15 July 2025

1300 794 893

Last week, stocks fell on a worse-than-expected US inflation number. This week they could stop falling or even drop further, depending on what happens in the States on Wednesday. That means our market will either have an OK day Thursday or head even lower!

So what’s the big event on Wednesday?

It’s the interest rate meeting for the Federal Reserve. While it’s expected there’ll be another 0.75% hike in official interest rates, there are two other big stories linked to this central bank get-together.

The first is this: could the rise end up being 1%, which a minority of experts are tipping? I’d say if the Fed tried this, stocks would slump BIG time. We wouldn’t be spared here, so our market would dive as well. Personally, I’m betting this won’t happen. It shouldn’t and I’ll explain why in a minute.

The second decision that could help or hurt stocks is really a collective decision made by the voting members of the central bank on what they think will happen to interest rates. When the mob (called the Federal Open Market Committee, or FOMC) make the decision on the size of an interest rate change, they also reveal what they think interest rates should do going forward. It’s called the dot plot because the dot indicates where the individual voting members of the FOMC think interest rates will stop.

If they raise their overall guesses, which could prove wrong over time, it will spook the stock market.

It makes total sense too because if the Fed raises rates too high, then the US could fall into a recession, which is why stocks are falling at the moment. In fact, there are two reasons, which could prove to be only short-term reasons for the sell-off but they’re understandable.

The first reason is rising interest rates make stocks less attractive. It reduces sales to consumers and business customers, which hits company revenue and profit, which isn’t good news for share prices.

Second, higher interest rates make alternatives to stocks more attractive. As interest rates rise and safe investments, such as government bonds and term deposits head towards 4%, many stock market players could easily dump risky shares for riskless income.

The really big worry for me is the potential of central banks to create a recession by mishandling these rate rises.

This really important fact from our own Reserve Bank shows how risky too many rate rises in a short timeframe might be.

In the egghead world of economics, we economists talk about the importance of the transmission mechanism. I learnt about this many decades ago from my old UNSW colleague, Dr John Hewson (the ex-Coalition leader).

As the RBA’s Tim Atkin and Gianni La Cava explain: “The transmission of monetary policy refers to how changes to the cash rate affect economic activity and inflation.”

But here’s something Tim and Gianni explain that shocks a lot of normal people about how interest rates work. “There is a lag between changes to monetary policy and its effect on economic activity and inflation because households and businesses take time to adjust their behaviour. Some estimates suggest that it takes between one and two years for monetary policy to have its maximum effect.”

That means to expect to see much of a reaction early seems ridiculous, so Dr Phil Lowe (locally) and Jerome Powell (at the US Fed) really are flying blind. Sure, they’d be looking at ‘good’ early predictors of what might happen to inflation but these can be really dodgy at times or be less negative — so they can be unreliable.

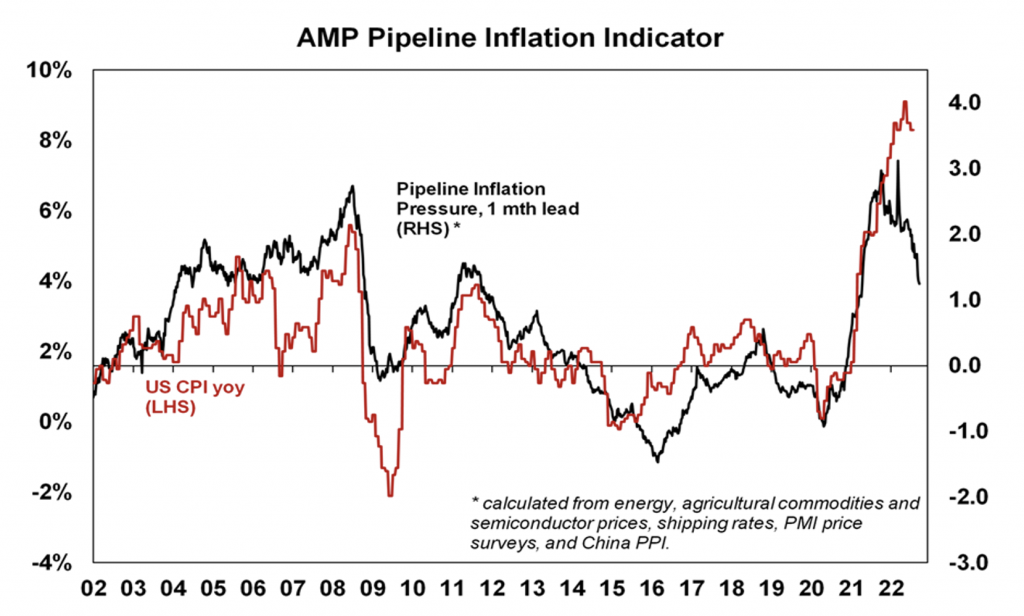

So we better hope Dr Phil and Jerome’s teams are good at guessing the effects of past rate rises. I hope they’re looking at work done by people like Dr Shane Oliver at AMP, whose Pipeline Indicator shows inflation is falling faster than what the US official numbers are showing.

In this chart below, the official inflation number (shown in red) is just starting to fall but the Pipeline Indicator (in black) has fallen a lot harder, which is a good sign that rate rises are working.

Shane makes three points about what he’s seeing with inflation:

1. Producer price inflation is slowing and looks to have peaked in the US, UK, China and Japan.

2. This is consistent with our Pipeline Inflation Indicator, which is continuing to trend down, given falling price and cost components in business surveys, falling freight rates and lower commodity prices (outside of gas and coal).

3. Market-reported rents, as measured by Zillow in the US, point to a slowing in US “shelter” inflation ahead. As this reflects new leases, it impacts with a lag. This is significant because the shelter component is 33% of the US CPI and is dominated by rent and owners’ equivalent rent.

If Jerome and his voting members are seeing this, they should be thinking that rate rises should be getting less frequent and lower in the not-too-distant future.

We have to hope that US economic indicators, other than inflation that’s out on October 13, will be telling the Fed that rate rises are working.

This week, the Yanks get housing, manufacturing and services sector data, as well as the leading index for the economy. These data reads along with the Fed meeting takeaways will be really important for Wall Street and our stock market.