13 July 2025

1300 794 893

Overnight the Yanks got their latest inflation number that was slightly higher than hoped for, and OPEC and its oil-producing members helped stop the nice fall in the CPI in the US. Meanwhile, on the local front, distressed listings of properties are on the rise.

In these two cases, central bankers in the US and Oz potentially face two different questions.

In the US, because inflation was slightly higher than expected, the Federal Reserve (which meets on rates next week) could raise rates or wait to see what happens between now and the rates meeting in November. Either way, my expected surge in stock prices is set to happen once we know that the chance of the Fed raising rates again has been put on hold. Mind you, most smart economists and market players either think there’s one more rate rise in the US, or upcoming economic data will determine what happens in November and beyond.

At home, we’ve seen progress of falling inflation. This is how Trading Economics saw the latest data drop: “The monthly Consumer Price Index (CPI) indicator in Australia increased by 4.9% in the year to July 2023, slowing from a 5.4% gain in June and below the market consensus of a 5.2% rise. This was the lowest inflation rate since February 2022, mainly due to a slowdown in housing and food prices, although it remained well above the Reserve Bank of Australia's target range of 2-3%.”

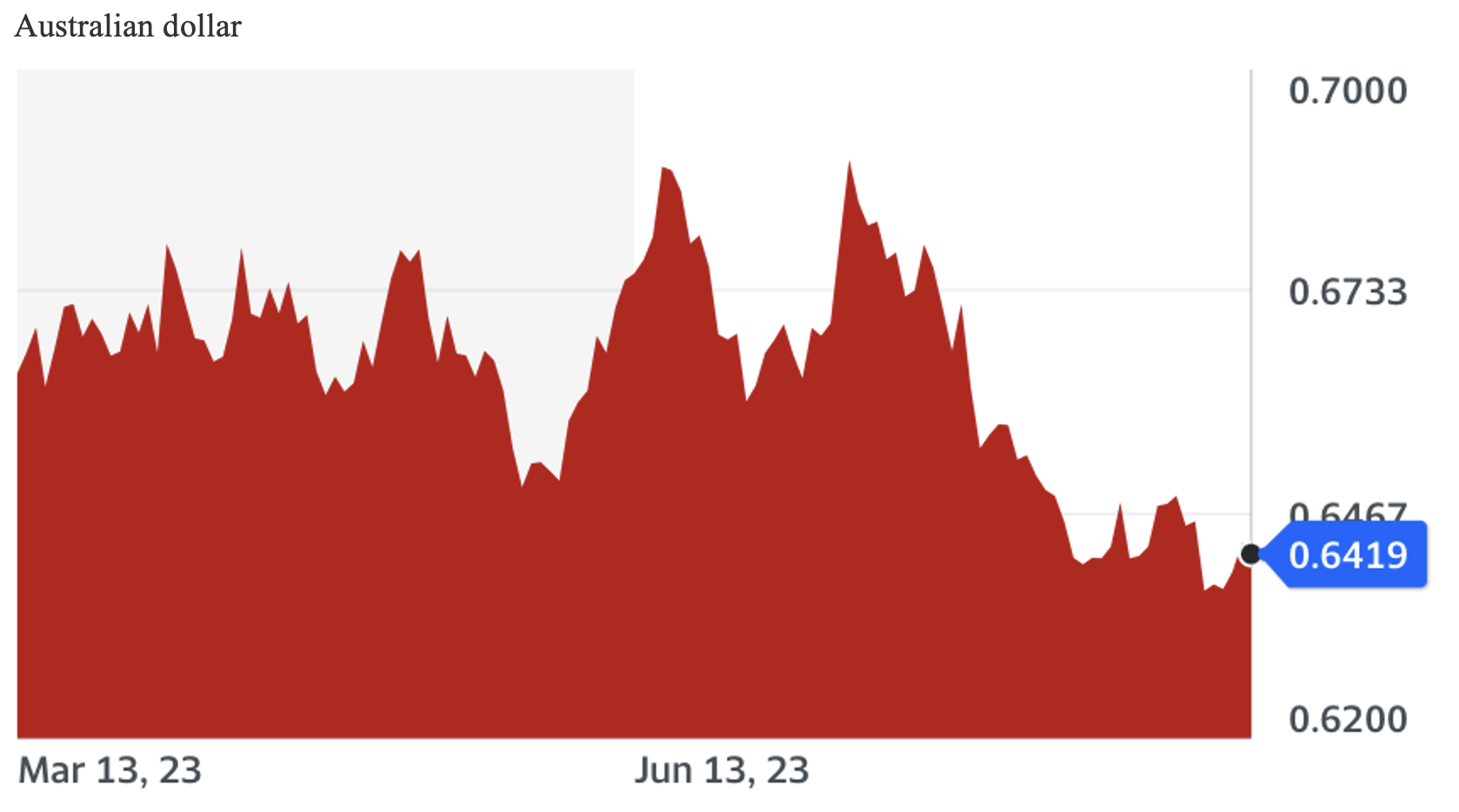

The trend is good, but the level of inflation remains high. This means we can’t relax and feel confident that the Reserve Bank here is done and dusted with rate rises. But the consensus is that rates have hit the top, which is why the Oz dollar has dropped in recent weeks. Overnight it was a little softer at 64.18 US cents because that inflation number was a little hotter than was hoped. (Economics lesson here: If we look like we’ve stopped raising interest rates, but the US could go one more time, then the greenback becomes more popular with those investors who chase higher interest rates and that increases the demand for the US dollar compared to our dollar.)

Before we got that surprise improvement in inflation and the RBA went into ‘on hold’ mode, the dollar was at 69 US cents. This drop is because the RBA looks done with raising rates, but the Fed could go one or even two more times if the data doesn’t get more worrying in the US.

