27 April 2024

1300 794 893

Global share markets were mixed last week being buffeted, among other things, by the rising number of new coronavirus cases around the globe.

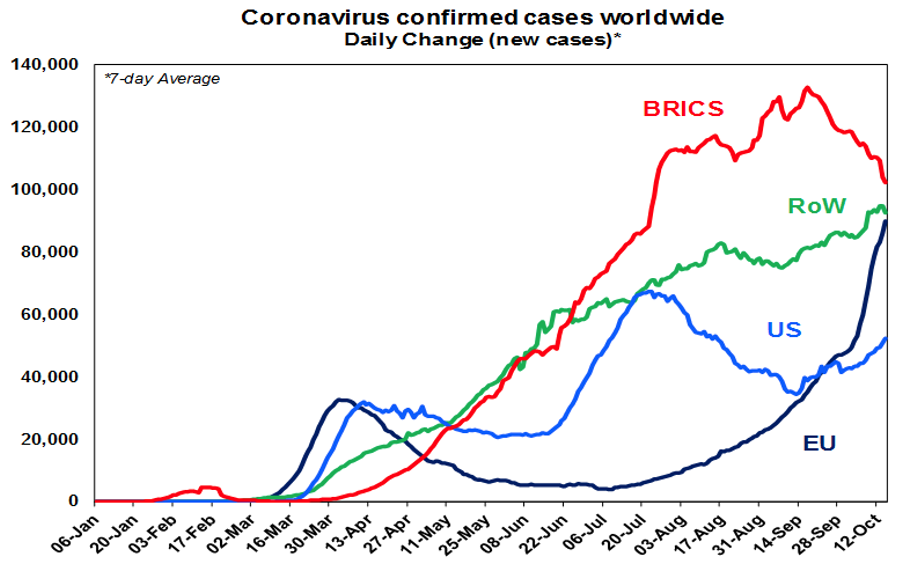

Last week saw a continuing surge in the number of new global coronavirus cases - to be now running around 350,000 a day. The latest surge is mainly being driven by developed countries – particularly Europe, the UK and Canada but with all US regions also seeing an upswing.

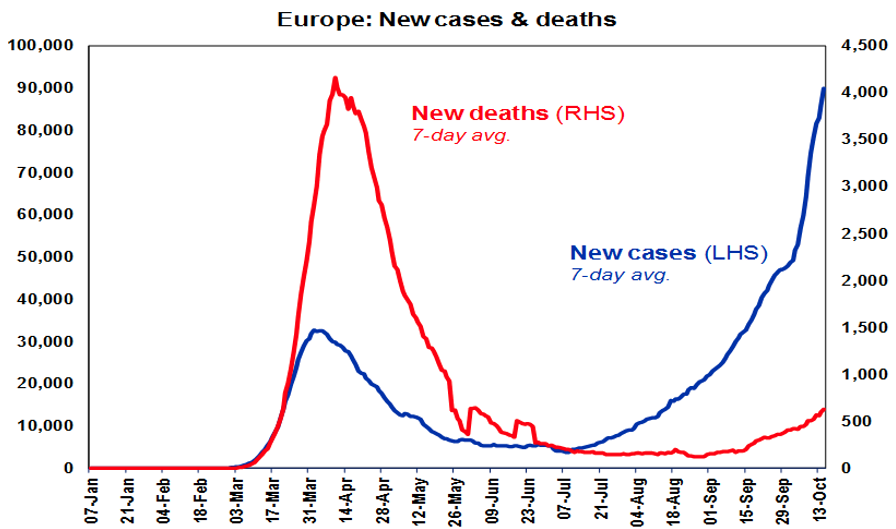

Fortunately, the number of deaths in developed countries remains well down compared to earlier this year reflecting more testing, better treatments and better protections for older people and this should help avoid a return to hard lockdowns. See the next chart for Europe.

