4 July 2025

1300 794 893

What we’re seeing today is the anatomy of an economic slowdown and, ultimately, a reduction in home price growth, which will then bring with it price falls. Oh yes, and if things get out of hand, we could be talking a recession. But let me pick up the vibes by saying I won’t get too worried about that until late 2023 or 2024.

So what’s the catalyst for the very rarely seen negativity from one P.Switzer? It’s actually two related revelations.

The first says that after looking at the seven and a half-year high of the underlying inflation rate on Tuesday for the December quarter, the consensus of economists now says that official interest rates will rise in August and not December. December was the old view but the RBA was basically implying that was too early.

Dr Phil Lowe, who runs the RBA, was initially a “rates won’t rise until 2024” guy, but lately, he has hinted that earlier was possible, if the economy goes gangbusters, wages are spiking and inflation becomes too hot to handle.

Second, it’s what the Telegraph’s John Dagge has done with these interest rate rise speculations. He’s the first to show us how our mortgages will be affected. And he kicks off by telling us that “the average homeowner will be coughing up close to $170 a month extra to cover their mortgage by the end of the year amid growing expectations the Reserve Bank will soon start hiking interest rates”.

Deutsche Bank Australia’s chief economist Phil O’Donoghue expects an August rise of 0.15% and then two more 0.25% increases by Christmas — what a gift!

Dagge then relies on Rate City’s calculations on what higher rates like Phil’s will do to home loan repayments. “Analysis from RateCity shows a homeowner with a $500,000 mortgage paying a variable mortgage rate of 2.98 per cent over 25 years would need to find an extra $168 a month by December if those predictions pan out,” he writes. “The hikes would take payments from $2,366 a month to $2,544 a month. A homeowner with a $1 million mortgage would need to cough up $336 a month extra.”

And that coughing will be manageable but as more and more rate rises happen over 2023 and 2024, the negatives from home loan borrowers will outweigh the positives of a booming economy, lots of jobs and decent wage rises.

The economy will slow, company profits will slip, share prices will fall and the boom could turn into a bust by 2024 or 2025. But that’s what happens in economies and stock markets. The taking away of money from borrowers is the start of the eventual slowdown and recession that economists expect over time.

That said, stock markets rise 7-8 years out of 10 and have a history of paying about 10% per annum on average — half of which comes from dividends.

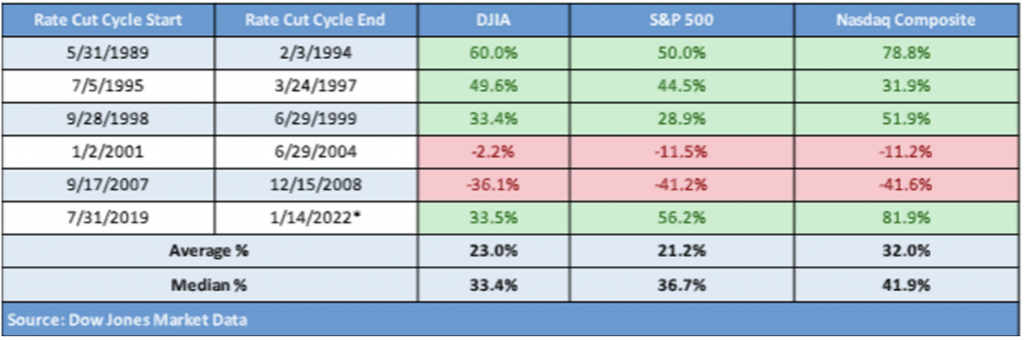

And this US table shows that rising interest rates don’t smash the economy and stock market in the early years of rate rises.

Looking at the first line in this table, you see the interest rate rise cycle between 1989 and 1994 saw the Dow Jones index up 60%, the S&P 500 up 50% and the Nasdaq up 78.8%. And four out of six times stocks rose strongly with rising rates.

So it might pay to remain positive on our economic future until we see how many rate rises we get and just how powerful the post-pandemic economic boom turns out to be. The latter could offset the costs of rising interest rates for a couple of years at least, if history is a good guide.