13 July 2025

1300 794 893

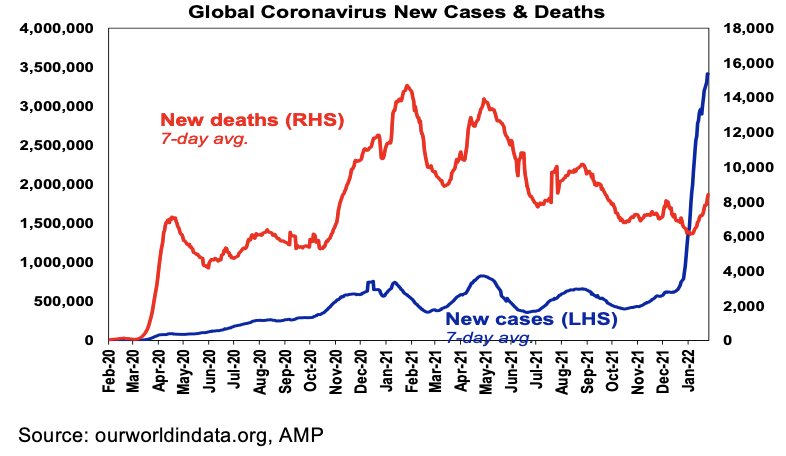

The Omicron wave has seen new global cases surge again over the past week.

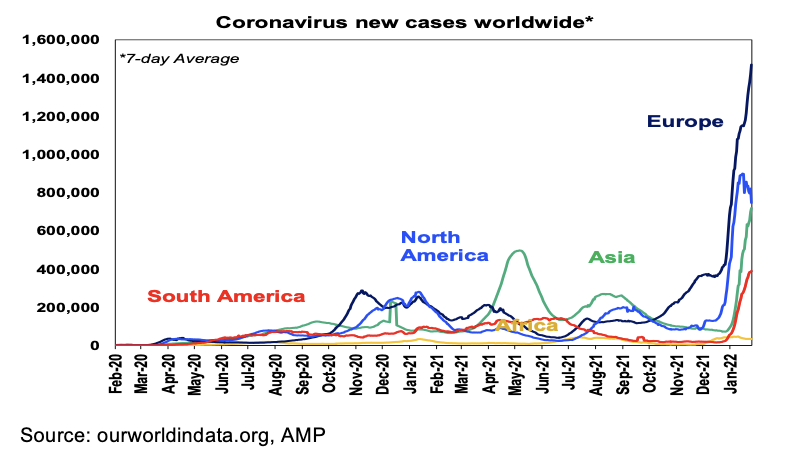

While the UK, US, Canada and Australia have seen new cases slow consistent with South Africa’s Omicron experience, Europe has seen a new leg higher which appears to be due to a new Omicron subvariant (BA.2) which may be more transmissible than the original Omicron (BA.1) but does not appear to be more harmful.

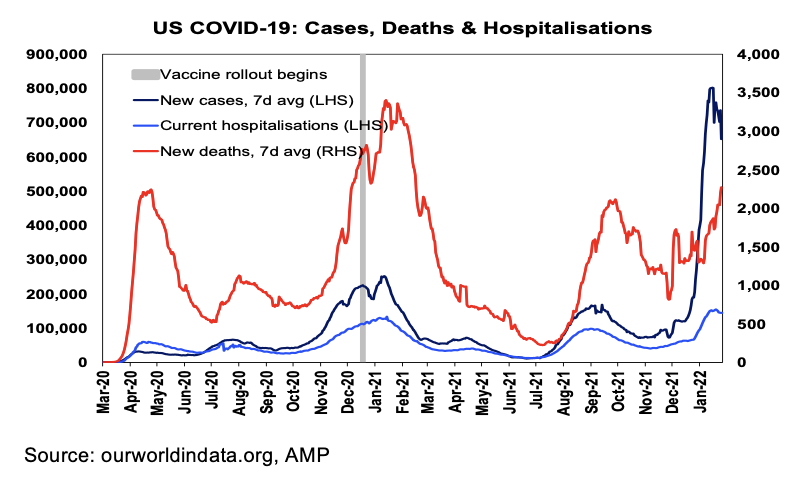

Fortunately, while deaths and hospitalisations have increased reflecting the surge in coronavirus cases they remain subdued relative to new cases compared to prior waves. This is evident in most developed countries – even the US as shown in the next chart where the lower vaccination rates are providing less protection than in other developed countries. It likely reflects a combination of protection against serious illness provided by prior covid exposure and vaccines, better treatments and Omicron being less harmful.

