6 July 2025

1300 794 893

US shares made it to a new high in the past week helped by strong earnings and good economic data. The rise was tempered, however, as Fed Chair Powell signalled some concern about elevated inflation lasting longer. For the week, US shares rose 1.6%, Eurozone shares rose 0.4% and Chinese shares rose 0.6% but Japanese shares fell 0.9%.

The positive US lead saw Australian shares rise 0.7% helped by lockdown reopening optimism. Bond yields resumed their upswing with 10-year bond yields in the US, Germany and Australia reaching close to their highs of earlier this year. Oil prices rose but metal and iron ore prices fell. The $A rose and briefly made it above $US0.75.

US concerns about inflation

Fed Chair Powell is more concerned about inflation, but the Fed, ECB and RBA are still likely to lag in removing stimulus compared to the BoE, BoC and RBNZ. Inflation risks remained the focus in the last week with more high readings in New Zealand, the UK and Canada adding to expectations for the removal of monetary stimulus or further tightening by their central banks. This followed very hawkish comments by Bank of England Governor Bailey. All of which pushed up bond yields and expectations for faster withdrawal of monetary stimulus.

However, the Fed and ECB are still likely to lag in removing stimulus: Fed Chair Powell signalled more concern about inflation staying higher for longer and confirmed that tapering will likely start next month but also said it’s not the time to raise rates as it’s still most likely that inflation will fall as supply constraints ease; ECB officials remain dovish and the departure of Bundesbank President Weidmann may add to the ECB’s dovishness; both have seen a long period of inflation undershoot prior to the pandemic; and all worry that premature tightening could just lead to a return to weak inflation once pandemic distortions to inflation fade. We expect the Fed to start tapering next month but rate hikes are probably a year or so away and for the ECB they are unlikely before 2023.

Inflation weak in Australia

At least up until the June quarter in Australia, inflation has been weaker than in the US and New Zealand. Inflation expectations have been more contained, while some sectors have seen wage inflation lift, for the majority, it appears to remain weak and the RBA minutes (while dated) remained dovish on rates. That said, the supply constraints driving higher inflation look like staying with us for a while yet and Australia’s reopening looks to be unfolding faster than expected which may bring forward the next step in the process of unwinding the extraordinary pandemic-related monetary stimulus.

After having commenced tapering, the RBA is likely getting closer to ending Yield Curve Control, i.e. the 0.1% target for the April 2024 Government bond but the first rate hike is still unlikely until 2023. In any case, higher bond yields are likely to drive further increases in fixed mortgage rates (which major banks have just increased by between 0.1% to 0.35%) and this will be another factor helping to slow home price gains into next year.

Moving forward

While the risk of a correction for shares remains – with issues around inflation and China’s slowdown likely to linger for a while – they seem to be climbing the proverbial wall of worry. US shares have made it to new highs and the relative strength of cyclical plays like copper, financials, credit spreads and the $A are a positive sign that the world is not about to plunge back into recession and augur well for a rising trend in shares over the next 6-12 months. And the period ahead is normally positive for shares into the Santa Claus rally.

Adele is back

When I first heard Adele’s Rolling In The Deep I thought she was amazing. And I reckon Skyfall is the best Bond song of recent years (although bond tunes these days struggle to match the John Barry music of the earlier Bond films and of course Live And Let Die…then again my generation might say that!). After six years Adele has a new album out, the first single of which, Easy on Me, broke single-day streaming records on Spotify. So “do yourself a favour” and check it out. Cassettes must be coming back as there is one in the video at 1.32 with a nice crackle suggesting it was taped off vinyl!

