4 July 2025

1300 794 893

New governor of the Reserve Bank Michelle Bullock might have been given a timely revelation from the real world that might give her a good reason to keep pausing on interest rate rises. It could be the start of a lot of economic indicators that scream it’s time to stop the monetary tightening altogether.

In today’s AFR, Michael Bleby points out a significant development that CoreLogic has reported in its regular surveillance of the property market.

What this data-collection group has found is that over scheduled auctions have spiked to 1,518 from 1,428 in the space of the week and what’s noticeable about these numbers is that they’re described as being “unreasonable” for this time of the year.

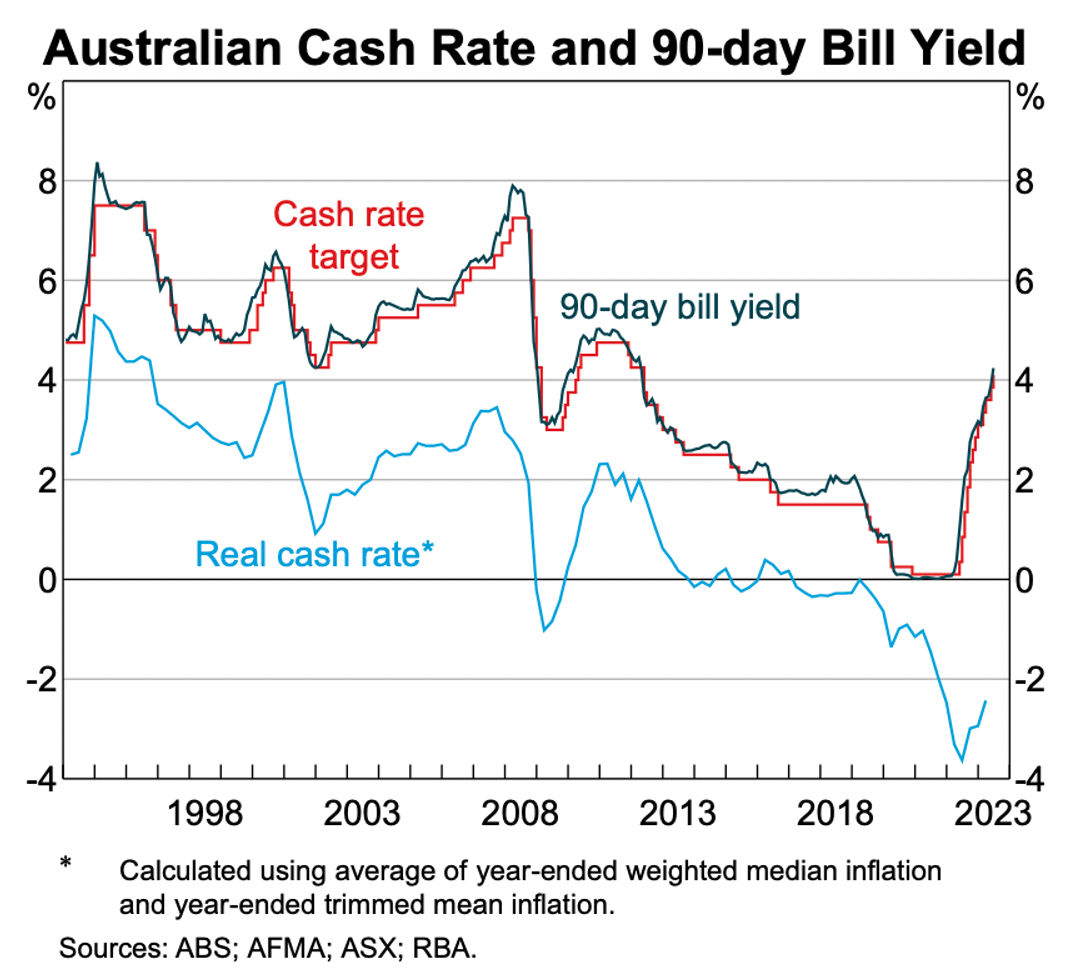

This has led AMP’s Chief Economist Shane Oliver to refer to this development as the “…long awaited rise in distressed selling.” Like me, Shane has argued that enough has been done by the RBA pumping up the cash rate of interest from 0.1% to 4.1% over 12 out of 14 meetings, in a little over a year. This chart below shows how dramatic those rate rises have been.

Shane and I have long argued that monetary tightening (i.e., raising interest rates) works off a long-time lag, and that the mortgage cliff was bound to kick in when we got to the second half of this year. In fact, it was the RBA’s new governor who told us that about one million households were set to experience the belt-tightening effect on their spending from their low fixed rate mortgage going to a high variable rate home loan.

That’s when those 12 rate rises will give the central bank the bang it has been looking for from those excessively fast hikes in the cash rate that has forced home loan rates over 5.5%. On that subject, that 5.5% rate is primarily for refinancing not new borrowers.

Right now looks good for sellers, with clearance rates high and buyers enthusiastic but the supply has been constrained. What seems to be changing is that these new potential sellers are saying: “Let’s get out while the going is good.”

These are early days for the impact of the mortgage cliff, which was always slated to start in June. By early next year, it’s likely to have affected most of these million borrowers, who fixed for four years or borrowed on fixed terms in early 2022 before rates went berserk!

The point of monetary tightening is to slow down spending to beat down inflation. Michelle Bullock will be hoping for economic data to show that her predecessor Dr Phil Lowe will make her a very likeable RBA boss, who ultimately decides that it’s time to wait a little longer before raising rates again.

The case for pausing for longer than one month was made when the US received a bigger-than-expected fall in inflation to 3%, while the core rate dropped to 4.8%, which was the lowest since October 2021.

This all makes this week’s release of the minutes of the last RBA board meeting (when rate rises were put on hold) an even more gripping read as a guide to what Ms Bullock decides to do at next week’s rates meeting.

I say she should persist with the pause, but that’s my view as an economist. You might need to be a psychologist to work out what Michelle Bullock and her board are likely to do.

I’m hoping they’re mentally stable enough to give pausing a little longer, especially with those figures pointing to a rise in the number of homes going up for sale.