17 July 2025

1300 794 893

The last quarter of 2023 was a ripper for stocks, which helped a lot of super funds, that were underperforming (even compared to term deposits) to end the year with returns they’re now crowing about. By the way, they weren’t as public about their performance earlier in the year.

That said, the super story of 2023 underlines important messages people need to understand about investing for returns better than term deposits, which incidentally are around 5% for a one-year fixed term and heading lower.

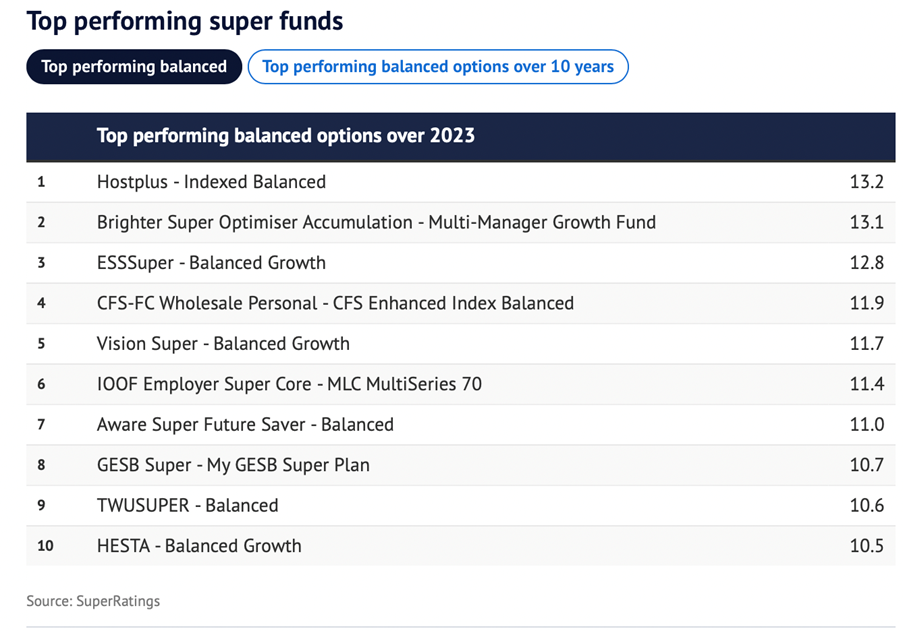

This table from SuperRatings shows the best performers for 2023. The 13.2% return for the Hostplus Indexed Balanced fund continues this fund’s historically good showing. However, you do have to be careful about one-year performances and you have to be careful about comparing funds because they’re not all exactly the same, even if they all call themselves balanced. Why? Keep on reading!

In the world of financial advice, a balanced investor has a 60% exposure to stocks and 40% exposure to defensive assets, such as term deposits or bond funds. In fact, advisers are made to put clients into a 50:50 mix of stocks versus defensive assets when their clients are deemed as being balanced.

However, in the world of industry super funds, the word “balanced” has different meanings to different funds.

Be clear on this: the average good super fund returned 9.6% for the year ending 2023 but most of these funds would have had a bigger exposure to stocks than 60%. The 2023 winner, Hostplus, can have up to 76% of their clients’ money in stocks and that’s how it would’ve got a 13.2% return. Industry funds also invest in other assets not on the stock market and here the valuations used are sometimes ‘questionable’.

In July 2022, the AFR questioned the value Hostplus put on its investment in local hotshot design company Canva, when the company’s private share value was reportedly down more than what the fund was valuing in its unit price.

This is the way the AFR’s Tony Boyd revealed the story: “Two of Australia’s leading superannuation funds – Hostplus and Aware Super – have revealed different approaches to valuing the country’s most successful, privately owned technology company, Canva. This will add fuel to the vexed debate over superannuation fund valuations of unlisted assets at a time when Canva shares have plunged by up to 60 per cent in the secondary market.”

All this makes comparing fund performance difficult. That said, I prefer to look at longer run returns from super funds because that gives you a good idea of how they consistently invest for success, and it gives you the real return you should expect out of the best super funds. “Hostplus Balanced is the best performer over the 10 years to December 31, 2023 with an average annual compound return of 8.3 per cent,” the SMH’s John Collett reports. “Second spot is shared by AustralianSuper Balanced and Australian Retirement Trust Super Savings Balanced, each with an average annual compound return of 7.9 per cent.”

But a more important number is 6.8%, which is the long-term average return from the typical super fund.

Also, when you want to compare funds, you have to look at the risk option selected. A growth investor in a fund like Hostplus could have earned more than 13.2% because they had a bigger exposure to the stock market, and especially the US market.

Collett explains the difference in returns depending on what risk option you select. “Calculations by SuperRatings shows an investment of $100,000, 10 years ago, in the median-performing balanced option would now be worth about $189,000, assuming no additional contributions have been made,” he explained. “If someone had put $100,000 into the typical capital stable option 10 years ago, their account balance would have grown to about $148,000 now.”

Capital stable options are more conservatively invested than balanced options, with exposure to growth assets of between 20 and 40%. Capital stable options are favoured by retirees as their returns are less volatile than balanced options.

The important lesson is this: if you’re afraid of losing money because of the ups and downs of the stock market, you can’t expect to get an average return of 6.8% per annum, which average balanced super funds have delivered. By being risk averse, you dial down your potential returns to around 4% or 5% a year.

Finally, all this information isn’t advice as I don’t know your appetite for risk. It’s meant to be educational information. If you want to take actions with your super, make sure you do your homework, talk to advisers and check out ASIC’s Moneysmart website.