11 July 2025

1300 794 893

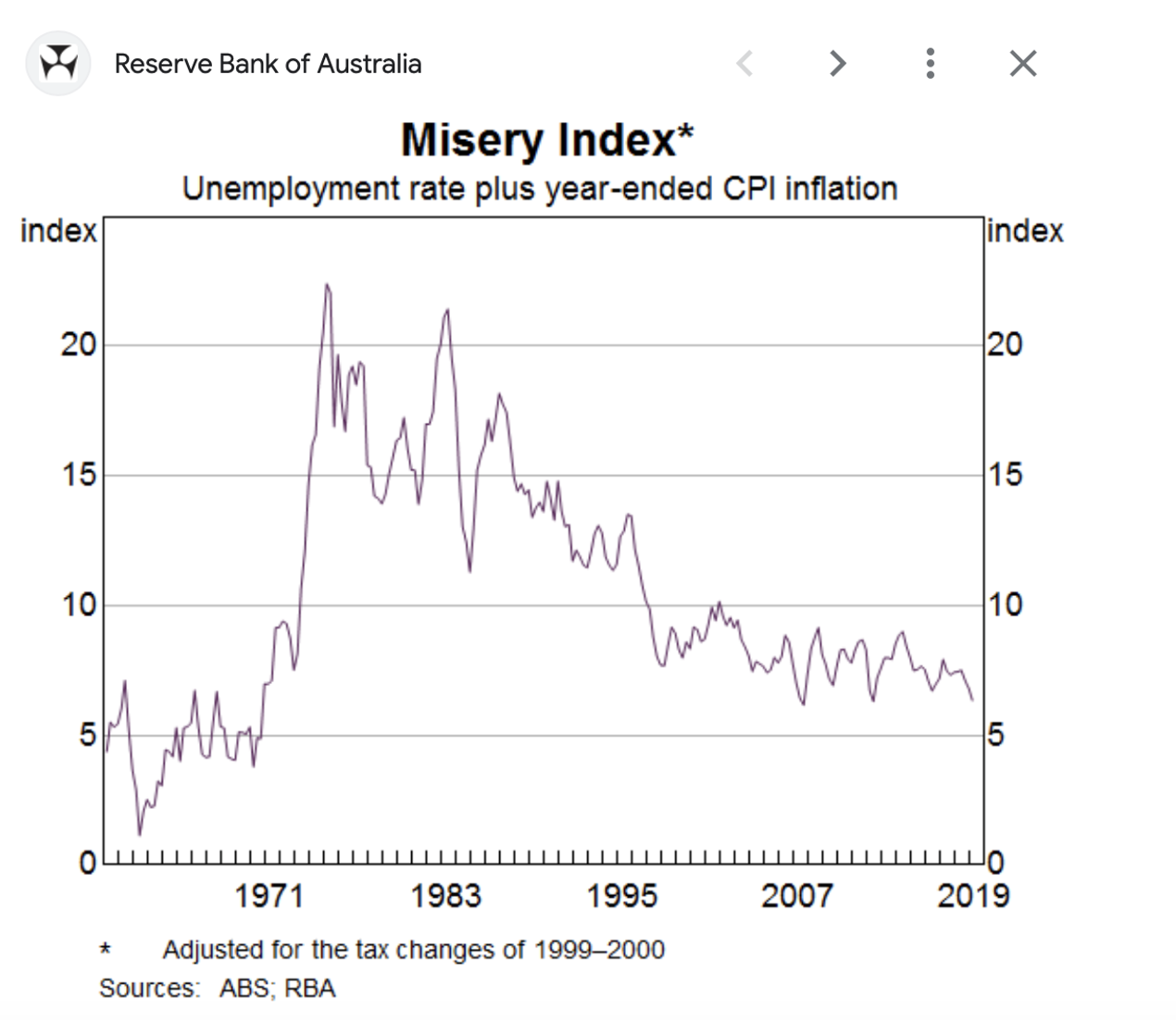

A story today on the Misery Index (MI) took me back to the 1980s when constant rate rises and high inflation saw the MI readings top over 20 on two occasions. It’s now under 10. On that basis, the 1980s was more miserable, but you can’t always trust statistics and I do worry about rattled Aussies fearing another interest rate rise this week.

One important observation about economics and measurements such as the Misery Index, which the SMH’s Shane Wright has reminded us about, is that economic misery and happiness isn’t spread around equally. This unequal metering out of good and bad economic developments or policies will be seen at its worst for some Aussies if the Reserve Bank makes a mistake and raises the cash rate of interest tomorrow.

Before explaining what the Misery Index is, let me quickly point out that Wright informs us that surveys of economists show only one in three think Dr Phil Lowe will raise tomorrow, opting to watch more economic data before he raises again in July or August.

Those worrying about more rate rises are in the hands of the flow of economic data in coming weeks and more miserable economic readings, apart from falling inflation, is going to be the best news for those overborrowed. Underlining the dismal nature of economics, if unemployment rises, demand from business and consumers weakens, both business and consumer confidence plummets and house prices start to fall again. Then the RBA will assume inflation is set to keep dropping.

All that bad news will be good news for inflation and anyone praying for no more rate rises.

The Misery Index simply has been the unemployment rate added to the inflation rate, but University of Melbourne economists Guay Lim and Sam Tsiaplias have incorporated the interest rate effect as well to say that the average citizen is in a GFC-like situation.

But this is the problem with the Misery Index, because it can be driven by different bad things.

“During the September quarter of 2008, the RBA had official interest rates at 7.25 per cent, unemployment was 4.2 per cent and inflation reached 4.8 per cent,” Wright recalls. However, after that, rates were cut and

unemployment rose to 6% but inflation was lower. Collectively, the number for the index was similar.

This demonstrates that as some have misery in our economy, others can be paying $10,000 to fly business class to Europe, buy new cars or a house with their good fortune and spending, adding to inflation and possibly future rate rises!

Like yours truly, AMP’s chief economist Shane Oliver is worried about any future rate rises escalating the chances that we’ll end up in recession. “The risk is steadily rising that the RBA will hike rates too far and knock the economy off the narrow path into recession,” he told the SMH.

And Oliver isn’t alone in warning the RBA to be careful about more rate rises. “The case for the RBA to pause in the June meeting is strong, as the RBA may want to have time to receive additional data flows, especially when the monthly inflation data is volatile, and April’s inflation figures do not capture the full extent of services inflation,” explained KPMG chief economist, Brendan Rynne.

Last week’s jump in annual inflation from 6% to 6.8% was based on some questionable statistical numbers. I looked at the 0.3% rise in prices in April and if that was annualised by multiplying it by 12 for the twelve months of the year, the inflation rate would be 3.6%.

I think that’s a good reason for the RBA boss not to add more misery to home loan repayment sufferers, who must be hating the first Tuesday of the month.