6 July 2025

1300 794 893

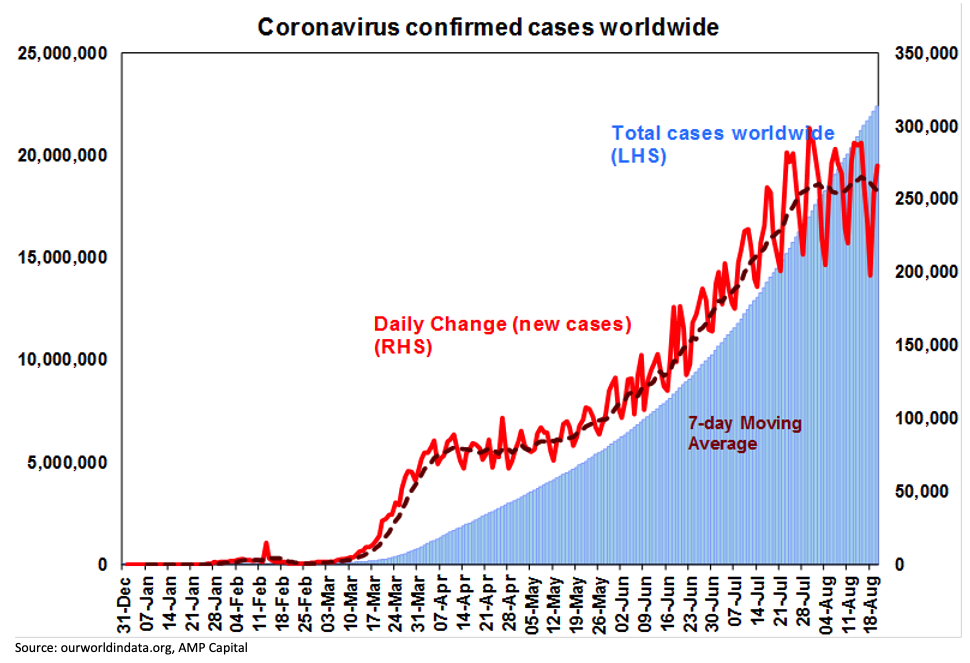

The flat trend in new global coronavirus cases is continuing. Emerging countries are mixed with:

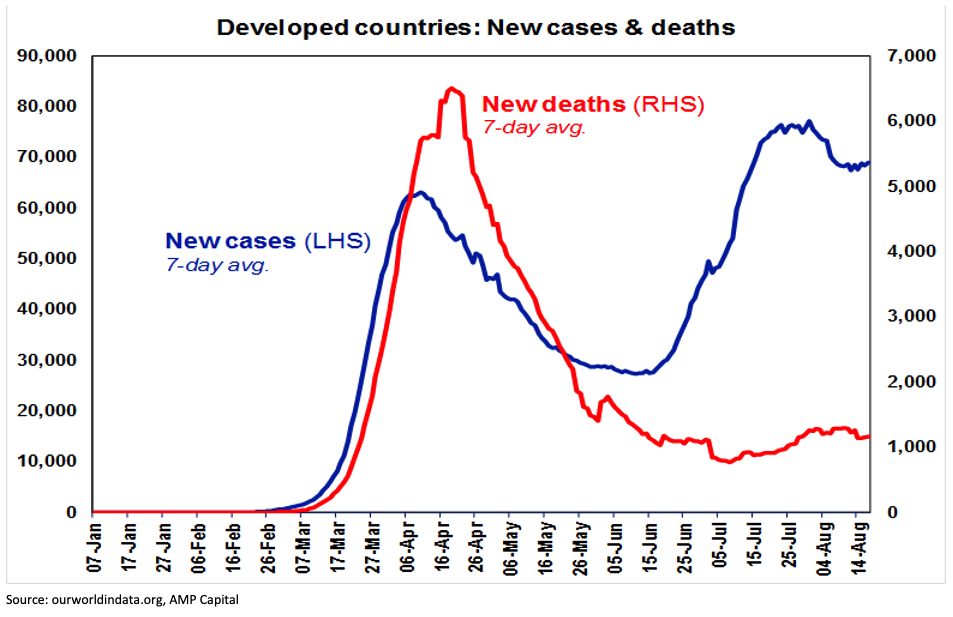

New cases in developed countries remain down from their recent highs with a still falling trend in the US offsetting a rising trend in Europe (led by Spain and France but with Germany and even Italy and the UK on the way up). Japan remains elevated but is now down from its highs, but now South Korea is also rising and New Zealand has seen a spike.