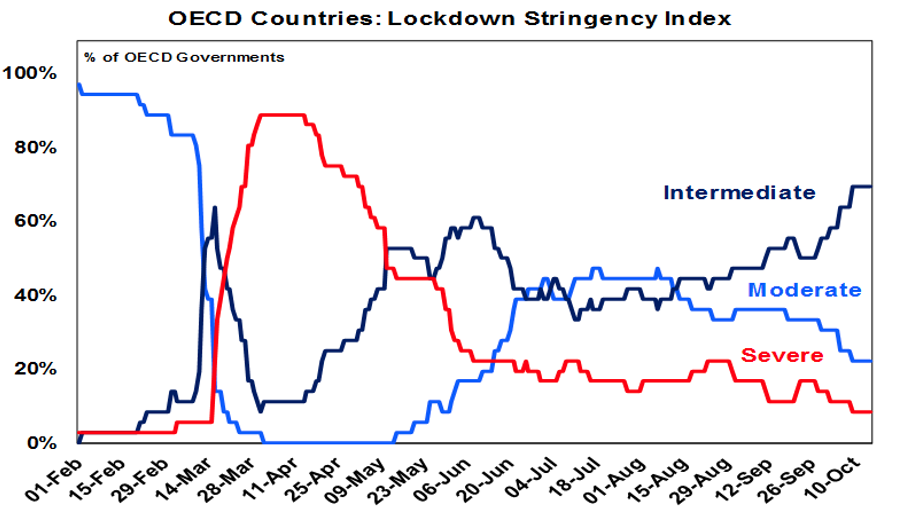

But we are nevertheless seeing a tightening in restrictions,evident in the percentage of OECD countries moving back into intermediate lockdowns, from moderate.

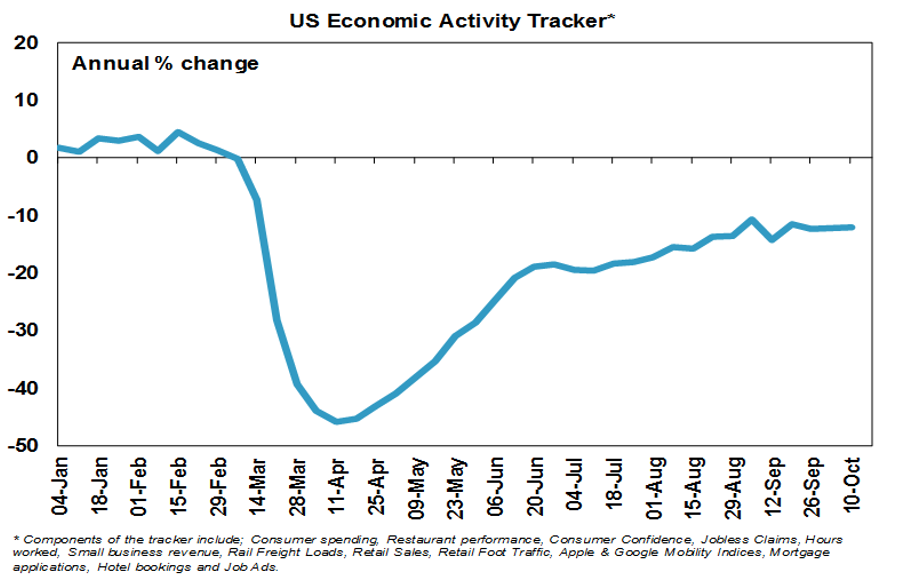

Possibly reflecting the latest rise in US cases, our US Economic Activity Tracker has been flat for several weeks now,suggesting the US recovery may be stalling again.

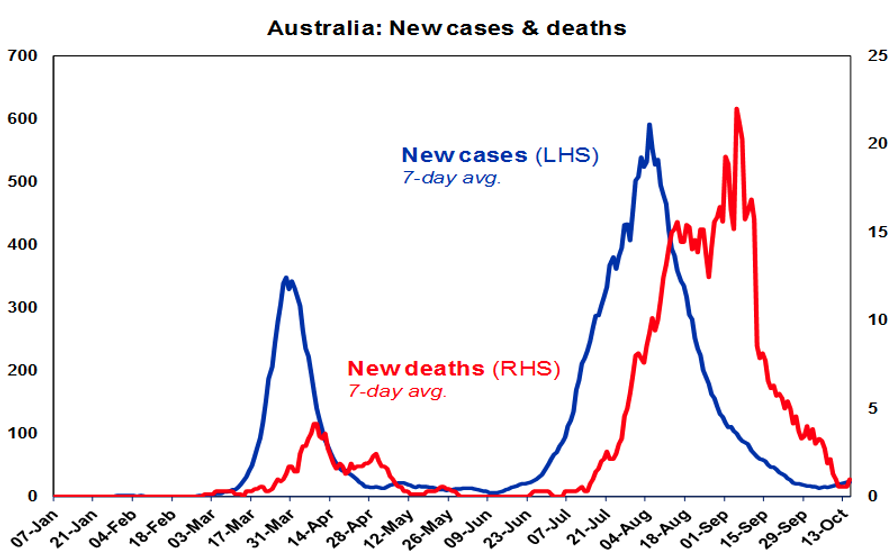

Australia is seeing new coronavirus cases remaining low and deaths have fallen.

