24 February 2026

1300 794 893

In a week when the Reserve Bank is certain to cut interest rates, the home loan market and, undoubtedly, property prices are set to surge if recent applications for lenders’ money is any guide.

The Australian reports that new figures by mortgage brokerage Loan Market have revealed that following the RBA's February cash rate cut, pre-approvals were 43% higher (!!!) than in the same period last year.

Given most economists expect not one but three rate cuts this year and a possible fourth early next year, you don’t have to be Harry Triguboff, Tim Gurner or John McGrath to work out that this will help bring buyers back to auctions and Saturday afternoon browsing for a property.

What we will see is the opposite of the mortgage cliff, which said borrowers who were on COVID-driven very low fixed rate home loans would fall over a spending cliff when they were forced onto higher rate variable home loans.

So did that warning come to pass?

The RBA told us in 2023 that around 880,000 fixed-rate loans expired in that year, with another 450,000 due to expire by the end of 2024.

One aspect of the “cliff” was that borrowers would fall into arrears. While that didn’t become a scary issue for banks and other lenders, spending did fall away, so consumer discretionary outlays of holiday, furniture, cars and other retail did suffer.

Ask Airbnb if holiday lettings fell and the answer is yes — big time! And many retail business owners have hit the wall as rate rises killed spending. Even now borrowers are saving money coming from the two rate cuts this year.

I’ve often said to audiences that Aussies would sell their granny into captivity before they stop paying their home loan and gave up their precious quarter acre block or apartment!

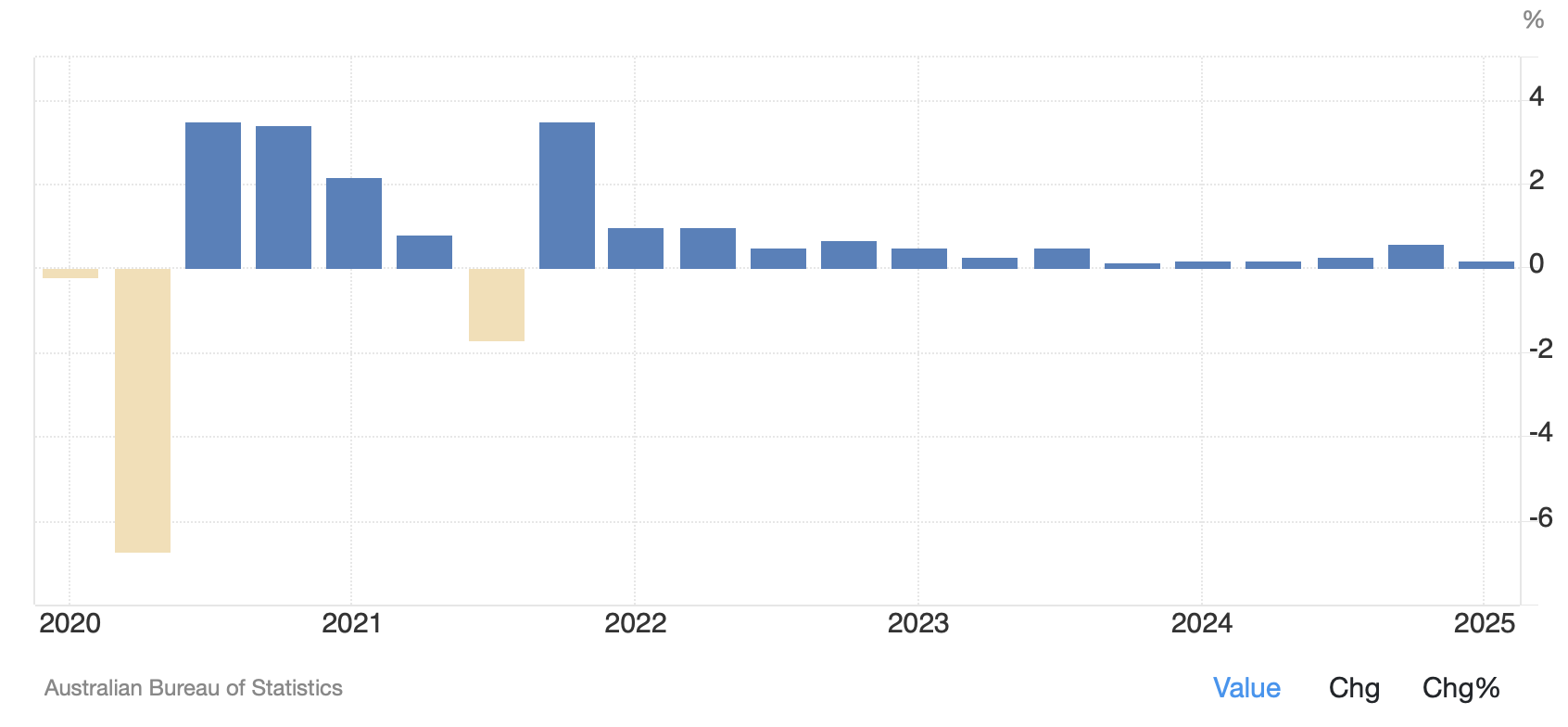

This chart shows a cliff-like retail slump from 2023 after rate rises started in 2022.

And the chart below shows how economic growth has slumped over the period of late 2021 to now. While this is another indicator that the mortgage cliff happened, it just wasn’t as steep as the media and other alarmists portrayed it.

Want more proof of the cliff effect? Check this out from Creditor Watch as reported by the ABC:

“Hospitality closures hit a record high of 9.3 per cent — one in 11 businesses — in the 12 months to February, up from 7.1 per cent in the previous 12 months as customers under cost-of-living pressure cut their discretionary spending.”

So, what’s behind this 43% surge in loan pre-approvals?

Loan Market research says the rise is linked to rising buyer confidence following the February rate cut of 0.25%. Since then, there has been another one in May. Then there are the news reports of the likes of AMP’s chief economist, Shane Oliver, who’s tipping cuts in July, August, November and February.

The Loan Market research also points to a surge in listings for the upcoming Spring sales period that’s also getting would-be borrowers out inquiring about a possible loan.

First homebuyers and people wanting to upgrade their homes are leading the charge to get the tick for a possible loan, with many applicants driven by FOMO (the fear of missing out) as they expect three or four rate cuts to lead to a stampede for properties that will drive prices up.

So, will the RBA give us a 0.25% or 0.5% cut on Tuesday? Given the slowdown in the economy and the expectation that official rate cuts will come in July and August, a jumbo half-a-percent cut would be great for stimulating the economy, but the RBA could worry about the house price effect.

I’m sure they will want to keep their powder dry for helping the economy in case Donald Trump’s tariffs, expected to be revealed this week on July 9 leads to a collapse of global trading and economic confidence. If this happens the central bank might go with a 0.5% to try to avoid a tariff-related recession.

Note, while this is a worst-case scenario that I don’t expect to happen, second-guessing the most unpredictable US President ever is not a very wise strategy.

This could be a huge week for our views on rate cuts going forward. It would be the first time that someone in the White House had such a huge influence on what we pay for our mortgage!

As the decisions of Donald Trump hit us daily, never have the words of James Brown “Living in America” meant so much to us here in Australia.

Living in America (yeah)

Hit me

Living in America

Living in America!