The good news though is that the second-wave of new coronavirus cases in developed countries has continued to be far less deadly than the first wave, with deaths running well below their April high whereas new cases have been well above. This is helping to avoid a return to generalised lockdowns in most countries – in favour of targeted measures.

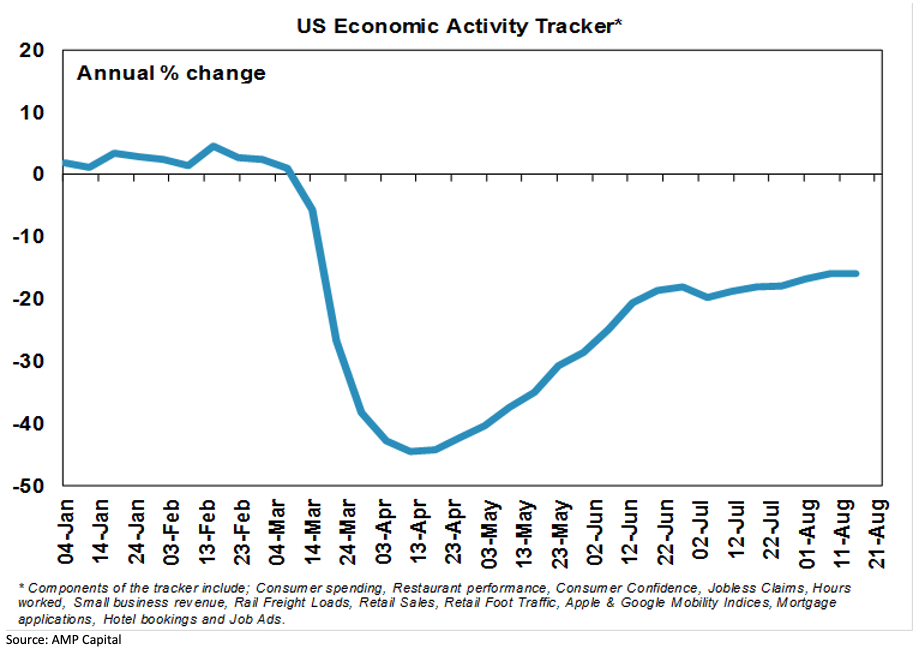

This in turn continues to add to confidence that the economic recovery that has been seen in developed countries since April can continue. With new cases and hospitalisations falling and the fatality rate remaining relatively low without a return to a lockdown averted our US Economic Activity Tracker looks to be resuming its upswing, albeit it was flat over the last week not helped by a fall in job ads.