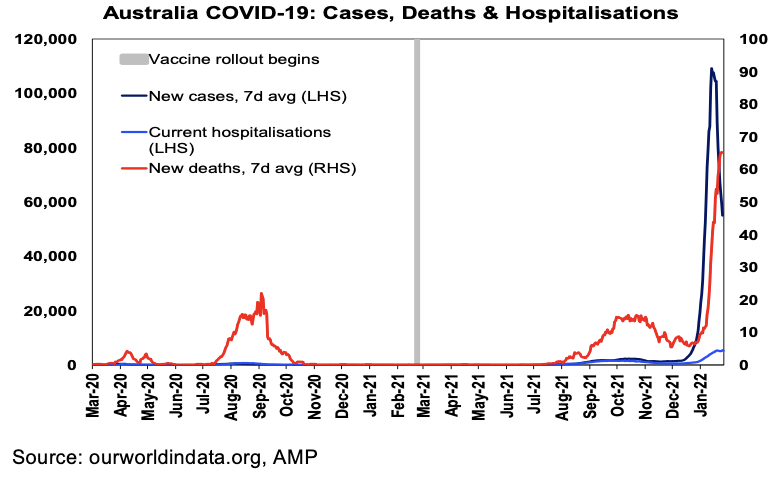

Australia is continuing to see a declining trend in new cases and the proportion of cases suffering serious illness remains low versus prior waves. Hospitalisations and deaths are showing signs of peaking and follow new cases with a lag.

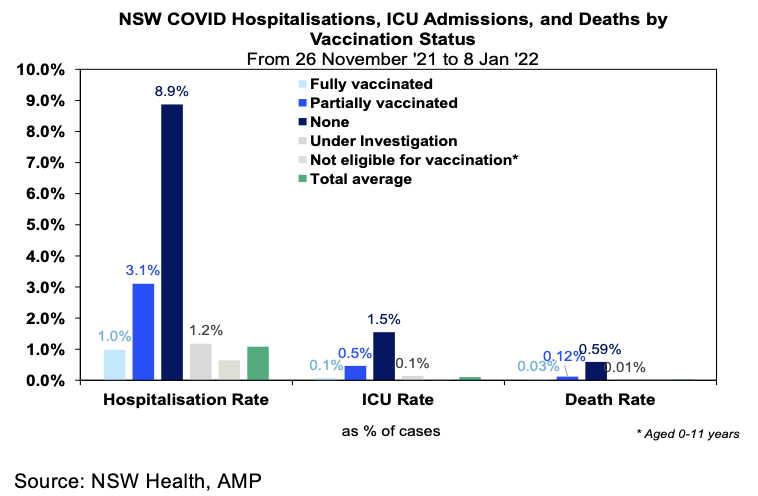

Vaccines are continuing to provide protection against serious illness.

Data from NSW shows that the unvaccinated are nearly 9 times more likely to end up in hospital, 15 times more likely to end up in ICU and nearly 20 times more likely to die with covid than a fully vaccinated person.

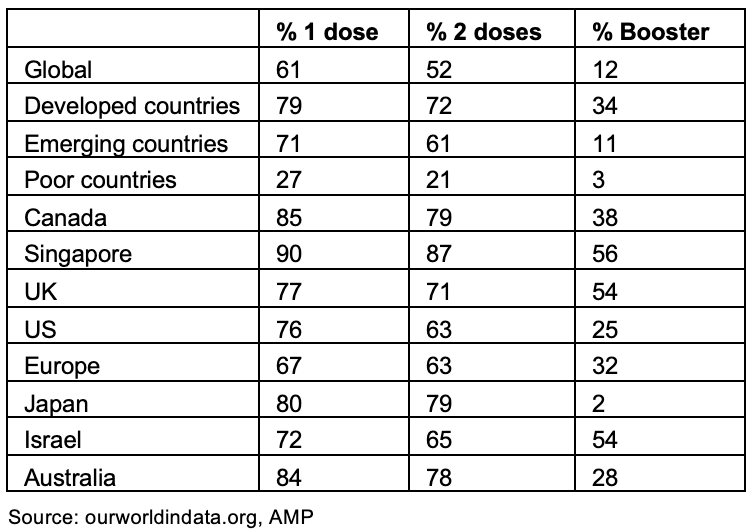

The combination of prior exposure to covid globally and vaccines providing some immunity, new covid treatments and covid morphing lately in a way that is more transmissible but less harmful all provide reason for optimism the pandemic may be heading down a path where the world can live with covid and disruptions caused by it will continue to ease. The main risk remains the possible emergence of more harmful variants – particularly in poorer countries where only 21% are fully vaccinated.

