversed course as concerns around rising bond yields weighed with the week seeing sharp falls in utilities, consumer staple, real estate and energy stocks. Bond yields rose further as did oil, metal and iron ore prices but the $A was little changed as the $US rose slightly. Crypto mania continued with more jumping on the Bitcoin bandwagon.

The bond sell off gathered pace again over the last week, raising fears about collateral damage to equity markets. From their lows in March-April last year 10-year bond yields have now increased by around 0.8% in the US and Australia. The rebound has been driven by increasing confidence in economic recovery helped by optimism that vaccines will allow a sustained reopening spurred along by policy stimulus with an emerging concern that US fiscal stimulus will cause overheating and much higher inflation ultimately forcing the Fed to tighten earlier than planned. There are several points to note:

First, it's normal for bond yields to rise in an economic recovery as investors switch out of safe haven bonds into growth assets, borrowing increases and saving declines.

Second, rising bond yields are not necessarily a problem for shares if its matched by a rise in earnings – and so far we are seeing the latter with consensus earnings expectations revised up by 12% in the US and by 8% in Australia over the last month. So far, the rise in bond yields has not been enough of a problem for the overall market – but a further rapid 50 basis points rise in yields may start to cause some problems and could trigger a correction.

Third, some sectors of the market are more vulnerable to higher bond yields – eg, tech stocks as they will see less of a cyclical uplift in earnings and trade on higher PEs.

Fourth, the Fed, ECB and the RBA all want what bond markets are worried about, ie, higher inflation – but the central banks fear that the bond market is jumping at what will be a transitory hike in inflation over the months ahead as the deflation from a year ago drops out and higher commodity prices and goods supply bottlenecks impact. So the central banks would rather look through any short term spike in inflation, and allow the recovery to use up spare capacity and generate higher wages growth before tightening – and this may still be several years away.

Fifth, we have seen several spikes in bond yields in the past – notably the 1994 bond crash and the taper tantrum of 2013 that proved temporary but still caused a rough ride for shares in the interim.

Finally, central banks are now throwing the kitchen sink at deflation and disinflation just as they threw it at high inflation in the 1980s and early 1990s. There is a good chance they will win this time ultimately resulting in a sustained rise in inflation but that’s probably still a few years away.

Overall, I am not too fussed, but bond yields could still go a lot higher in the short term before they settle down again and this could cause a correction in equities. But the big picture backdrop of still low underlying inflation and spare capacity in jobs markets combined with economic and profit recovery and low interest rates is a positive one for growth assets particularly shares and this includes the Australian share market. Meanwhile it’s kind of odd to think that only a year ago investors were worried about depression and deflation and now they are worried about overheating and inflation!

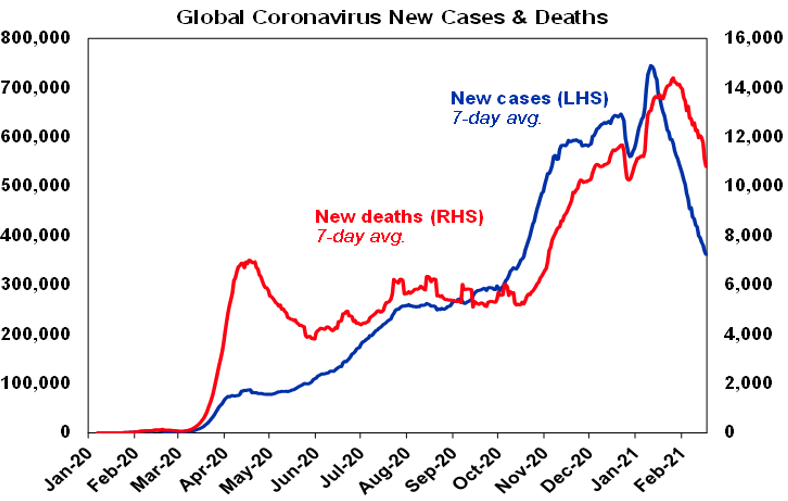

The downtrend in new global coronavirus cases continued over the last week with the daily number of new global cases running around half its January high. The decline has been particularly sharp in the US, Europe, UK, Japan, Canada and South Africa. Deaths are following new cases lower.