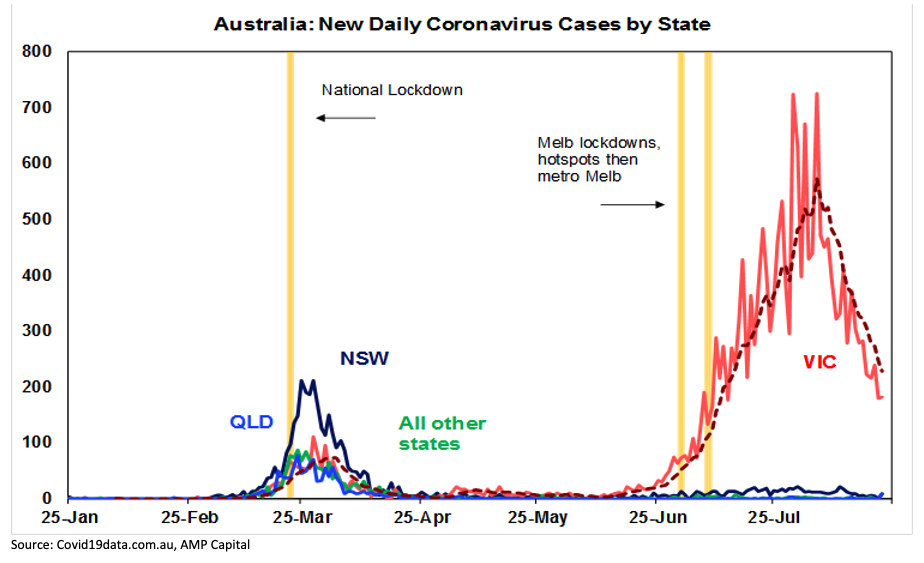

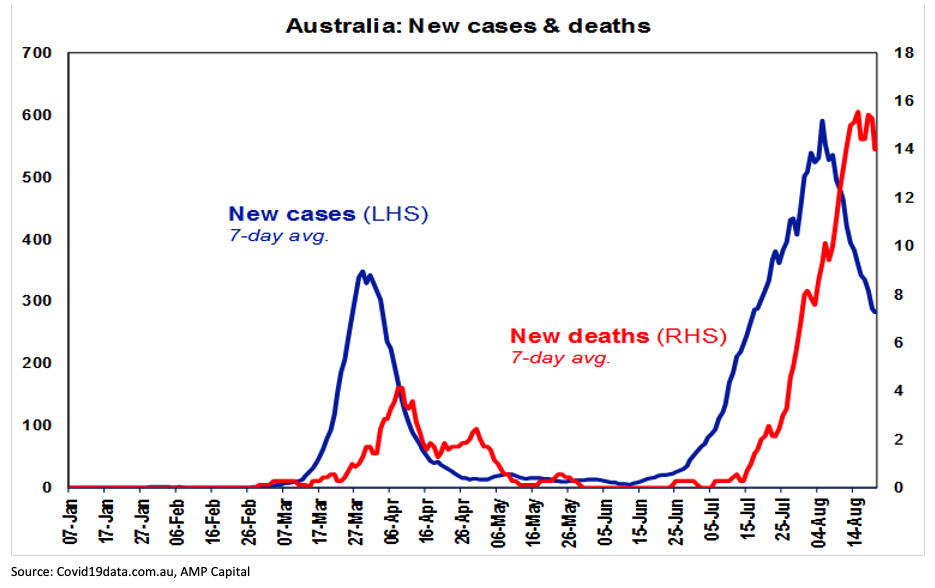

In Australia, we have continued to see better news on coronavirus frontwith new cases in Victoria trending down as the hard lockdown impacts and new cases remaining low in NSW (suggesting that testing, tracking and quarantining programs outside Victoria are working well).

Unfortunately, unlike in many other developed countries the second wave of coronavirus cases has been more deadly in Australia than the first as it took hold in Victorianretirement homes. With new cases now falling though deaths should soon follow thankfully. And Australia’s measured death rate at 1.8% remains low compared to the US at 3.1%, the UK at 12.9%, France at 13.5%, Italy at 13.9% and Sweden at 6.8%.