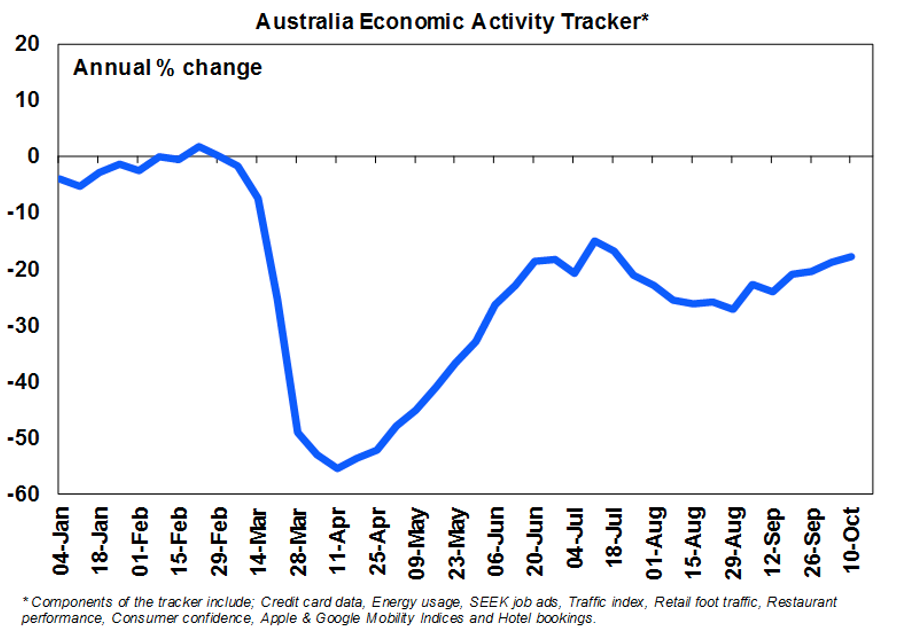

The decline in new cases has seen our Australian Economic Activity Tracker continue to hook up from August lows with gains over the last week in consumer confidence, restaurant bookings, traffic, retail foot traffic & credit card transactions. Expect the trend to remain up as Victoria gradually reopens and other states continue to recover.

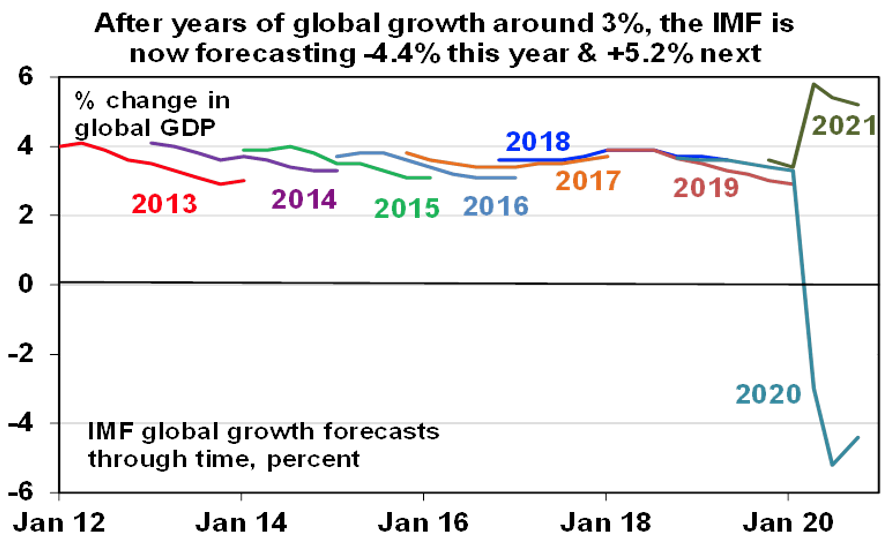

While the IMF revised up its 2020 global growth forecast to show a -4.4% contraction it revised down its 2021 forecast to 5.2%and noted the recovery will be prone to setbacks until coronavirus is tamed - we have heard that before!

On the housing front continuing strength in new home sales in September confirm that HomeBuilder and other incentives to buy or build new homes are working – but note that arrivals data for September confirm that net immigration is starting to go negative.

Finally, reports suggest that China has stopped coal orders from Australia. This could be a temporary move similar to what occurred last year, or it could be reflective of a continuation of the political tensions between the two countries. Australian coal exports to China amount to around 0.7% of Australian GDP, just above education. Hopefully, it’s resolved soon rather than allowed to spread further to iron ore and other products.

What to watch over the next week?

Outlook for investment markets

Eurozone shares rose 1.4% on Friday, but the US S&P 500 ended flat despite an initial 0.9% rally on the back of strong retail sales data was reversed as tech stocks fell on options expiries and House Speaker Nancy Pelosi said that the divide remains wide on fiscal stimulus. Despite the flat US lead ASX 200 futures rose 39 points, or 0.6%, pointing to a positive start to trade on Monday.