1 July 2025

1300 794 893

Share markets fell over the past week as US inflation data for April came in far stronger than expected, raising fears of an earlier Fed tightening, before a rebound later in the week - partly helped by softer US retail sales that took some pressure off bond yields - pared losses. So despite the sharp fall earlier in the week, US shares only fell -1.4%. Eurozone shares lost -0.5% and Japanese shares fell -4.3%. Chinese shares bucked the global trend and rose 2.3%. The poor global lead also weighed on the Australian share market after it hit a record high early in the week, although it fell back by far less given that the threat of higher inflation is a bit less in Australia than in the US and given the higher exposure in the local share market to cyclical and value stocks that may benefit from higher inflation and interest rates. For the week Australian shares fell -0.9%, and of course they missed out on a sharp rally in US shares on Friday. Bond and interest rate sensitive IT, utility, property and telco shares along with energy stocks led the declines in the ASX 200. Bond yields rose although not dramatically, and in the US and Australia they remain down from their highs earlier this year highlighting that the inflation scare had already been at least partly priced in. German bond yields look to be rapidly heading towards being above zero though on the back of the improving outlook in Europe. Oil prices rose but metal prices fell. Iron ore price rose to a new record high before declining later in the week. The $A fell as the $US rose.

After having run hard with investor sentiment becoming pretty elevated shares are vulnerable to a correction as we enter a seasonally weaker period that normally runs from around May out to September/October. The still intensifying inflation scare and the risk of a further bond market tantrum along with geopolitical risks - notably China tensions but also in relation to Israel and Iran - and possibly still more coronavirus setbacks could all be triggers. However, as we have seen over the last 12 months corrections are hard to time and beyond the short-term correction risks our broad view remains that share markets will head even higher by year end supported by strong earnings growth and central banks remaining ultra-easy. Our ASX 200 forecast for year-end remains 7200, but having almost reached there early in the past week the risk is likely on the upside. (Note in relation to the fighting between Israel and Gaza: in the past Israeli/Palestinian related conflicts, while terrible, have rarely had a significant impact on global share markets unless oil prices are impacted.)

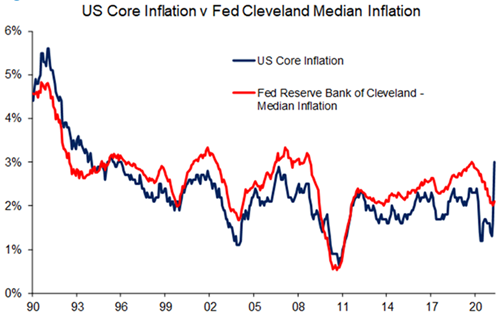

US inflation surged in April by a lot more than expected, but our assessment remains that its likely to be a confusing picture on the inflation front over the next few years, all against the likely bottoming of the long-term decline in inflation seen over the last 40 years. US headline CPI inflation surged to 4.2% year on year and core inflation rose to 3%yoy compared to expectations for 3.6% and 2.3% respectively. The key drivers were base effects as last year’s deflation drops out of annual calculations; higher commodity prices; goods supply bottlenecks as a result of cuts to production in the pandemic and then consumers switching spending to goods from services; and reopening leading to a rebound in some prices. However, reflecting the reopening and bottlenecks the surge in inflation was not broad based. Just four groups with a weight of about 12% in the core CPI accounted for around 70% of the 0.9% increase in core inflation – including used car and truck prices which rose 10%, airfares up 10% and hotels up 7.6%. The median CPI which provides a better guide to underlying inflation rose just 0.2% in April or 2.1%yoy and indicates the rise in inflation was not broad based. In the months ahead annual inflation in the US (and elsewhere) will likely push even higher as base effects have further to go, bottlenecks persist and reopening continues. And this in turn will likely drive an ongoing inflation scare pushing bond yields higher and threatening share markets (particularly growth stocks like the tech sector which has long duration earnings and so is very vulnerable to higher interest rates).

However, while the risks have increased we remain of the view that the inflation spike will prove temporary as: the base effects will drop out and then reverse; industrial production will pick up in response to the surge in prices thereby boosting supply and depressing prices; consumer spending will gradually rotate back to services and away from goods; some sectors like traditional retailing, corporate travel and CBD services will see a longer lasting hit to jobs from the pandemic; and in the US the ending of enhanced unemployment benefits in September will push more workers back into the workforce. In fact, 9 US states have already announced that will now end the enhanced unemployment benefits that are seen as dissuading some workers from returning to the jobs market. So, inflation is likely to fall back again later this year as bottlenecks and the reopening boost fade. While the Fed was likely also surprised by the April CPI, its likely to hold the line and avoid rushing into an earlier tightening and the same will likely apply at the ECB, BoJ and RBA. The likely fall back in inflation later this year combined with central banks remaining dovish will mean that any near-term inflation driven bond market panic and hit to share markets will likely to be short lived. Key to watch will be inflation expectations and wages growth.