Coronavirus update

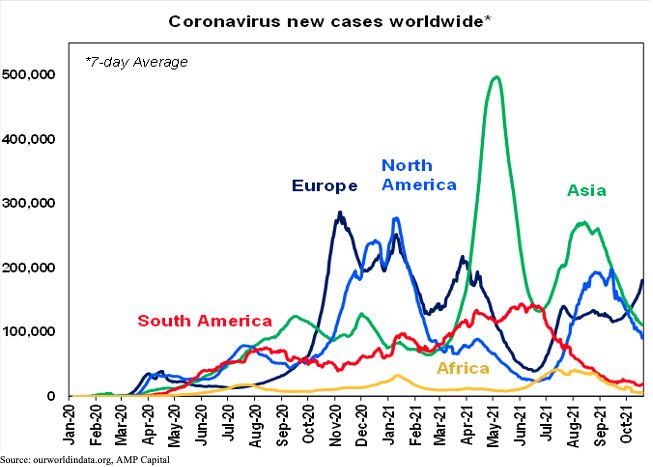

New coronavirus cases are continuing to trend down in most regions, although the UK and Europe are trending up.

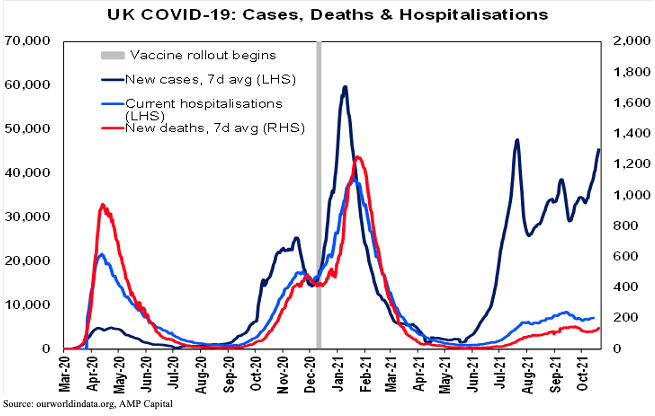

Key to watch in the UK and Europe will be hospitalisations and deaths. The UK (and Europe) may be starting to see the feared rise in new cases following reopening, the start of cooler weather, a stalled vaccine program at 68% of the UK population, fading efficacy against new infection for those vaccinated earlier this year and a slow start to boosters, and there is a new Delta variant (AY.4.2) although it’s unclear whether it poses a greater risk or not.

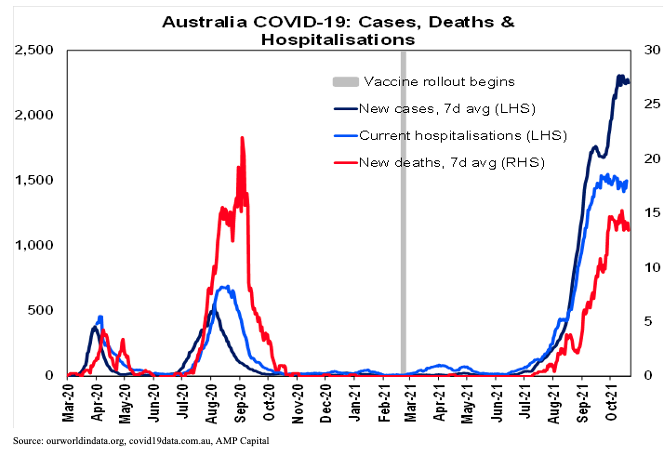

Key to watch will be whether vaccines remain successful in keeping hospitalisations manageable and deaths down as they have since mid-year. The US faces a similar risk. So far so good though. Deaths in the UK are continuing to run at less than 20% of the level suggested by the December/January wave.

