4 July 2025

1300 794 893

There’s been a whole pile of super whinging this year after ScoMo allowed desperate and worried Australians to access $20,000 from their funds to cope with the economic implications of the Coronavirus. And the super funds weren’t only complaining about that. Helped by the godfather of super, ex-PM Paul Keating, they didn’t like hearing that the scheduled 0.5% increase in compulsory super paid by employers mightn’t happen next year.

This would take the super slug on employers to 10% but the Treasurer is arguing that the economy, workers and consumers might want the money now rather than see it buried in their super funds for a comfortable retirement.

It’s a bit like: What do we want? Comfort! When do we want it? Now!

Of course, this isn’t the cry of everyone. If the virus hasn’t threatened your job, your income or your future, and interest rates on your loans have shrunk to unbelievably low levels, then you’d probably want your super increase.

But if you’re young, property-less and wealth-aspirational before retirement, you might want that money now. You might be asking: “With property prices so high, how am I ever going to buy a place if I lose 10% of my wage to super each year?

You might be even saying: “Those damn baby boomers with their homes didn’t have to pay into super until 1992, when most of them would’ve had a house and were on higher pay because of their experience!”

Of course, the baby boomers could return fire and say: “Our bosses weren’t forced to put 9% of our pay into super and you youngsters will retire with over a million dollars in your super funds!”

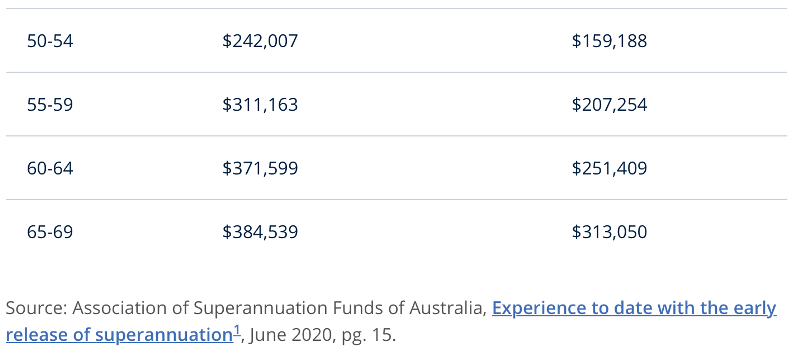

This chart shows how hopelessly low the super of older Australians is.

Older Australians Super Balances

But back to the now story. In September, the ABC revealed that “nearly 2.8 million people have been approved to withdraw more than $34 billion from their retirement savings under the COVID-19 early access program.”

This led the likes of Paul Keating to be stressed out about the future retirement incomes of young Australians to be substantially reduced when they eventually retire.

However, better-than-expected positive news might offset the negativity that was pedalled by those who like to be doomsday merchants.

Yesterday a new financial planning client asked me if I thought stocks would rise in 2021, considering the big rebound in share prices since March 23. Our market is up 47% (after falling 37%) but to get back to where we were, our stock market has to rise by 57%.

This led me to suggest that I wouldn’t be surprised to see a 10% gain in stocks next year, as the vaccine increases the chances of normalcy showing up faster than expected. Only today, the first UK person received a vaccine, and yesterday Microsoft’s Bill Gates predicted that there would be six vaccines in operation in the March quarter. This is a powerful force for stock prices and eventual super returns.

Looking to see if smart people agreed with me, I found the world’s most influential investment bank Goldman Sachs has tipped stocks will rise by 16% in 2021! And yep, if that’s right, super funds will have a great year next year, which could help make up for those who needed to withdraw super funds to get through their personal 2020 Coronavirus crisis.

So in a sense, what the virus took from super, the virus could give back to super. Next year was never expected to be a great year, as the first year of a US presidency is generally the weakest for Wall Street.

On the other hand, the first year out of a recession is generally a good one, and this one will be powered by the biggest global stimulus ever and the lowest interest rates ever!

And if you need proof that this terrible virus is creating economic outcomes that could help justify these positive views on stocks, look at these numbers from yesterday:

If these numbers (which show both business and consumer confidence is actually higher than they were before we ever heard of the Coronavirus) don’t reduce your inclination towards negativity, nothing will. However, despite your perpetual pessimism, your super fund is bound to go sky high next year, unless your negativity makes you tick the box for a cash or conservative investment strategy!