6 July 2025

1300 794 893

September quarter CPI inflation was in line with market expectations for a 0.8% QoQ/3% YoY rise on the back of high petrol prices, but the surprise was that the underlying measures rose more than expected and are now back in the target range for the first time since 2015. While it’s pretty benign compared to the US, UK, NZ and Canada it shows that supply constraints and other pandemic distortions are also impacting Australia. Producer price inflation and import price inflation also accelerated in the September quarter as global supply constraints impacted.

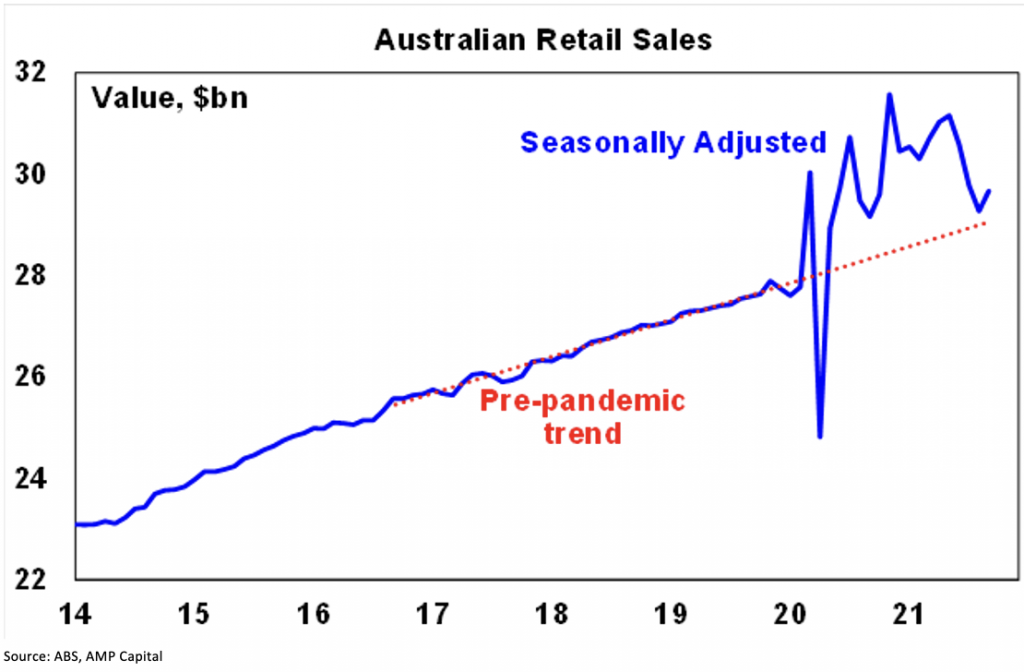

Retail sales bounced in September. Further recovery is likely this quarter as a result of reopening. For the September quarter though, real retail sales likely fell about 5% implying a big hit to consumer spending from the lockdowns.