52% of the world’s population is now vaccinated with two doses and only 12% have had a booster.

Percentage of population that’s been vaccinated & had a booster

27% of the Australian population have now had a booster and it's rising rapidly as well as the proportion of the population with one dose with the vaccination of 5-11-year-olds.

Economic activity trackers

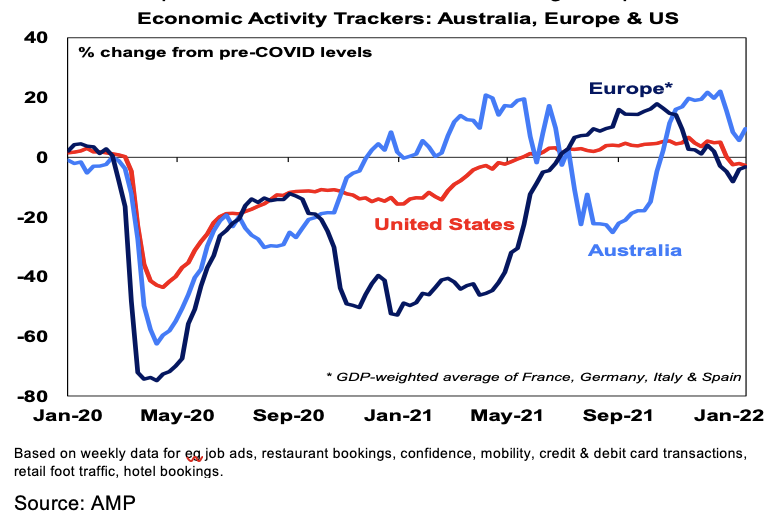

Our Australian Economic Activity Tracker rose slightly over the last week reflecting improvement in mobility, restaurant and hotel bookings, shopper traffic and confidence. This is consistent with the downtrend in new Omicron cases and lessening workplace disruptions. The worst may now be over with further improvement likely. Our US activity tracker fell a bit but our European tracker showed a further slight improvement.

Based on weekly data for eg job ads, restaurant bookings, confidence, mobility, credit & debit card transactions, retail foot traffic, hotel bookings.

Major global economic events and implications

Business conditions PMIs fell in January in the US, Europe, UK, Japan and Australia as Omicron disruptions impacted. With new cases declining in some regions and restrictions being eased the pull back may be short-lived.

Other US data was mostly solid. Consumer confidence fell but by less than expected. Meanwhile, December quarter GDP rose by 6.9% annualised although that was mainly driven by inventories, capital goods orders are continuing to trend up, new home sales and house price gains are strong and jobless claims fell suggesting some lessening in Omicron disruptions.

The fact inventories are starting to rebuild is positive suggests supply bottlenecks may be starting to fade. Of course, they are still very low relative to GDP. Meanwhile annual core private consumption deflator inflation rose further to 4.9%yoy and growth in employment costs accelerated further to 4%yoy.

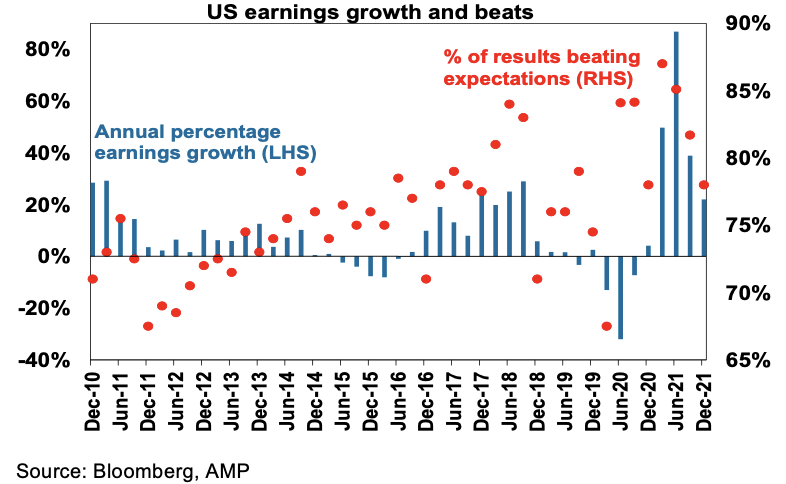

So far, 34% of US S&P 500 companies have reported December quarter earnings with 77% now beating expectations (compared to a norm of 76%) and consensus earnings growth expectations have been revised up to 23%yoy.

