11 July 2025

1300 794 893

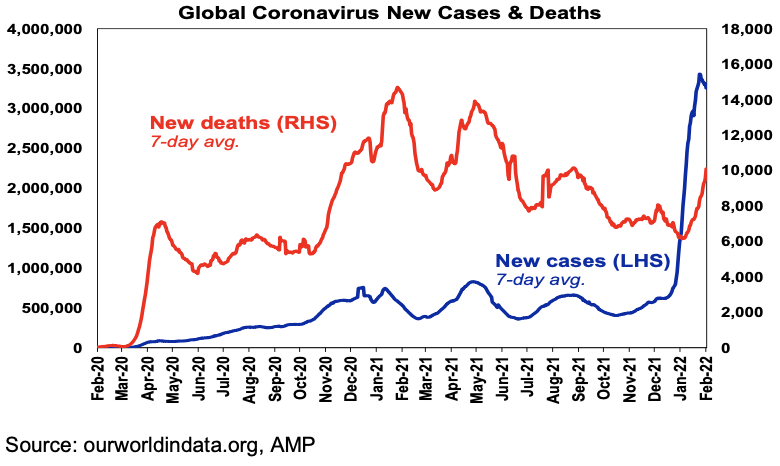

New global covid cases slowed a bit over the last week.

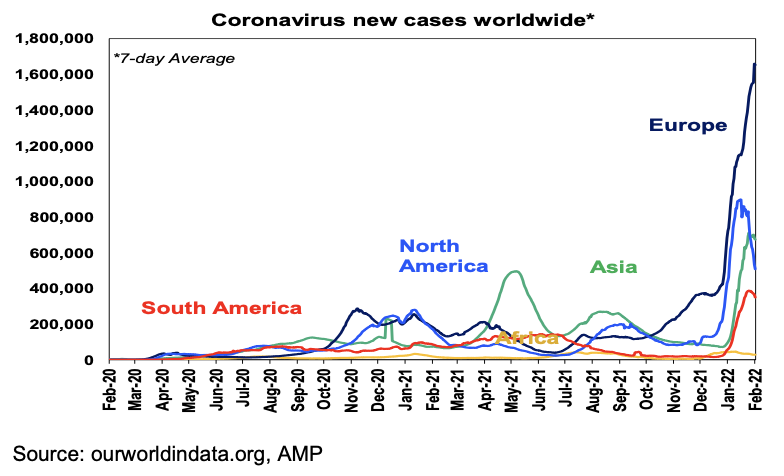

New cases have continued to slow in the US and Canada, but Europe has seen a further rise driven by Germany and a renewed spike in the UK as Omicron sub-variant BA.2 impacts. Several countries in Europe are seeing a declining trend though and this includes France, Italy and Spain and several countries across Europe have been easing restrictions, including Denmark which also looks to have peaked.

A new but less severe Omicron wave on the way?

The bad news is that the rise of Omicron sub-variant BA.2 – which appears to be more transmissible than the original Omicron (BA.1) – could extend the latest global covid wave as it has in several European countries. However, Omicron BA.2 appears to be no more severe than BA.1. In fact, based on Denmark’s experience - which was one of the first countries to be hit by BA.2 - it looks to be much less severe with far more ICU patients at the height of the Omicron BA.1 wave in early January than in the second BA.2 wave (which saw more than double the number of daily cases) in late January.

Taken together with Denmark’s very high vaccination rate – with about 80% of the population double vaccinated and about 60% having had a booster – it has removed all covid restrictions because covid is no longer seen as a “critical threat”. The further evolution of coronavirus in a more transmissible but potentially less harmful direction along with protection from vaccines provides reason for optimism covid is transitioning from being a pandemic to being endemic.