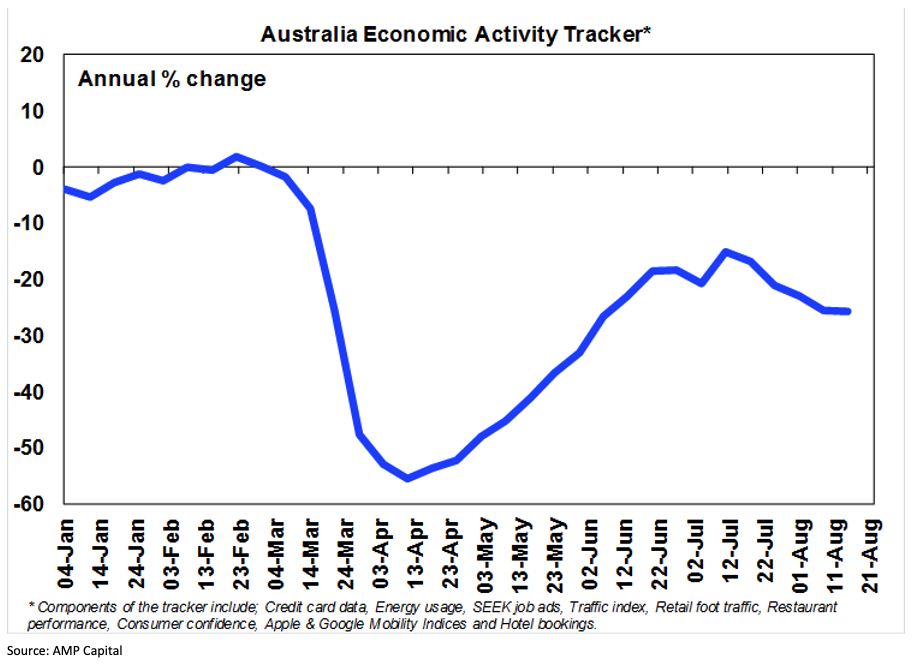

The Victorian lockdown is continuing to weigh on economic activity in Australiawith our Australian Economic Activity Tracker remaining well down from its July high although it was basically flat over the last week helped by a slight rise in consumer confidence and restaurant bookings. If Victoria continues to come under control the economic recovery should resume sometime in the next month.

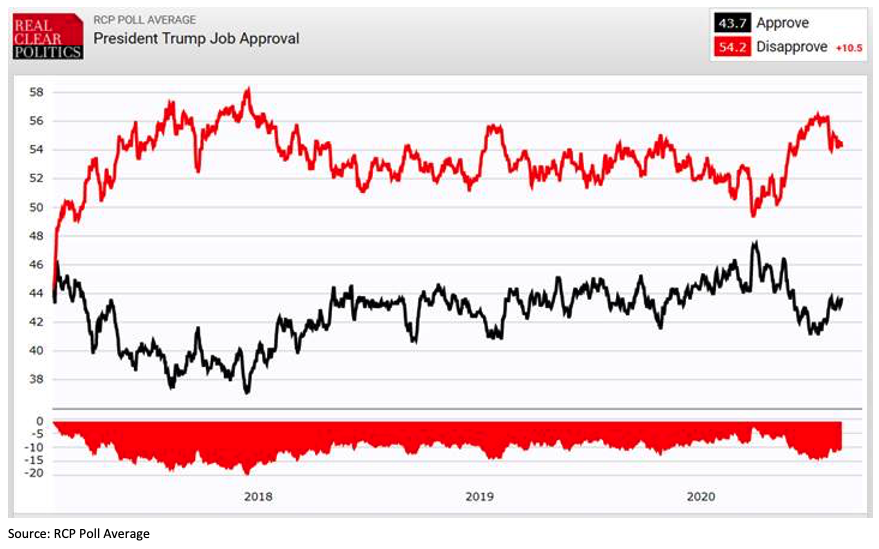

The US election is now hotting up and with new coronavirus cases declining Trump’s approval rating has improved a bit and Biden’s lead in opinion polls has narrowed from around 10 points in late June to around 8 points. With the increasing focus on the election its likely to add to market volatility particularly if Trump’s prospects start deteriorating again - the market often favours the incumbent ahead of the election and prefers his tax policies. But as long as Trump still sees some chance of being returned he is unlikely to ramp up tensions with China to the point of adversely affecting the economic outlook. Election pressures may be getting the US closer to a stimulus deal though with House Speaker Nancy Pelosi indicating that the Democrats might agree to reduce their stimulus proposal in order to reach a deal to help the economy and then revisit it after the election.

For share markets it’s still the same story. The negatives remain the uncertainty around coronavirus, the pausing or reversal of reopening, very high unemployment, the hit to earnings, the US election, US/China tensions and the seasonally weak period of the year for shares that we have now entered. Recent gains in US shares have also come on low breadth suggesting the risk of a correction. But these are arguably more than offset by a long list of positives including continuing good news on coronavirus treatments and vaccines, the second wave in developed countries being less deadly than the first, several countries showing that it is possible to contain the virus, China tracing out a Deep V recovery, the safe haven $US falling which is normally a positive sign, monetary and fiscal policy remaining ultra-easy, low interest rates and bond yields making shares look cheap and there is still a lot of cash on the sidelines. Shares are still vulnerable to further volatility, with coronavirus and US/China tensions being the main risks. But the positives should keep any volatility to being a correction in a still rising trend.