The German IFO business climate index saw a surprise rise in January driven by improved expectations.

Australian economic events and implications

In Australia a fall in business confidence in the December NAB survey confirmed the Omicron driven weakness evident in Australia’s PMI. Fortunately, we may have seen the peak in disruption with Omicron with new cases down and Woolworths noting the number of missing warehouse staff has halved. Apart from the stronger than expected CPI inflation for the December quarter, producer price inflation also accelerated in the December quarter to 3.7%yoy.

What to watch over the next week?

Jobs data in the US (Friday) for January is expected to be impacted by Omicron with payrolls up a relatively subdued 200,000 but unemployment remaining very low at 3.9%. In other data, Omicron disruptions are likely to see the January ISM manufacturing conditions index (Tuesday) and the services ISM (Thursday) pull back but job opening data for December (Tuesday) is likely to have remained strong. The flow of December quarter earnings will start to speed up.

Eurozone December quarter GDP (Monday) is expected to show a slowdown in growth to 0.4%qoq from 2.2% in the September quarter as a result of the surge in Delta cases from October. December unemployment (Tuesday) is expected to be unchanged at 7.1% and January inflation (Wednesday) is expected to fall back to 4.4%yoy. The ECB on Thursday is expected to leave rates on hold but continue with a slowing in its overall bond buying program and signal somewhat greater concern about inflation.

By contrast, the continuing surge in inflation is expected to see the Bank of England (Thursday) raise rates to 0.5%.

In Australia, the RBA (Tuesday) is expected to leave rates on hold but following recent stronger than expected jobs and inflation data will likely revise down its unemployment forecasts and revise up its inflation and wages forecasts and as a result, adopt a far more hawkish stance signalling that rate hikes are likely to start earlier than its previous guidance for around 2024. In the meantime, it will announce an end to its bond buying program. This more hawkish message is likely to be elaborated on in a speech by Governor Lowe (Wednesday) and in the RBA’s quarterly Statement on Monetary Policy (Friday). As noted earlier in this report our base case is for the first hike in August of 0.15%, followed by a 0.25% hike in September with the cash rate to end the year at 0.5% but the risk is that rate hikes will start in June with the cash rate ending the year at 0.75%.

On the data front expect a further acceleration in December credit growth (Monday) driven by housing credit, CoreLogic home price data for January to show a 0.9% rise, December retail sales to fall by 3% but leaving December quarter retail volumes up 7.3% and housing finance for December to fall by 1% (all Tuesday) and dwelling approvals to show 1% rise with the trade surplus falling to around $9bn (both Thursday). December quarter earnings results will start to flow but only with a handful of companies reporting including Amcor (Wednesday), Newscorp and REA (Friday). Consensus earnings expectations for this financial year are for a 4% rise with a 3% fall in mining profits but gains elsewhere.

Outlook for investment markets

Global shares are expected to return about 8% this year but we may now be starting to see the long-awaited rotation away from growth and tech-heavy US shares to more cyclical markets. Inflation, the start of Fed rate hikes, the US mid-term elections and China/Russia/Iran tensions are likely to result in a far more volatile ride than 2021, and we are already seeing this. Mid-term election years normally see below-average returns in US shares and since 1950, have seen an average top-to-bottom drawdown of 17%, usually followed by a stronger rebound.

Despite their rough start to the year Australian shares are likely to outperform helped by stronger economic growth than in other developed countries and leverage to the global cyclical recovery.

Still-very-low yields and a capital loss from a rise in yields are likely to again result in negative returns from bonds.

Unlisted commercial property may see some weakness in retail and office returns, but industrial property is likely to be strong. Unlisted infrastructure is expected to see solid returns.

Australian home price gains are likely to slow with prices falling later in the year as poor affordability, rising mortgage rates, higher interest rate serviceability buffers, reduced home buyer incentives and rising listings impact.

Cash and bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.1%.

Although the AUD could fall further in response to coronavirus and Fed tightening, a rising trend is likely over the next 12 months helped by still-strong commodity prices and a decline in the USD, probably taking it to about $US0.80.