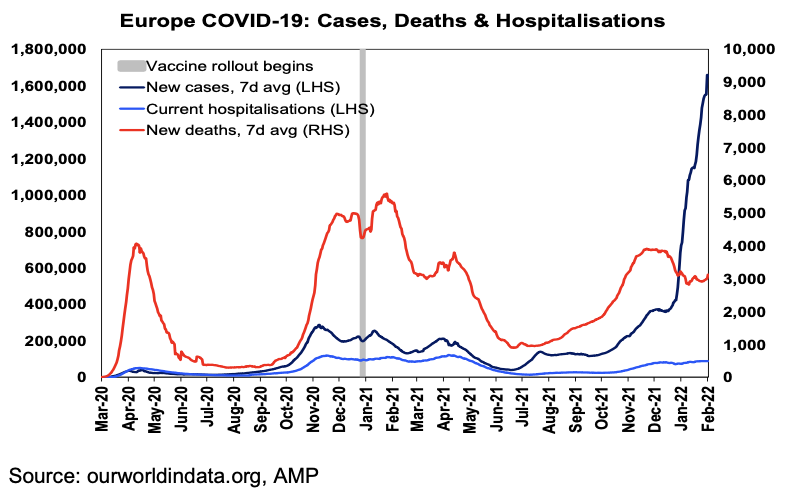

Deaths and hospitalisations remain subdued relative to new cases compared to prior waves. This is evident in the chart for global deaths versus cases above and is evident in most developed countries (including Europe in the next chart) and likely reflects a combination of protection against serious illness provided by prior covid exposure and vaccines, better treatments and Omicron being less harmful. Europe’s experience is particularly noteworthy - so far its spike higher in new cases in the last few weeks which appears to have been largely driven by Omicron BA.2 has not been associated with much of a rise in hospitalisations at all which may be consistent with Omicron BA.2 being less harmful than Omicron BA.1, which was in turn less harmful than Delta.

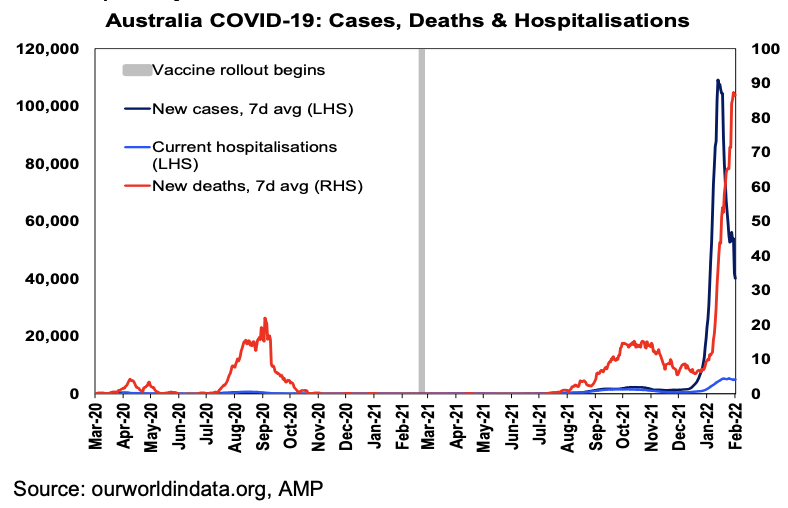

Australia has seen a further decline in new cases. While the level of hospitalisations and deaths increased in the last two months, they remain low relative to new cases compared to earlier waves reflecting the protection provided by vaccines against serious illness and Omicron being less harmful. The decline in new cases points to a further fall in hospitalisations and then deaths as they follow with a lag. The high risk for the next few months is that Omicron sub-variant BA.2 along with the return to school leads to a resurgence in new cases. However, as noted above, Omicron BA.2 may be less harmful than the original Omicron and if it's mainly more children getting covid, a new Omicron wave of cases may not necessarily put significantly more pressure on the hospital system.

Various studies continue to highlight that vaccines are providing significant protection against serious illness including from the Omicron variant(s). For example, during the week ending 8 January, unvaccinated adults were 23 times more likely to be hospitalised in Los Angeles County than vaccinated adults.

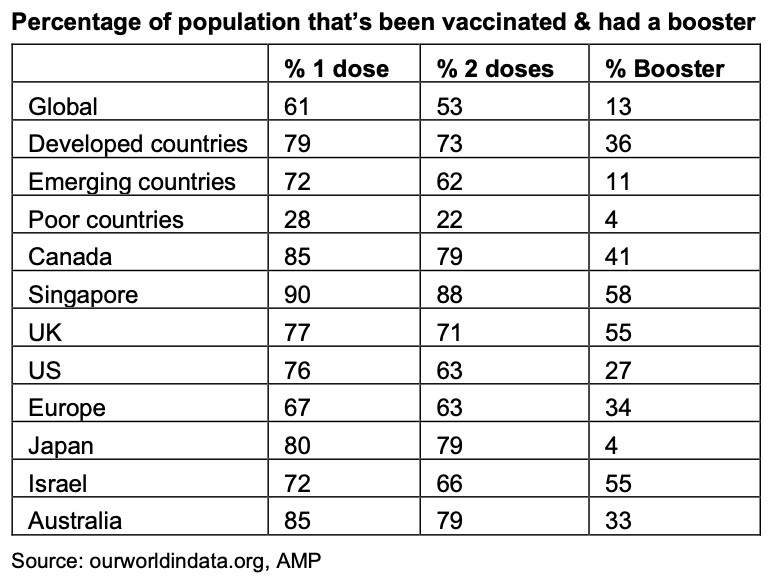

53% of the world’s population is now vaccinated with two doses and 13% have had a booster. The trouble is that it's rising slowly (at about 1% of the world’s population a week) and in poor countries, only 22% have had two doses – which prolongs the risk of new more harmful mutations developing.