Yes, the US needs to see their 11 rate rises hurt the economy and inflation a little more to make it certain that no more rate rises are needed there.

In contrast, the data here is making our monetary or interest rate policy look like a better policy. Maybe you could say that Dr Phil Lowe was good at creating inflation through rates that were too low, but he was also good at killing it with rates that are too high!

In reality, our monetary policy does work better because in Australia less home loan borrowers have fixed rate loans. In America, 90% of home loans are fixed for 30 years, while here it’s usually only 15%.

Because of the very low fixed rates offered in the pandemic, 40% of loans became fixed between two and four years. But having 60% of loans variable helps our RBA get an economic reaction when they hike rates.

Yesterday we saw how the mortgage cliff is starting to work, which should be good for inflation and no more rate rises here in Australia. The mortgage cliff says that as borrowers on fixed rate loans have to roll onto higher variable rate loans, they’ll feel the drop in their overall income and spending as their repayments increase.

Today the AFR tells us that “the proportion of distressed listings has almost doubled in some heavily mortgaged areas such as Blacktown in Sydney’s west during August, amid signs some households may be starting to buckle under the pressure of higher interest rates and weaker economy.”

Nila Sweeney puts it even more precisely with this: “More than one out of seven homes listed for sale in the Blacktown district were selling under distressed conditions – a sharp rise from a year ago when only 8.7 per cent were distressed, data from Domain shows.”

Happily, not all areas are experiencing distressed selling, with the percentage falling in Sydney — 4.7% last year to 3.3% during August.

“It fell from 2 per cent to 1.6 per cent in Melbourne and from 6.6 per cent to 4.2 per cent in Brisbane,” Sweeney reports.

All up, it looks like our interest rate policy is working better than the Yanks’ rate rises. That’s why our dollar is under pressure. However, this dollar weakness isn’t expected to last. Both NAB and Westpac see the dollar rising to 69 US cents or higher by year’s end, but we do need to see US inflation to fall further for that to happen.