11 July 2025

1300 794 893

It’s been a question financial planners and others in the money game have debated since the arrival of compulsory super for all employees in 1992, which made it more difficult for those people who had too much income or too many assets to get a government pension. It’s the same question that our financial planning clients ask us, even if they’re in their late 40s or early 50s:

How much do I need to retire comfortably?

Most experts say the answer is $1 million. (I can’t help thinking of Austin Powers and Dr Evil whenever I say “One million dollars.” But I digress.)

Lucy Dean in the AFR has looked at the possible ‘evil’ misleading of potential retirees by the finance industry in making everyone think you really do need a million dollars to retire. Dean brings in new analysis that questions how much you need for a comfortable retirement.

The findings come from a group that came out of Choice (the consumer watchdog mob) which has the name Super Consumers Australia.

In the first paragraph of her article, anyone reading this story has to pick up on the line that says “retirees with low-spending patterns can potentially bow out of the workforce with $88,000 in super, without their living conditions deteriorating”.

What? A super balance of one million versus $88,000? This is a must-read yarn! From the outset, you have to know that this will give you a very different retirement than someone who does have $1 million in super when they stop work.

Super Consumers Australia has put the story into three buckets for a pre-retiree aged 55-59 years.

First is the high-spender’s bucket, where a single person who wants to retire and spend $55,000 a year needs $745,000 in super by age 65. A couple wanting to spend $88,000 a year will need $1,003,000 in super by age 65.

Second is the medium spender’s bucket, where you live on $44,000 a year. Then you’ll need $301,000. A couple wanting to spend $64,000 a year will need $402,000 in super on retirement.

And third is the low spender’s bucket. If you can get by on $34,000 a year, you only need $88,000. A couple needing $48,000 will have to have $111,000 in super.

If you’re wondering how all this works, well, you might not know that with a certain amount of money in super you can get a full pension. And retirees have other help from the Government that raises the disposable income of retirees who don’t have big super balances.

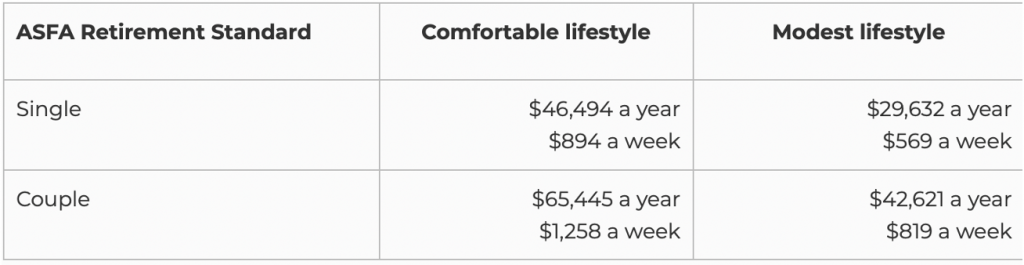

These numbers are way below what the Association of Superannuation Funds of Australia (ASFA) has told us is needed for a good retirement.

ASFA estimates that the lump sum needed at retirement to support a comfortable lifestyle is $640,000 for a couple and $545,000 for a single person. With these amounts, the retirees get a partial Age Pension. The amount these retirees will get will be a reasonable sum as the pension cuts out at $915,500.

In simple terms, if a couple who owns their own home has $405,000 in super and other assets at the point of retirement, they will qualify for the full pension of $38,709. If they earn 5% a year from their super they will get that tax-free. This means they’ll have about $58,000 a year to live on.

This will make them comfortable but they won’t be living the life of Reilly.

I know the good people of Super Consumers Australia want to dispel the $1 million myth about super, but a million dollars provides comfort. It means they don’t need to take big investing risks to live on $70,000 a year. This kind of tax-free annual income coming from super means they can easily go to restaurants, travel, drive a good car, pay for life-happy services and even help their kids and grandchildren.

People with lower balances can do a lot of this by being wise spenders, belonging to clubs and being really organised, but they will feel the pinch at times and might not be able to help others they care about at certain times.

After talking to many retirees in my financial planning business, the bigger you can build your super, the greater your peace of mind in retirement. Fortunately, most young people will retire with big super balances after being slugged with a 10.5% or higher compulsory super charge for most of their working life. Though many young people may not own their home because of the super slug.

Note: For this analysis, it’s important to remember that super isn’t the only asset in the asset test for getting the full pension. The assets include:

The test also considers assets that mightn’t seem obvious. These include:

If you want to build your super or investment portfolio watch our latest episode of Switzer Investing