Australian economic events and implications

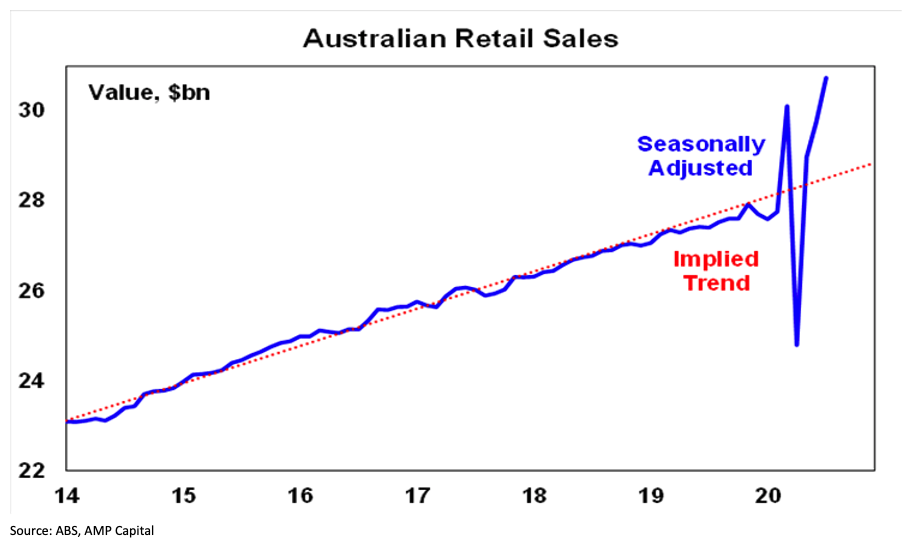

Australian retail sales rose another 3.3% in July led by large increases in household goods - reflecting people being at home, not going away on holidays and so spending on refurbishment - along with a continuing recovery in clothing and café/restaurant sales. Victoria was the only state to see a fall (-2% month-on-month). With retail sales up 12% on a year ago and running well above pre-Covid levels some pullback is to be expected in the months ahead as demand looks to have been pulled forward and as government income support measures are reduced. Melbourne’s stage 4 lockdown will also likely depress August retail sales. However, the continued strength in July does tell us that people are still keen to get out and spend and that there is still some chance of overall positive GDP growth this quarter despite the setback in Victoria.The problems in Victoria saw the CBA’s composite PMI fall back sharply driven by a slump in the services sector with the manufacturing index little changed.

The RBA remains dovish and is not ruling out further easing. With negative rates, monetary financing of the government and foreign exchange intervention basically ruled, further easing is likely to come in the form of a rate cut to 0.1% and more QE