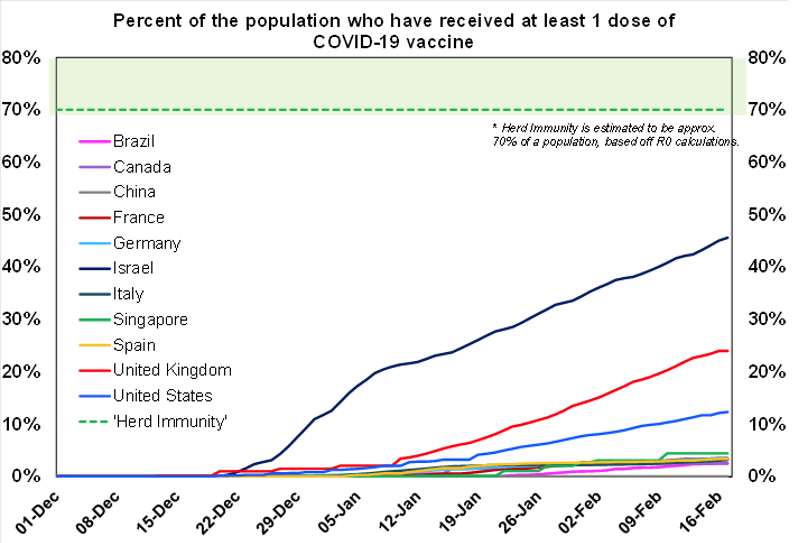

The decline in new cases largely reflects lockdowns doing their job, but the roll out of vaccines is continuing to gather pace. 46% of Israel’s population has now received one dose of vaccine, 24% in the UK and 12% in the US. While concern about new mutations remains, indications are that vaccines will still be highly effective in preventing severe cases, hospitalisations and deaths and so will still allow sustained reopening. Our view remains that the US will reach herd immunity around mid-year, most developed countries including Australia will reach it by the December quarter with most emerging countries in first half next year.

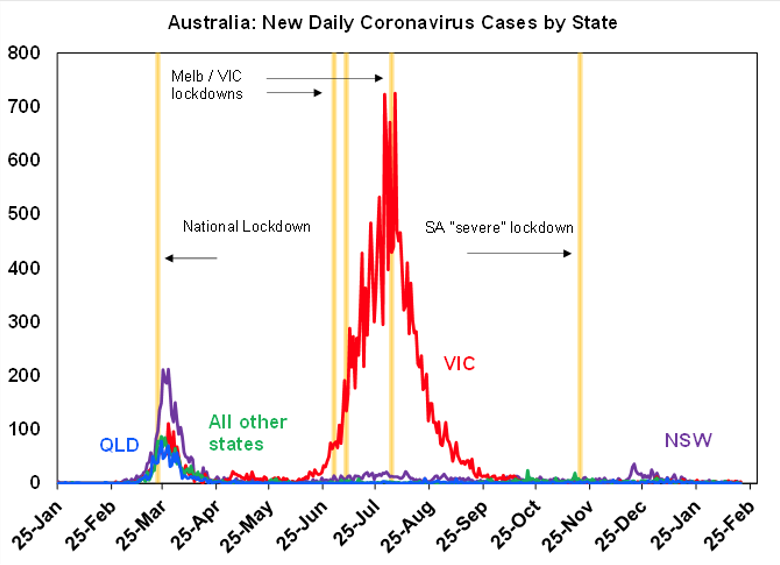

New coronavirus cases remain very low in Australia, with Victoria’s snap 5 day lockdown able to end on schedule as local transmission has been very limited. This is consistent with the experience from snap lockdowns in Queensland and WA and suggests they are working as circuit breakers and maybe that the new variants are not as contagious as feared (best to be cautious though).

