1 July 2025

1300 794 893

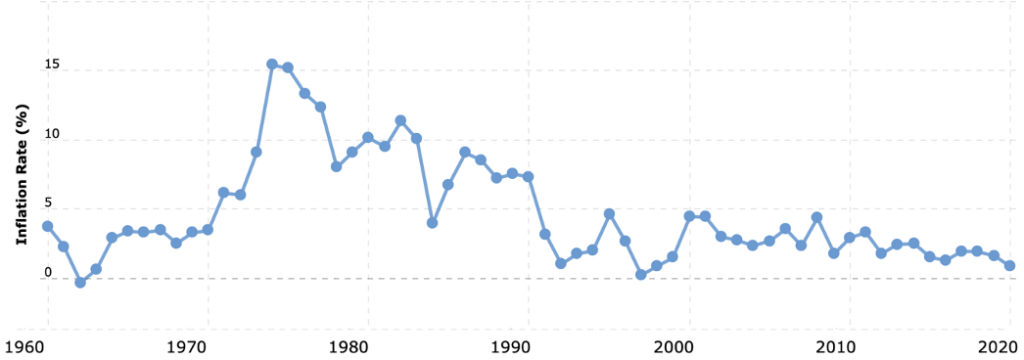

One of the scariest economic periods of my life as a human being (not as an economist) was the late 1980s when my home loan interest rate went to 17%! During those days, in practice, the Treasurer (who was Paul Keating at the time) ran the Reserve Bank. Showing how forgiving we Aussies can be, we voted in him into the Prime Minister’s job in 1993!

That said, you should recall that his rival, Dr John Hewson, was trying to win an election with a new tax called a GST, which was to kick off at 15%!

But back to those record-high home loan rates and the cause was persistently high inflation starting in the 1970s. By the way, I started that loan I mentioned above at 13% and term deposit rates were as high as 10%. The reason was that inflation had been around and high for a long time.

Inflation 1960-2020

And it’s a little worrying when The Australian’s David Rogers writes: “Markets had their first taste of what to expect as inflation started to take hold across the global economy…”.

Interestingly, our market didn’t overreact with the All Ords only down 36 points (or 0.47%), which is not a big sell off. Interestingly also, the Yanks have kept any panic under control overnight, with the Dow only down marginally.

So why the jitters yesterday about inflation and a muted response today?

Rogers gave a part-explanation in telling us why our market did not go too negative when the likes of The Wall Street Journal hit the headlines with: “U.S. inflation hit a three-decade high in October, delivering widespread and sizable price increases to households for everything from groceries to cars due to persistent supply shortages and strong consumer demand”.

The Consumer Price Index (CPI), which is a basket of products ranging from petrol and health care to groceries and rents, rose 6.2% from a year ago, the most since December 1990. And this led to the bond market, which tries to guess how the economy is growing and what will happen to interest rates, pushed up its view on how high rates will rise and when they’ll rise.

And this spooked the stock market, but so far it’s not a big scare.

Why? Well, for starters, economists expected the October number to come in at 5.9% and it was 6.2%, so a big jump in prices was expected.

When interest rates rise, stocks fall in the short term and that’s why the big, bad inflation number hit stocks yesterday. But there’s more to the story.

Aside from a surprise jump in unemployment locally, which went from 4.6% to a 6-month high of 5.2% that also hurt stocks, there’s a big question that when answered could be good or bad for stocks long term.

What we have here is a data-credibility problem. First, as Rogers points out: “economists said a 46,300 fall in employment in Australia and a 5.2 per cent unemployment rate for October were exaggerated by the fact that the employment survey was conducted earlier than usual, in late September and early October, when NSW and Victoria would still be caught up in lockdowns”.

Stocks actually rose on the bad news jobs data! But what about the inflation number? Why isn’t it scaring the pants off the stock market?

Firstly, interest rates in the real world of the consumer and business haven’t changed and the economic growth rates ahead look so good that this positive news will offset the bad news of an eventual interest rate rise, that could come sooner than what’s currently expected.

And secondly and importantly, lots of economists, bankers and stock market influencers think the inflation is temporary. Why? Well, a lot of the inflation is driven by supply problems because of the Coronavirus and as we get vaccinated and economies reopen, it’s thought these supply/cost problems for inflation will disappear.

That’s why stock markets aren’t really having hissy fits. But if the consensus changes that inflation is going to be big and persistent for a long time, stocks will dive.

Over the coming months, the trend for inflation, costs out of the manufacturing sector and economic growth will be watched carefully. If growth is strong and inflation falls, stocks will boom. But if inflation shocks trend on the high side, share prices will give into gravity.

On the growth front, the news is good, with UBS tipping global economic growth booming 7% by year-end, before slowing to a still strong 4.7% in 2022 and 3.6% in 2023. On global inflation, UBS says it drops to 3.9% next year and 2.7% in 2023.

For the US inflation reading, which now is 6.2%, UBS has 2022 at 4.2% and 1.4% for 2023, which means these guys think this high inflation is temporary. I think UBS is on the money. Right now, the stock market agrees. So let’s hope they have a reliable economic crystal ball.