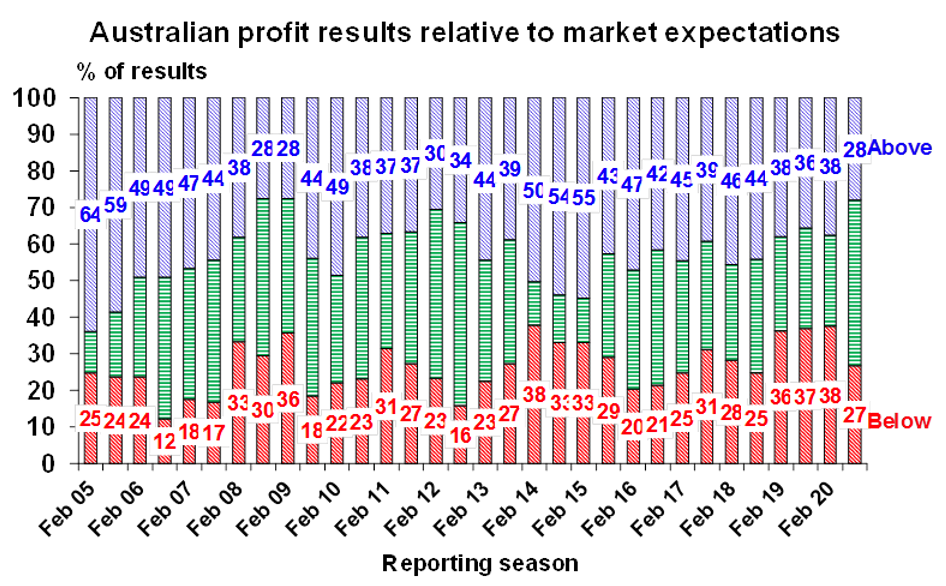

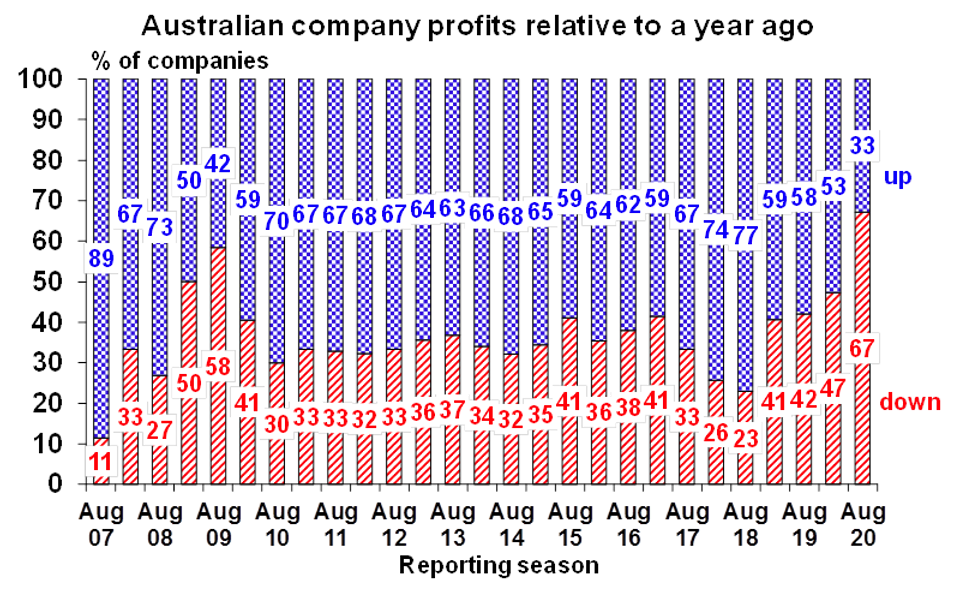

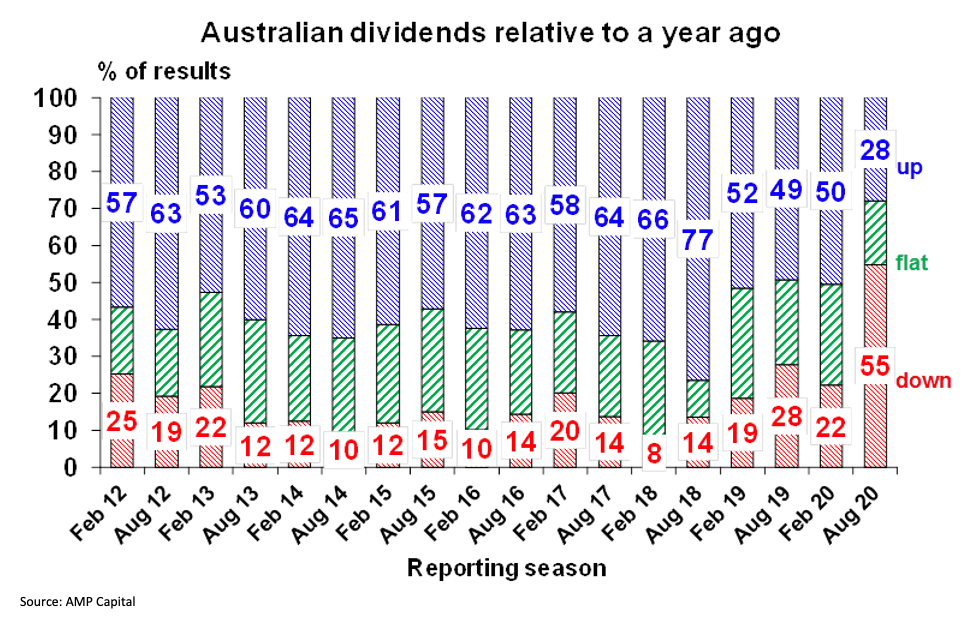

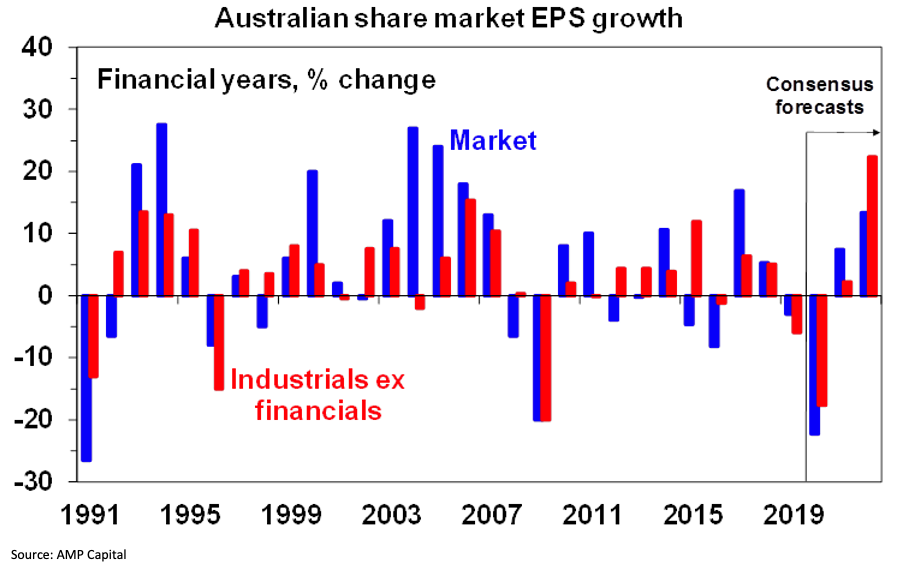

The Australian June half profit reporting season is now 70% complete by companies and 80% complete by market capitalisation. While it’s clear that company earnings and dividends have been hit hard by the coronavirus shock, the hit has not been as bad as feared and most companies appear quite resilient and this in turn has enabled a majority (or 59%) of companies’ share prices to outperform the market on the day they reported and for the market as a whole to rise so far through August. In this sense it’s been similar to the US June quarter earnings reporting season. So far only 28% of results have exceeded expectations compared to a norm of around 44% but at least misses have only been 27% so beats have roughly matched misses. Only 33% of results have seen earnings rise from a year earlier (compared to a norm of 66%) and 55% have cut dividends (compared to a norm of just 16%). So far consensus earnings expectations for 2019-20 have fallen slightly to -22.3% (from -21% three weeks ago) and this will be worse fall in earnings since the early 1990s recession. Financials are being hit the hardest with the consensus expecting a -29% slump in earnings led by insurers and the banks, followed by industrials with a -17.7% fall in earnings and resources with -14.4%.

What to watch over the next week

In Australia, the ABS’s weekly payroll jobs data (Tuesday) will likely have been dragged down by the Victorian lockdown, June quarter construction data (Wednesday) is likely to have fallen 7% with business investment (Thursday) showing a similar fall reflecting theshutdown from late March. Preliminary July goods trade data (Tuesday) is likely to point to a continuing strong trade surplus.