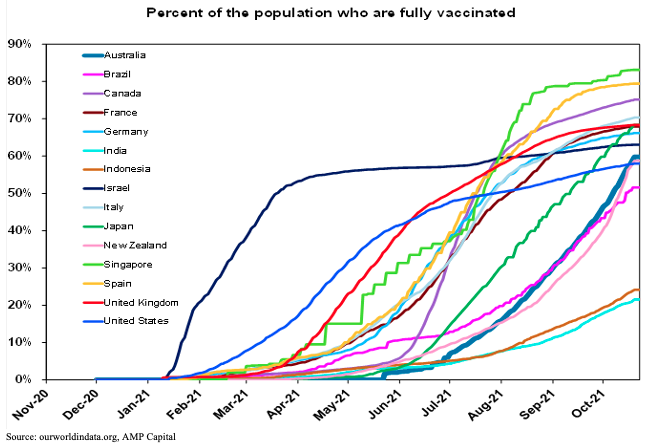

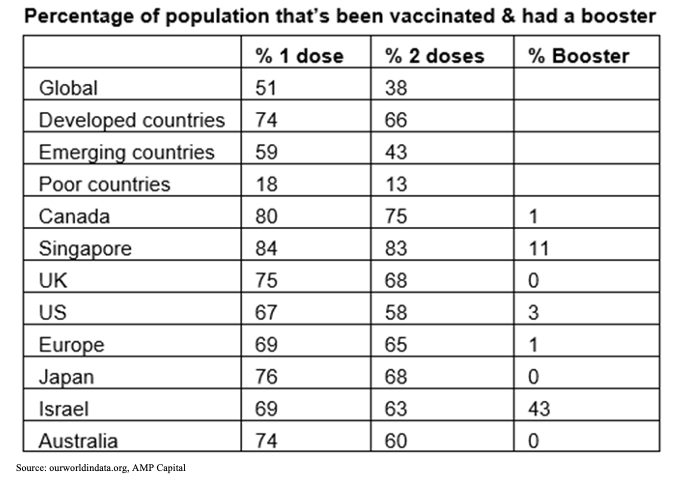

A risk remains that poor countries are lowly vaccinated which increases the risk of mutations. Singapore is perhaps the gold standard with 83% fully vaccinated and is rapidly ramping up booster shots. Following the reopening, it's still seeing over 3000 new cases a day – but it appears to have stabilised helped by the return to some restrictions and booster shots may be helping as is the case in Israel.

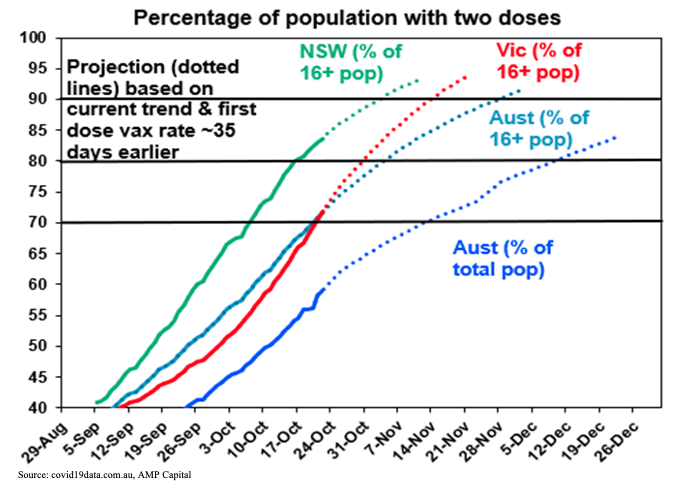

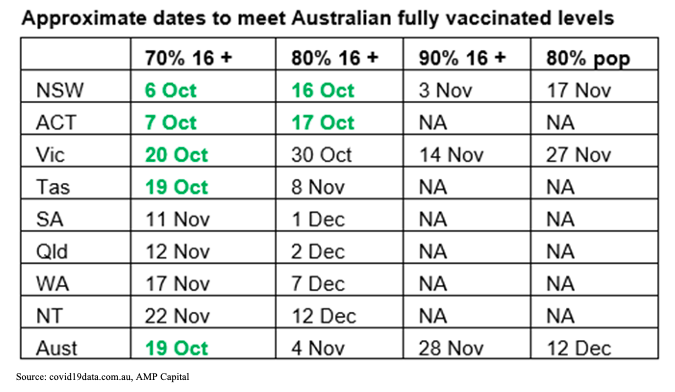

Australia is continuing to vaccinate about 1% of the population a day with 74% of Australia’s whole population now having had at least one dose, and 60% with two doses, which is now above the US. The ACT, NSW and Victoria are continuing to lead the charge helped by making vaccination a condition of participating in the initial recovery (and maybe even indefinitely in Victoria). Allowing for current trends and the average gap between 1st and 2nd doses the following chart and table shows approximately when key vaccine targets will be met.

