12 July 2025

1300 794 893

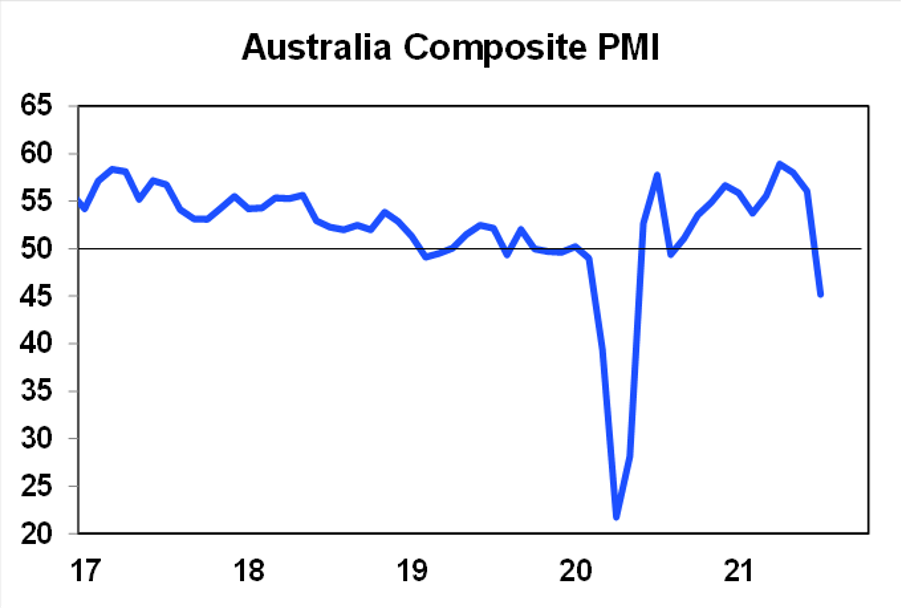

Australian business conditions PMIs fell sharply in July, reflecting the hit from the lockdowns with the services sector driving the bulk of the fall.

Australian retail sales fell -1.8% in June as lockdowns impacted various states. Despite this retail sales rose 1.3% in the June quarter as a whole but they are likely to weaken in July as lockdowns continue to hit. Meanwhile, payroll jobs fell over the two weeks to 3 July, particularly in NSW. The trade surplus widened further driven by continuing export strength.

What to watch over the next week

In the US, the Fed is expected to leave monetary policy on hold but continue the taper talk with Fed Chair Powell noting that it’s still a “ways off”. We don’t expect a formal announcement until later this year with tapering commencing at the start of next year. On the data front expect pending home sales (Thursday), solid growth in durable goods orders and home prices but a fall in consumer confidence (all today), an 8.3% annualised rise in June quarter GDP (Thursday) and reopening driven growth in consumer spending for June (Friday). June core private final consumption inflation (also Friday) is likely to be up 0.7% month-on-month or 3.8% year-on-year driven by pandemic/reopening related items as already seen in the CPI and the June quarter employment cost index is expected to show another strong rise of 0.9% quarter-on-quarter. And US June quarter company profit results will continue to flow.

In Australia, June quarter CPI inflation is expected to show a sharp rise of 0.8% quarter-on-quarter, reflecting a 7.5% surge in petrol prices, higher electricity prices in WA and some pick up in dwelling purchase prices and rents. Combined with the dropping out of the -1.9% decline in the CPI seen in the June quarter last, this will see the long-awaited spike in annual inflation to 3.9% year-on-year. Underlying inflation will likely accelerate reflecting supply constraints and strong demand to +0.5% quarter-on-quarter /+1.6% year-on-year. Producer price inflation is also likely to rise due to higher commodity prices and credit data will likely show a further pick up in housing credit (both due Friday).

Outlook for investment markets

Shares remain vulnerable to a short-term correction with possible triggers being the upswing in global coronavirus cases, the inflation scare and US taper talk and geopolitical risks. But looking through the inevitable short-term noise, the combination of improving global growth and earnings helped by more fiscal stimulus, vaccines allowing reopening once herd immunity is reached and still low interest rates augurs well for shares over the next 12 months.

Still ultra-low bond yields and a capital loss from rising yields are likely to result in negative returns from bonds over the next 12 months.

Unlisted commercial property may still see some weakness in retail and office returns but industrial is likely to be strong. Unlisted infrastructure is expected to see solid returns.

Australian home prices look likely to rise 15 to 20% this year before slowing to around 5% next year, being boosted by ultra-low mortgage rates, economic recovery and FOMO, but expect a progressive slowing in the pace of gains as poor affordability impacts, government home buyer incentives are cut back, fixed mortgage rates rise, macro prudential tightening kicks in and immigration remains down relative to normal. The lockdowns have increased short term uncertainty though.

Cash and bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.1%. We remain of the view that the RBA won’t start raising rates until 2023.

Although the $A could pull back further in response to the latest coronavirus scare and the threat it poses to global and Australian growth, a rising trend is likely to remain over the next 12 months helped by strong commodity prices and a cyclical decline in the US dollar, probably taking the $A up to around $US0.85 over the next 12 months.