The Australian June half profit reporting season will basically wrap up with 41 major companies reportingincluding Fortescue and Super Retail Group (today), Ansell, Oil Search, Scentre and Stockland (Tuesday), Adelaide Brighton and Worley Parsons (Wednesday), Flight Centre and Nine (Thursday) and Woolworths (Friday).

Outlook for Aussie markets

After a strong rally from March lows shares remain vulnerable to short term setbacks given uncertainties around coronavirus, economic recovery, the US election and US/China tensions. But on a 6 to 12-month view shares are expected to see good total returns helped by a pick-up in economic activity and stimulus.

Unlisted commercial property and infrastructure are ultimately likely to continue benefitting from a resumption of the search for yield but the hit to economic activity and hence rents from the virus will weigh heavily on near term returns.

Australian home prices at present are being protected to some degree by income support measures and bank payment holidays but higher unemployment, a stop to immigration and rent holidays will push prices lower into next year. Home prices are expected to fall by around 10%-15% from their April high. Melbourne is particularly at risk on this front as its Stage 4 lockdown pushes more businesses and households to the brink.

Cash and bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.25%.

Although the $A is vulnerable to bouts of uncertainty about coronavirus, the economic recovery and US/China tensions, a continuing rising trend is likely. Particularly with the US expanding its money supply far more than Australia is via quantitative easing and with China’s earlier recovery supporting demand for Australian raw materials (assuming political tensions between Australia and China are kept to a minimum).