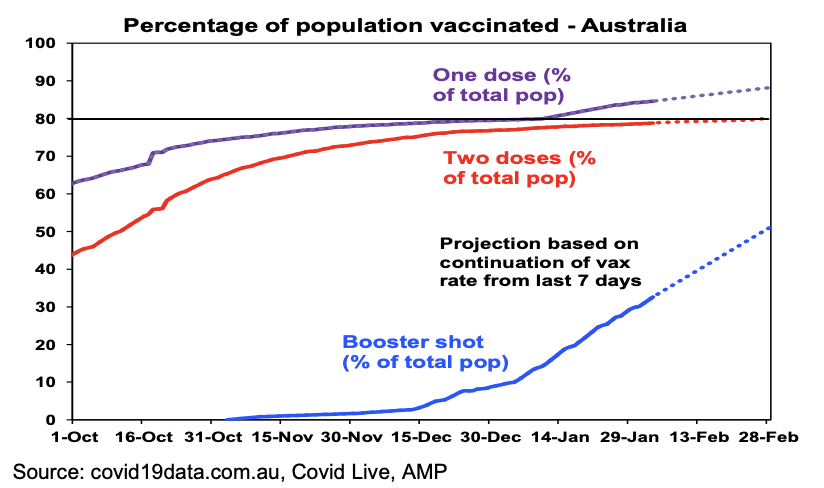

33% of the Australian population have now had a booster and it’s rising rapidly and the proportion of the population with one dose has risen to 85% with the vaccination of 5-11-year-olds.

Economic activity trackers

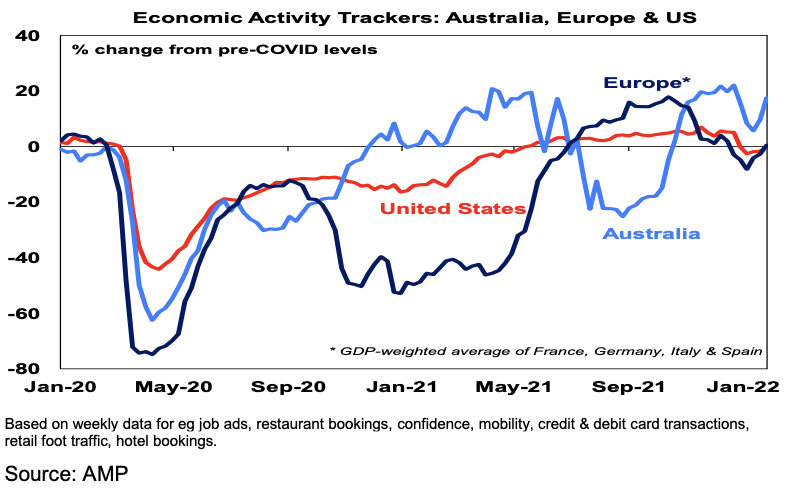

Our Australian Economic Activity Tracker has recovered further reflecting improvement in mobility, restaurant and hotel bookings, shopper traffic and confidence as Omicron cases and workforce disruptions receded. The shallow and brief dip in the Tracker points to far less impact on March quarter GDP than seen with the Delta lockdowns in the September quarter. In fact, we just see a moderation in the rate of GDP growth rather than a contraction. Our US and European Economic Activity trackers also improved.

Major global economic events and implications

US data was mostly strong. Payroll employment growth at 467,000 in January was far stronger than expected with prior months revised up by 709,000, unemployment rose but only to 4% with underemployment falling again and wages growth accelerated to 5.7%yoy. This was despite the Omicron disruption. While participation rose, it's still well below pre-pandemic levels. Meanwhile, job openings and quits data also point to a continuing very tight labour market and jobless claims have been falling since mid-January suggesting a fall in unemployment in February. The strong January jobs report keeps the Fed on track for a March rate hike which could yet turn out to be 0.5%, four or five rate hikes this year and the start of quantitative tightening. The ISM business conditions indexes fell back in January with Omicron impacting but by less than expected and remain strong.