Viewed in a very long-term context though we are likely now going through the bottoming of the long-term decline in inflation that has been in place since the early 1980s as bigger government and slower to tighten central banks focussed on pushing unemployment as low as it can go to get inflation up, a reversal in globalisation and a decline in workers relative to consumers results in higher inflation on a more sustained basis. This is ultimately what central banks are aiming for. In this context the spike in inflation now occurring is likely part of a long term or secular bottoming process for inflation and bond yields. This will take several years to play out and the question is whether it results in inflation ultimately averaging around target or something higher. Our base case is the former, although the risks are possibly swinging to the latter.

Spend, spend, spend for jobs, jobs, jobs (and to get re-elected). Five points on the 2021-22 Australian Budget.

First the additional spending of $96bn over five years was about double what I was expecting. It gave away almost all of the $104bn windfall to the budget from stronger growth.

Second, it was consistent with a trend towards fiscal policy and government more broadly playing a bigger role in the economy – this is evident in the delay in fiscal repair in order to focus on pushing unemployment below 5% and also with many of new measures resulting in baked in spending in contrast to support measures last year that were mostly temporary. As a result, government spending is projected to settle at a relatively high 26% of GDP.

Third, there is no medium-term plan for fiscal repair – but it may not be quite as bad as it looks. While the deficit is projected to decline a surplus is not expected for more than a decade. A saving grace is that the revenue forecasts may be too cautious due to conservative growth and iron ore assumptions. For example, if the iron ore price averages $US150bn per year from 2022-23 rather than $US55 it will cut nearly $25bn off the budget deficit (easily paying for the $17bn pa stage 3 tax cuts). But this would then bang up against the commitment not to let the ratio of tax revenue to GDP rise above 23.9% of GDP. So, at some stage spending cuts will likely be needed.

Fourthly, the spendathon with the only losers being non-voters (future taxpayers and foreign aid recipients) highlights that this is a pre-election budget potentially bringing forward the next election to later this year.

Finally, the key risks to the Budget are that: the extra stimulus brings forward the first RBA rate hike; rising global growth and inflation pushes bond yields back above nominal GDP growth making the new higher level of public debt less sustainable; and Australia loses its AAA rating - although this would mainly impact the national psyche with little real economic impact.

Is Australia’s recovery really dependent on reopening the international border? Angst around this got a new lease of life after the Budget assumed the border would not reopen until next year with jokes about Australia becoming a new “hermit kingdom” or “the lost kingdom of the South Pacific”. Everyone wants the freedom to travel out of and back into Australia and an open border is key to having a dynamic economy over the long term, but its short-term importance to the economic recovery should not be exaggerated. First, the economy has likely already recovered back to pre-coronavirus levels. Second, Australia normally runs a trade deficit in tourism equal to 1% of GDP as we lose more from Australians travelling overseas than we gain from foreign tourists coming here. And now, that spending by Australians is trapped here benefitting the Australian economy. Third, we normally run a trade surplus in education equal to 2% of GDP but with the pandemic we have lost maybe just half of that as many foreign students just went online. Fifth, while the loss of immigration means lower growth potential it doesn’t necessarily impact per capita GDP (and hence living standards) in the short term or recovery prospects (except for some sectors). Finally, a premature reopening before herd immunity is reached and we are confident vaccines will protect travellers from new variants, will risk reversing the recovery we have seen so far.

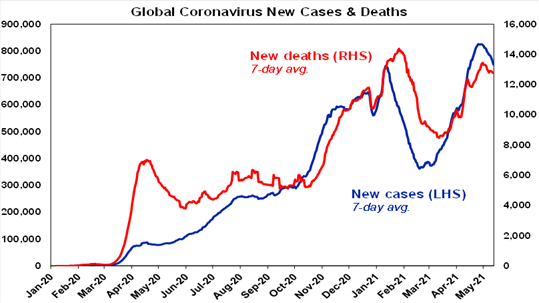

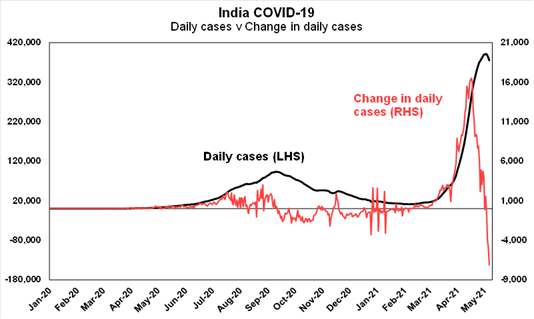

New coronavirus cases and deaths slowed further over the last week. Developed countries remain in a downtrend helped by vaccines (although Japan is a notable exception and still seeing a rising trend) and India continues to see signs of slowing momentum helped by reduced mobility.