NSW and the ACT have surpassed the 80% of adults double vax target, and Victoria will do so in the next week. Tasmania has reached the 70% double vax target and other states should do so in mid-November. On current trends, Australia will average 90% of the adult population fully vaccinated by the end of November. Booster shots are set to be available from mid-November in order to head off waning vaccine effectiveness, with Pfizer trials showing that their booster restores efficacy against infection to 95%.

Reflecting the achievement of vaccine targets, reopening is continuing in NSW, the ACT and Victoria, and Queensland has issued a plan to reopen its domestic border with key steps contingent on the achievement of vaccination targets. If anything, the reopening is so far proceeding faster than expected reflecting changes under NSW’s new premier and the faster achievement of vaccine targets.

Vaccination is helping keep serious illness down. Coronavirus case data for NSW shows the fully vaccinated make up a low proportion of cases (6%), hospitalisations and deaths in contrast to their majority share of the population and as in the UK the level of deaths is at less than 20% of the level predicted on the basis of last year’s coronavirus wave.

The main risk in Australia remains a resurgence in new cases in NSW, the ACT and Victoria after reopening - like the UK, Israel and now Singapore have seen - which threatens to overwhelm the hospital system necessitating some reversal in reopening to slow new cases down as seen in Singapore. This could particularly be a risk in the months ahead if vaccine efficacy for those vaccinated earlier this year starts to wear off before booster shots are fully rolled out.

The speed of the reopening and the sharp narrowing in the gap between doses (which can reduce vaccine effectiveness) has arguably added to this risk. Key to watch will be new cases but particularly hospitalisations and deaths – in terms of whether the hospital system is coping. So far so good – with hospitalisations and deaths remaining subdued relative to new cases compared to past waves - but it's only early days in the reopening process. Domestic border reopening in the other Australian states that have not been locked down may also be bumpy as they have a lower level of natural immunity and high numbers of cases could impact confidence as they are less used to it.

New Zealand’s move to a traffic light system to guide the transition to living with covid once 90% of those over 12 are vaccinated makes sense - because it targets a higher level of vaccination which better helps reduce the risk of coronavirus spreading and provides guidance and greater certainty in terms of what level of restrictions will be imposed depending on the pressure on the hospital system from new cases.

Economic activity trackers

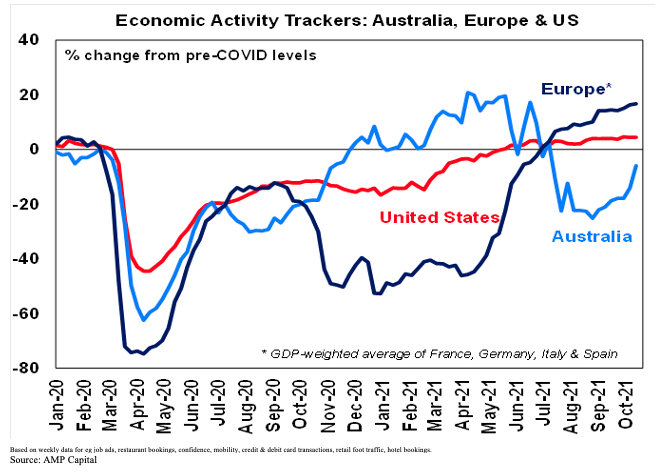

Our Australian Economic Activity Tracker rose sharply over the last week as reopening gathered pace. All components rose but notably restaurant bookings, transactions and mobility. It’s likely to move higher as reopening continues.

However, given the coronavirus numbers present in the community, which may result in a degree of consumer and business caution and the risk of a setback, this recovery may still prove more gradual in the months ahead than was the case after last year’s lockdowns but it’s likely to speed up next year as we learn to live with covid.

Our US and European Economic Activity Trackers were little changed but Europe remains stronger than the US.