4 July 2025

1300 794 893

Along with the stronger-than-expected surge in US CPI inflation seen in April, producer price inflation also rose more than expected. US economic activity data was mixed though. On the one hand, job openings rose to a record high, jobless claims fell further and small business optimism rose. But retail sales and industrial production for April were softer than expected. However, both retail sales and industrial production for March were revised up and retail sales held on to their stimulus driven 10.7% surge seen in March, remain around 15% above their long-term trend and are starting to be affected by reopening which is seeing a rotation away from goods back towards spending on services (which apart from restaurant sales which was very strong, are not really captured in the retail sales data).

The UK looks like staying together (for now) after the Scottish parliamentary election did not produce a clear win for the independence movement. The Scottish National Party did well but is one seat short of a majority and their performance was down from their 2016 and 2011 performances.

Chinese money supply growth and credit growth slowed further in April, likely as a result of the PBOC normalising monetary policy after easing last year. Producer price inflation rose to a stronger than expected 6.8% year on year, but CPI inflation was a bit less than expected at +0.9%yoy, with the rise from +0.4%yoy in March due to base effects as prices fell in April. Core CPI inflation rose to just +0.7%yoy from +0.3%.

Australian economic events and implications

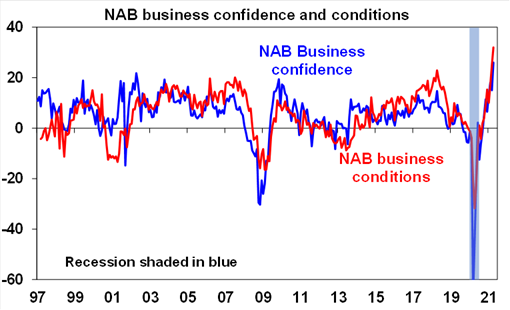

Australian data remains strong. The NAB business survey’s measure of business conditions rose to a record high in April and business confidence rose to its highest since 1994 with strong readings for most components including for forward orders, employment and investment. Payroll jobs also rose adding to evidence that the ending of JobKeeper has had a minimal impact on employment. Real retail sales fell -0.5% in real terms in the March quarter which likely reflects a combination of lockdowns as well as the commencement of a rotation in consumer spending back towards services.

New home sales fell -54% in April as HomeBuilder ended. HomeBuilder likely pulled demand forward but the boost to construction it provided will continue for a long while yet and Budget deposit based assistance schemes will provide an ongoing boost to new home demand.

What to watch over the next week?

In the US, expect housing starts (today) to fall -2% but after a 19% gain in March, the minutes from the Fed’s last meeting (tomorrow) to remain dovish and May business conditions PMIs (Friday) to remain very strong. Manufacturing conditions indexes for the New York and Philadelphia regions will also be released and will likely remain strong.

Eurozone business conditions for May (Friday) will be watched for further improvement.

Japanese March quarter GDP (Tuesday) is likely to show a contraction of -1.1%qoq reflecting the covid related state of emergency. May business conditions PMIs and April’s CPI will be released on Friday.

Chinese April data for industrial production, retail sales and investment (Monday) are likely to show some further loss of annual momentum as the favourable base effects from the pandemic lockdown drops out of annual data but underlying conditions are likely to have remained solid.

In Australia, April jobs data (Thursday) will give an initial look at the impact of the ending of JobKeeper. Given that the number of workers on zero or reduced hours in March were around normal levels, job vacancies are very strong and the number of people on welfare payments in April actually fell we see little impact other than a slowing in the pace of job gains to 15,000 leaving the unemployment rate at 5.6%. Meanwhile expect March wages growth (Wednesday) to have remained softish at 0.5%qoq or 1.4%yoy and a long way from RBA conditions for a rate hike, consumer confidence (also Wednesday) to have remained strong helped by the upbeat Budget, April retail sales (Friday) to show a 0.5% gain (with snap lockdowns continuing to have some impact and business conditions PMIs (also Friday) to have remained strong. The minutes from the last RBA meeting (Tuesday) are likely to remain dovish.

Outlook for investment markets

Shares remain are at risk of a correction with possible triggers being the inflation scare and rising bond yields, coronavirus related setbacks, US tax hikes and geopolitical risks. But looking through the inevitable short-term noise, the combination of improving global growth and earnings helped by more stimulus, vaccines and still low interest rates augurs well for shares over the next 12 months.

Australian shares are likely to be relative outperformers helped by: better virus control enabling a stronger recovery in the near term; stronger stimulus; sectors like resources, industrials and financials benefitting from the rebound in growth; and as investors continue to drive a search for yield benefitting the share market as dividends are increased resulting in a 5% grossed up dividend yield. Expect the ASX 200 to end 2021 at a record high of around 7200 although the risk is on the upside.

Still ultra-low yields and a capital loss from rising bond yields are likely to result in negative returns from bonds over the next 12 months.

Unlisted commercial property and infrastructure are ultimately likely to benefit from a resumption of the search for yield but the hit to space demand and hence rents from the virus will continue to weigh on near term returns.

Australian home prices are likely to rise another 15% or so over the next 18 months being boosted by record low mortgage rates, economic recovery and FOMO, but expect a slowing in the pace of gains as government home buyer incentives are cut back, fixed mortgage rates rise, macro prudential tightening kicks in and immigration remains down relative to normal.

Cash and bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.1%.

Although the $A is vulnerable to bouts of uncertainty and RBA bond buying will keep it lower than otherwise, a rising trend is likely to remain over the next 12 months helped by strong commodity prices and a cyclical decline in the US dollar, probably taking the $A up to around $US0.85 by year end. Eurozone shares and the US S&P 500 both rose 1.5% on Friday, as softer than expected US retail sales took some pressure off US bond yields. Reflecting the positive global lead ASX 200 futures rose 48 points, or 0.7% pointing to a positive start to trade for the Australian share market on Monday.