Despite ongoing scares in relation to outbreaks from the hotel quarantine system for returned travellers, new cases remain very low in Australia.

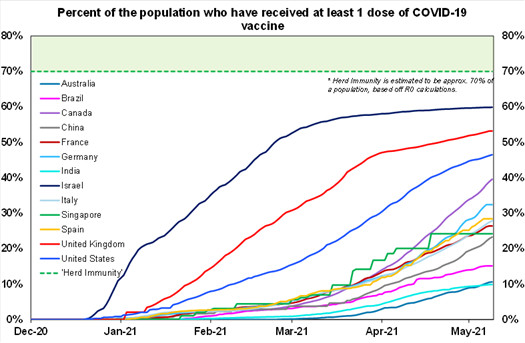

Meanwhile the vaccine rollout continues. 9% of the global population has now received one dose of vaccine, with 6% in emerging countries. Within developed countries the UK is at 54%, the US is at 47%, Europe is at 30% and Australia is at 11%. 85% of those in aged or disability care in Australia have had at least one dose and a deal for Modena to supply its mRNA vaccine starting at 10 million doses this year adds to confidence that the rollout will speed up.(It must be as I just got an invite from my doctor’s medical surgery to book for one!)The collapse in in new cases, deaths and hospitalisations in Israel, the UK and the US indicate that the vaccines work. A key risk remains in some countries of further coronavirus breakouts (eg, of the Indian variant) if reopening proceeds too quickly before herd immunity is reached. That said herd immunity may be closer in some countries than the chart below suggests if those that have already been exposed and just adults only are allowed for.

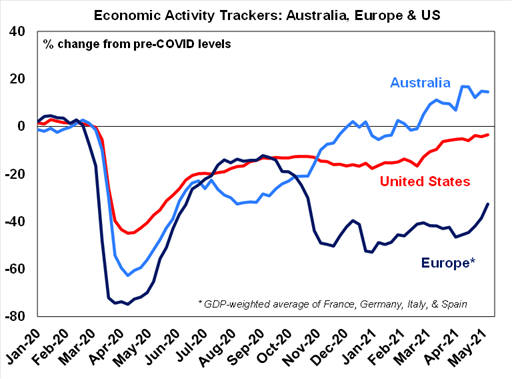

Our Australian Economic Activity Tracker was little changed over the last week and so remains very strong indicating that recovery remains on track, despite periodic coronavirus scares. Our US Economic Activity Tracker edged slightly higher and our European tracker rose again but remains very weak.

Elon Musk backflips on accepting Bitcoin. Back in February Tesla’s announcement that it had bought Bitcoin and planned to accept it as payment was a big factor adding to enthusiasm in it and propelling it higher. Now its decision to suspend accepting it on the grounds of its increasing fossil fuel use has contributed to a sharp fall in its value. Bitcoin’s massive electricity consumption, which is around that of Sweden and Argentina, and arises from the computing power necessary to mine new Bitcoins is well known - and was back in February too. But it’s not just Bitcoin – Dogecoin which was created as a joke lost close to half its value in the aftermath of Musk failing to say something positive about it while hosting Saturday Night Live. Bitcoin’s vulnerability to comments by influential individuals highlights its highly speculative nature (as it doesn’t cut it as digital cash and it’s not a capital asset providing earnings on which it can be fundamentally valued).

Amazing clips

In the past couple of weeks some colleagues have sent me some amazing music related clips. The first sees this music genius drummer Larnell Lewis listen to Metallica’s Enter Sandman for the first time and then replicate the drums perfectly. I am not really into metal (more pop for me) but I appreciate it (and love ACDC) and Larnell is just amazing. The second clip takes up back to pop with an episode of What Makes This Song Great? and breaks down Boston’s More Than A Feeling. I have never really been into Boston but this song always got my attention whenever I heard it and watching this you realise why and how it works so well and that its much more than just having a great tune and lyrics. And that’s episode number 71 so I have a lot of other episodes to get through to catch up!