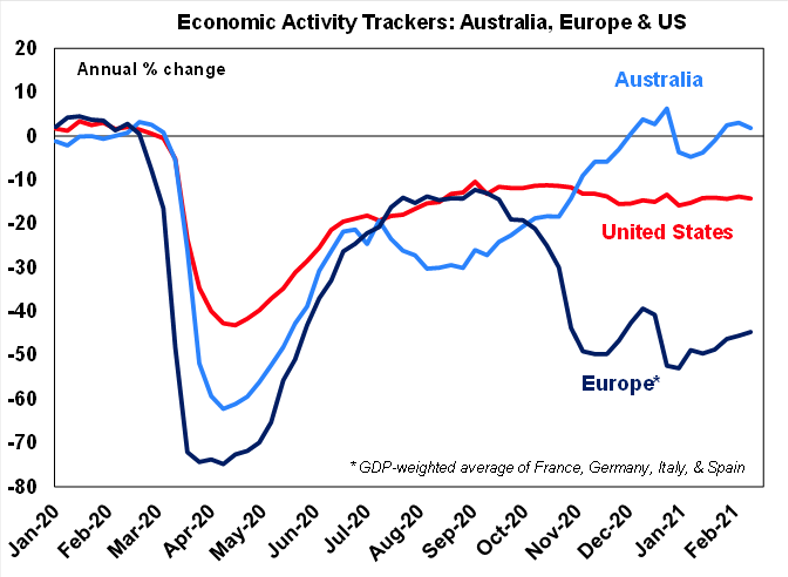

While our Australian Economic Activity Tracker dipped a bit over the last week reflecting Victoria’s snap lockdown, it remains relatively strong and is likely to resume its upswing as the lockdown was brief. Our rough estimate based on past lockdowns is that the Victorian lockdown cost the economy around $700 million – but this is likely to prove too pessimistic as 2 days were on the weekend, Australians have adapted to lockdowns such that they are now less economically disruptive and the brief nature of the lockdown would have meant less lasting damage and encouraged a strong bounce back helped by pent up demand.

Our US Economic Activity Tracker was little changed and remains softish & still down from its September high. And our European Economic Activity Tracker rose slightly again over the last week but remains very weak.

Major global economic events and implications

US data releases over the last week were mostly strong with the highlight being a 5.3% surge in retail sales in January. While it looks to have been boosted by a seasonal catch up in spending it also suggests that the $600 stimulus payments are working. Meanwhile industrial production rose more than expected, housing starts fell but this looks weather related with a surge in building permits and strong homebuilder conditions pointing to ongoing strength in housing construction and business surveys point to strong conditions in February. Jobless claims were the only real area of weakness though and warn that the jobs market is still lagging by a long way. Meanwhile a much stronger than expected rise in producer prices highlight the likelihood of a spike in the months ahead in inflation due to goods supply bottlenecks, higher raw material costs and base effects. Of course the minutes from the Fed’s last meeting reiterated that it will look through what it sees as being a transitory spike in inflation and that it will take some time for the conditions to be in place to reduce its bond buying.

The December quarter US earnings reporting season is now largely done with 85% of companies having reported and earnings running about 3% above their pre coronavirus December quarter high and 12% higher than expected a month or so ago. 79% of companies have surprised on the upside (compared to a norm of 75%) by an average 18% and 71% have beaten on revenue.

Japanese December quarter GDP rose a stronger than expected 3% quarter on quarter, but it’s still down -1.2% on a year ago and some slowdown is expected this quarter due to the coronavirus driven state of emergency. Machinery orders continued their solid recovery trend in December and Japan’s composite business conditions PMI improved slightly in February but remains soft. Core inflation jumped to +0.1% year on year from -0.4%yoy in January but this was mainly due to the suspension of the Go To Travel campaign.

Australian economic events and implications

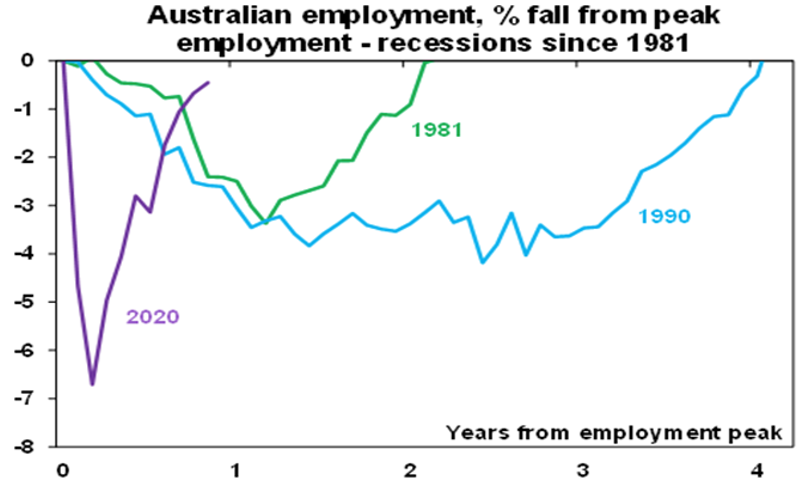

The Australian labour market continued to recover in January with employment up by another 29,000 despite various snap lockdowns, unemployment falling further to 6.4% and underemployment falling to 8.1%. So far 93% of jobs lost in last year’s national lockdown have been recovered compared to only 56% in the US. Its also been a far quicker bounce back than seen after past recessions and reflects the very different nature of last year’s recession – being due to a discreet lockdown and the massive upfront government support which enabled things to bounce back quickly.

