6 July 2025

1300 794 893

The Reserve Bank of Australia and Governor Phil Lowe will have a new board thrust upon them by Treasurer Jim Chalmers. And it’s not a reward for a job well done. At no stage has the Government ever roundly bagged the Big Bank but it’s obvious that there is a “not happy Phil, not happy” tone behind this change.

But why?

Until the pandemic struck, Dr Phil Lowe was highly regarded as a smart economist and was always seen as the right man to progress out of the bank to replace Glenn Stevens, who was the former Governor. Like most central bankers, he responded to the Coronavirus and its surprise economy-killing lockdowns by cutting interest rates.

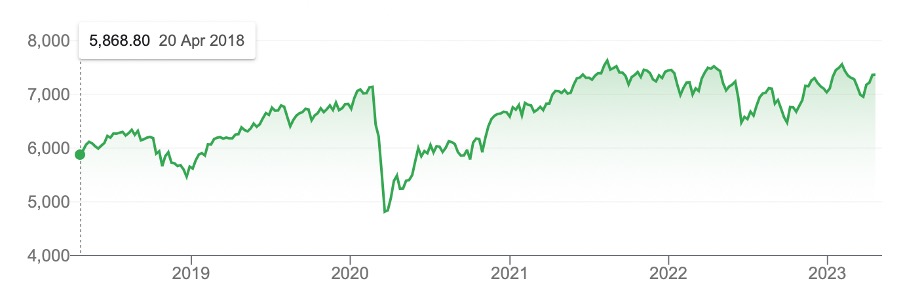

That led to big borrowing, buying of both properties and other retail goods and helped the recovery of the economy, which was then shown or mirrored in the big bounceback of the stock market.

That big drop in the S&P/ASX 200 and the ensuing rebound was the good work of Dr Phil and Treasurer Josh Frydenberg with his JobKeeper, along with the state governments who spent billions to save us going into a Great Depression Mk II.

This was a period when any Prime Minister and Treasurer would’ve been thinking: “Happy Phil, so happy.”

In trying to keep up confidence and feed the economic bounce back, Dr Phil then made a big call that has come back to bite him.

This is how the ABC remembered the story: “The Reserve Bank has been under political scrutiny during the pandemic for indicating that interest rates would not likely rise until 2024, but since lifting the official cash rate at nine consecutive meetings, taking it from 0.1 per cent in April to 3.35 per cent this month as it tries to bring inflation under control.”

Now that there have been 10 rate rises. And Dr Phil has actually been honest in saying that he’s not sure if he has done too many rises, or whether he’s done enough. These actions have not only worried those with big mortgages, who borrowed too much on his 2024 rates call, but also the Government.

Dr Jim and PM Albo must be concerned on both the economic and political fronts of the fallout of this aggressive interest rate rise policy. So, the news that they’re putting an oversight board on the RBA and Dr Phil shows Australians (let’s call them voters) that they will try to make the central bank better at its job.

The AFR’s John Kehoe says the change involves a new governance board that “…would oversee the bank’s operations such as human resources, finance, risk management and technology, similar to a corporate board at a major company”.

The other board would do the job we see the existing board doing, namely setting interest rates and will be made up of “experts on economics, labour markets and financial markets”.

Kehoe informs us this two-board model is like the Bank of Canada and the Bank of England, which is interesting to note, but neither bank is famous for great interest rate calls.

All this comes as two new board members are due to join the board and Kehoe says the Coalition’s support for these changes could rest on who is appointed to replace environmental expert Wendy Craik and Fortescue deputy chairman, Mark Barnaba, who used to work at Macquarie Bank.

These changes will help an RBA boss do a better job, as Dr Phil and his predecessors have had too many tasks to oversee. But there are other problems with the RBA that Gordon de Brouwer, the Secretary for Public Sector Reform pointed out. Here's Kehoe on what Dr de Brouwer observed: “Culturally among the RBA’s 1,400 staff, Dr de Brouwer said hierarchy and silos should be broken down to encourage debate and contestability from staff at different levels and to improve decision-making. It’s not as open, it’s not as contestable, in terms of its internal debate as it could be.”

This is the point I’ve made regularly. You have to ask the question: Why didn’t someone on the board or the whole board simply tell Dr Phil that his 2024 call was excessive and could cause overborrowing? That’s exactly what I said on 2GB at the time, when I was asked if I believed rates would be on hold for three years or so.

My response was “No”. My experience as an economist and someone who has watched and commented on our economy over a long time meant that I warned listeners and readers that the 2024 call was bound to be wrong.

The RBA board should have done the same thing. If Dr Phil wasn’t prepared to back down on his call, they should have called him out as being wrong. The silence of the sheep-like board on this subject either shows that the board was as wrong on the subject as the Governor, or they didn’t feel it was their place to criticise their leader.

Either way, change was necessary. That’s what Dr Jim is imposing on Dr Phil. It should be interesting if the latter’s job is renewed when his seven-year contract ends in September. Don’t get me wrong — I like and respect Dr Phil Lowe but he made a bad call and his board did nothing to change that call. Inexperienced borrowing Australians now find themselves in a money-crushing situation after 10 rate rises from Dr Phil and his board.

And tougher critics than me might even bag the RBA outfit for the high inflation and the slowness to raise rates, which might have meant fewer rises. I won’t go there because I know how hard it is to get interest rate settings right, as I’ve seen so many central bankers fail this test so many times.