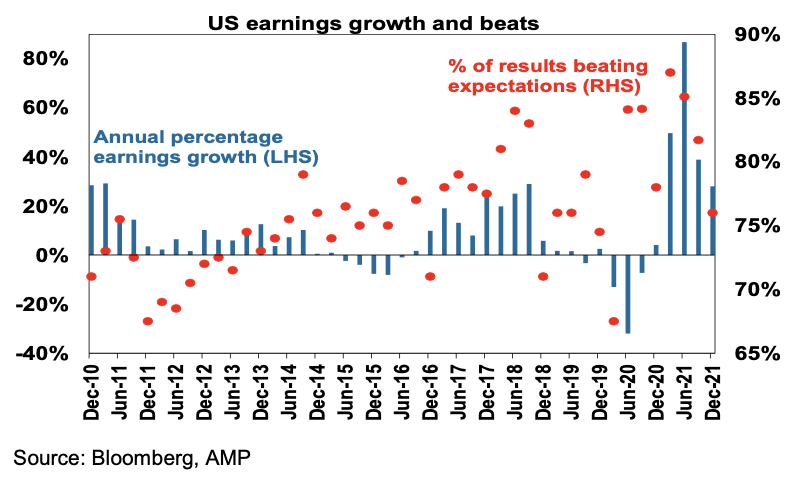

56% of US S&P 500 companies have reported December quarter earnings with 76% beating expectations which is about average and consensus earnings growth expectations have jumped to about 28%yoy and are now likely to end up at about 30%yoy.

Eurozone December quarter GDP growth slowed to just 0.3%qoq as coronavirus outbreaks impacted with Germany down but France, Italy and Spain up. Eurozone unemployment fell to 7% in December, but inflation surprisingly rose further in January to 5.1%yoy.

China’s business conditions PMIs for January moderated pointing to further policy stimulus measures.

A fall in NZ unemployment to just 3.2% in the December quarter and a rising trend in several wage growth measures following the surge in inflation to 5.9%yoy is adding to expectations that the RBNZ will raise rates by 0.5% this month.

Australian economic events and implications

While Australian retail sales fell in December it looks like payback after two very strong months as Black Friday sales brought spending forward, but in any case, December quarter retail sales look like were up 7.5% or so in real terms and they remain well above their pre-pandemic trend. Omicron is also likely to have impacted late in the month and this will likely also depress January retail sales ahead of a rebound this month.

The trade surplus fell again in December, but this was because of strong imports, rather than weak exports, which is consistent with rising demand in the economy.

Housing data was all strong: total credit growth rose to its fastest since 2008 and housing credit growth remained solid in December with investor lending growth continuing to accelerate; housing finance rose to a new record high pointing to a further acceleration in housing credit; building approvals unexpectedly rose in December and look to be settling at a pretty high level; and CoreLogic data showed another 1.1% gain in national home prices in January, led by very strong gains in Brisbane and Adelaide.

We remain of the view that home prices will peak later this year as poor affordability and rising rates impact, but in the meantime, the continuing surge in investor lending keeps alive prospects for further APRA macro-prudential tightening.

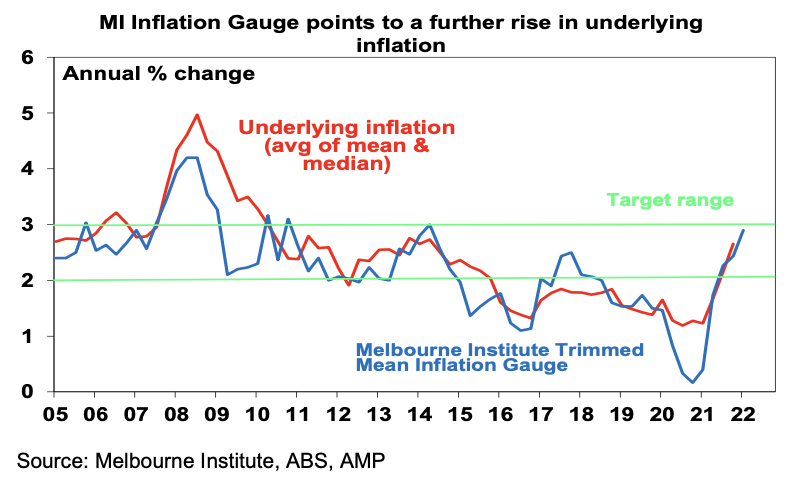

Meanwhile, the Melbourne Institute’s Inflation Gauge saw another acceleration in January pointing to a further acceleration in underlying inflation this quarter.