While the jobs recovery has been faster than expected and unemployment is expected to fall below 6% by this time next year, we are still a long way from full employment and hence a decent pick up in wages growth. The experience around September/October last year that saw JobKeeper wind back from protecting 3.6 million jobs to 1.5 million jobs without much impact on unemployment indicates that the ending of JobKeeper at the end of March is unlikely to cause a major problem particularly given the collapse in the number of workers on zero hours. However, its ending may cause a brief slowing in the rate of decline in unemployment. More importantly, to get decent wages growth we probably need to see unemployment fall well below the 5% level seen before the pandemic as even back then wages growth was weak. As a result, it's still hard to see the RBA rushing into monetary tightening any time soon with the Minutes from its last meeting reiterating its dovishness.

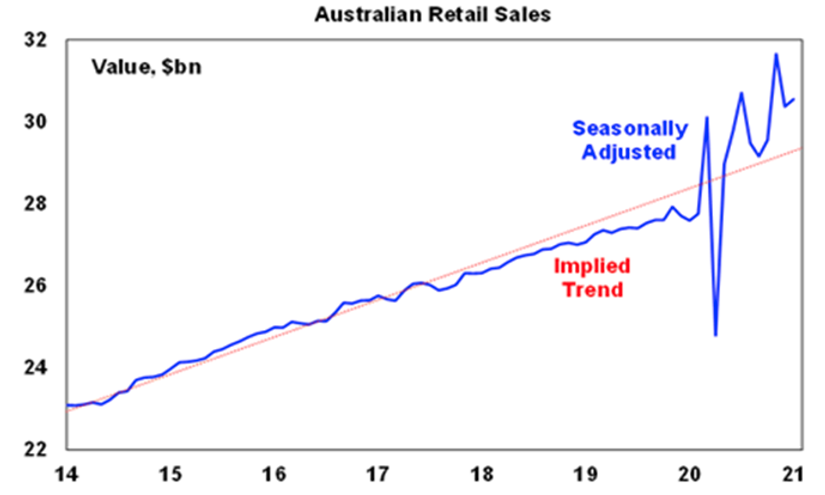

Meanwhile business conditions PMIs fell slightly in February but remain strong (with the composite PMI at 54.4) and January retail sales rose but by a less than expected 0.6%, after a -4.1% fall in December with the snap lockdown weighing on Queensland. Retail sales are still up 10.7% on year ago levels and way above their long-term trend. The combination of low interest rates, the recovering jobs market and the still high saving rate will support consumer spending but retail sales are likely to gradually move back towards trend as spending on services gradually returns to something more normal and as the pandemic related surge in household goods spending runs its course (eg the big splurge on home office stuff is likely behind us!)