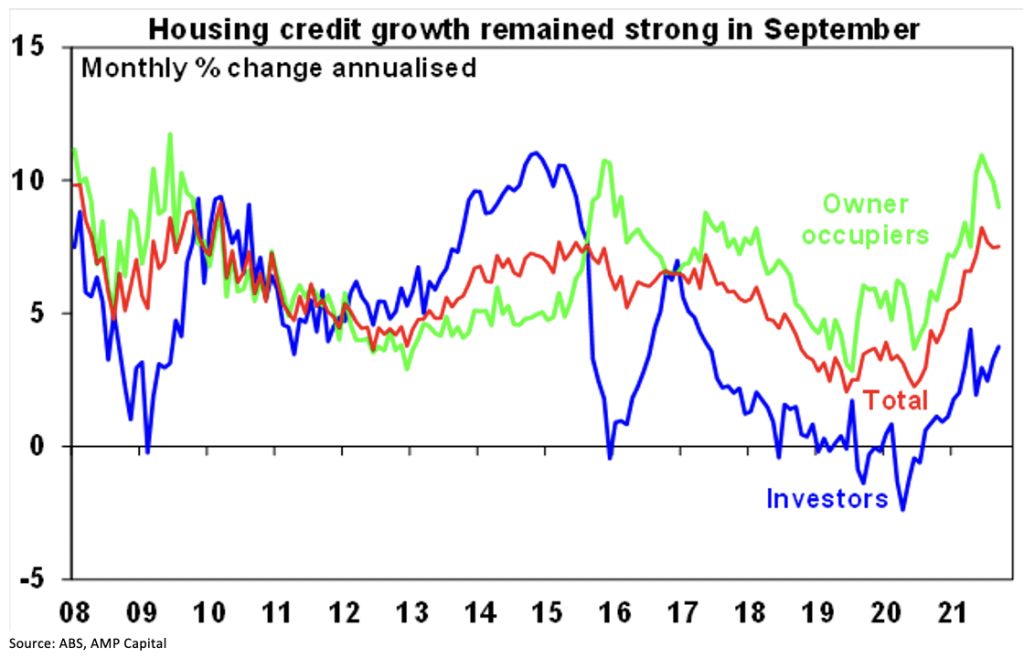

Housing credit growth remained solid in September at 0.6%, rising to 6.5%yoy.

Owner occupiers continue to drive the strength albeit it has slowed a bit and investor credit growth has picked up.

What to watch over the next week

In the US, the Fed is expected to announce that its long-flagged taper to its bond buying program will commence. The is expected to entail a reduction in asset purchases of $15bn a month ($10bn for Treasuries and $5bn in mortgage-backed securities) such that by mid next year the $120bn a month bond buying program will have come to an end. This is widely expected so should not have much impact on markets. The Fed is likely to signal more concern about inflation but indicates that it still sees it as transitory and the conditions for a rate hike are still not met. We expect the first rate hike to come in the second half of 2022.

Expect a strong US payrolls report. On the data front in the US, jobs data for October (Friday) is expected to show a 400,000 gain in payrolls and unemployment falling to 4.7% and the manufacturing and services ISMs for October (also due Wednesday) are expected to remain strong at about 60 with remaining high price indicators. Earnings reports will continue.

Eurozone unemployment (Wednesday) is likely to fall to 7.4%.

China’s Caixin business conditions PMIs for September will be released on Monday and Wednesday.

In Australia, the RBA today is expected to weaken its dovishness in response to the faster than expected reopening of the economy and the greater than expected rise seen in underlying inflation. This is likely to see it bring forward its guidance for the first cash rate hike to 2023 and it may ditch or soften its 0.1% yield target.

On the one hand, it is likely to point out that the rise in the trimmed mean inflation rate was narrowly based and impacted by various pandemic related distortions and that uncertainties remain about the pandemic, but on the other hand, it's likely to be more upbeat on the growth outlook following reopening and is likely to revise up its inflation forecasts slightly in its quarterly Statement on Monetary Policy on Friday. This should be consistent with further tapering in February next year and a weakening or end to the 0.1% yield target for the April 2024 bond sometime in the months ahead.

Given its failure to defend the yield target in the last week it may announce its abandonment on Tuesday. But it’s hard to see the RBA reducing its dovishness on rates too much just yet, preferring to wait and see how the recovery unfolds and whether the bounce in underlying inflation is sustained.

Outlook for investment markets

Shares remain vulnerable to short-term volatility with possible triggers being coronavirus, global supply constraints & the inflation scare, less dovish central banks, the US debt ceiling and fiscal plans and the slowing Chinese economy. But we are now coming into a stronger period seasonally for shares and the combination of improving global growth and earnings, vaccines allowing a more sustained reopening and still-low interest rates augur well for shares over the next 12 months.

Expect the rising trend in bond yields to continue as it becomes clear the global recovery is continuing resulting in capital losses and poor returns from bonds over the next 12 months.

Unlisted commercial property may still see some weakness in retail and office returns but industrial is likely to be strong. Unlisted infrastructure is expected to see solid returns.

Australian home prices look likely to rise by about 21% this year before slowing to about 7% next year, being boosted by ultra-low mortgage rates, economic recovery and FOMO, but expect a further slowing in the pace of gains as poor affordability impacts, home buyer incentives are cut back, listings return to more normal levels, fixed mortgage rates rise further, and macro prudential tightening slows lending.

Cash and bank deposits are likely to provide poor returns, given the ultra-low cash rate of 0.1%.

Although the AUD could pull back further in response to the latest threats to the outlook and weak iron ore prices, a rising trend is likely over the next 12 months helped by strong commodity prices and a cyclical decline in the US dollar, potentially taking the AUD up to about $US0.80.