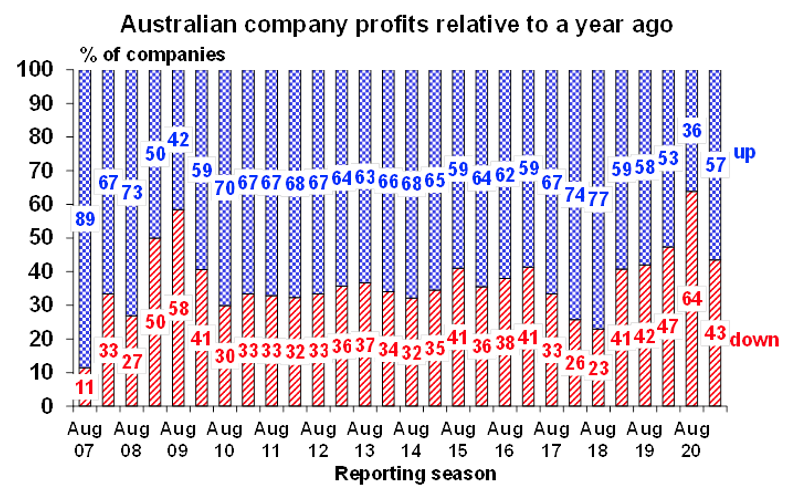

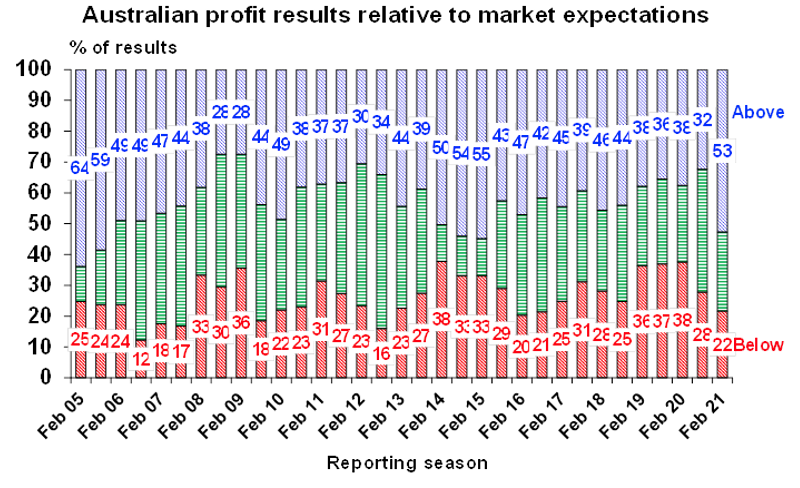

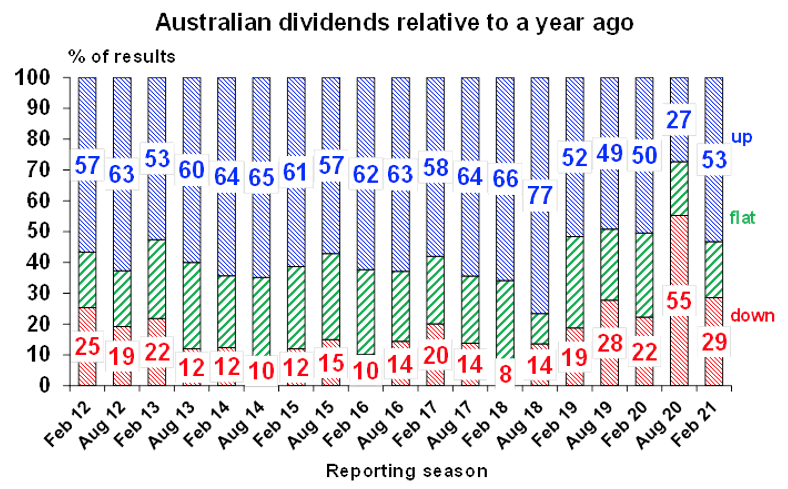

The Australian December half earnings reporting season is now about 60% complete by companies and nearly 80% complete by market capitalisation with the clear message that profits are rebounding strongly from the lockdown impacted June half last year with this driving a rapid rebound in dividends. So far 57% of companies have seen profits rise which is up from just 36% six months ago, 53% have beaten expectations compared to just 32% six months ago and 53% have increased dividends compared to 55% cutting dividends six months ago. Notably the banks have been pushing dividends back up as they reduce bad debt provisions and the big miners have announced record dividends. Consistent with the strong rebound in profits, more beats than misses and positive guidance earnings consensus expectations for earnings growth in 2020-21 has now been revised up to 29%, up from +21% a month ago. Resources companies have seen the biggest upgrades and are expected to see 50% earnings growth this year which explains the record dividends from BHP and Rio. Expected 2020-21 earnings growth for banks has now been revised up to 34%, with industrials expected to see 5% earnings growth led by IT, health, media and other material stocks.

What to watch over the next week?

In the US, expect to see continuing gains in home prices and a rise in consumer confidence (Monday), new home sales (Tuesday) and existing home sales (Wednesday) and in durable goods orders (also Wednesday).Personal income data for January (Friday) is expected to show a 10% rise reflecting recent $600 stimulus payments and a 4% rise in personal spending (Friday). Core personal consumption deflator inflation is expected to have fallen back to 1.4%yoy.

Japanese industrial production data for January (Friday) is expected to rise solidly.

The RBNZ (Wednesday) is expected to leave monetary policy on hold.