19 July 2025

1300 794 893

The legendary US comedian, Bob Hope, once observed: “A bank is a place that will lend you money if you can prove that you don't need it." This came back to me when news outlets reported NAB had been taken to court for cruelly ignoring customers pleas for help because of hardship circumstances, which in one case the bank ignored the request for help for 694 days.

Another NAB customer reached out for hardship assistance in January 2020 and said she had been directed to make a hardship application by the bank’s staff after leaving a long-term domestic violence relationship.

The Australian’s David Ross reported that this customer waited 1,756 days for a response rather than the 21 days the law says a bank must take before reaching out to a customer in trouble.

So, the frontline staff knew this was a case with merit but someone up the line and with more power chose to ignore the matter. And for someone like me, who knows the corridors of corporate power, this reflects on the top leadership of a company.

All up the Australian Securities & Investments Commission says NAB failed to respond to at least 345 customers seeking help, which breached the bank’s requirements. We don’t expect the bank to be too generous to all of their customers, who are feeling the pinch because of say 13 interest rate rises and when they’ve overborrowed, but when they have suffered traumatic circumstances, a bank is expected to help.

Ross looked at the circumstances when a bank is requited to assist: “This included customers fleeing family violence, suffering medical emergencies, or locked in their homes during the Covid-19 pandemic who reached out to NAB seeking pauses on payments for home and business loans.”

To be fair NAB did self-report its failures but also to be fair, it followed Westpac being charged for similar failures to its customers one month earlier. On the plus side, it shows that ASIC’s actions against the banks is working.

“NAB’s failures likely compounded the already challenging situation for these people,” said ASIC chair Joe Longo. But it is a pity that big corporations need to be sued to do the right thing by customers.

We have seen once respected companies such as Qantas, Woolworths, Optus and others let their loyal customers down, ignoring not only their hardship circumstances or the implications of their pricing actions or failed risk management policies but failing their shareholders by trashing their brands via unfavourable media coverage.

The Australian provides a photo of NAB’s current Group CEO, Andrew Irvine but this terrible behaviour happened under the former CEO Ross McEwan.

In August this year Yahoo Finance’s Stewart Perrie looked at bank CEO’s annual pay packets, giving the payments gold to bronze medals for the top three earners and this is what he discovered: “Coming in at number three is the head honcho for NAB, Ross McEwan, and he pocketed a cool $2,383,654 last year. Interestingly, that was the lowest base salary out of the four CEOs, but it was his other streams of revenue that pushed him into bronze.

“He had a little more than $45,000 in ‘other’ income and copped a hefty bonus of $3,746,795. This took his total yearly income to $6,176,092.”

The irony is that nowadays we reward CEOs who save money ignoring hardship cases, who then generate surprise bigger and bigger profits and higher share prices, by giving them bonuses.

For years, banks and other big businesses have signed up for ethics courses for their staff and have ads, like NAB’s “more than money” line but the evidence suggests governments need to give regulators such as ASIC and the ACCC more money to bolster regulation.

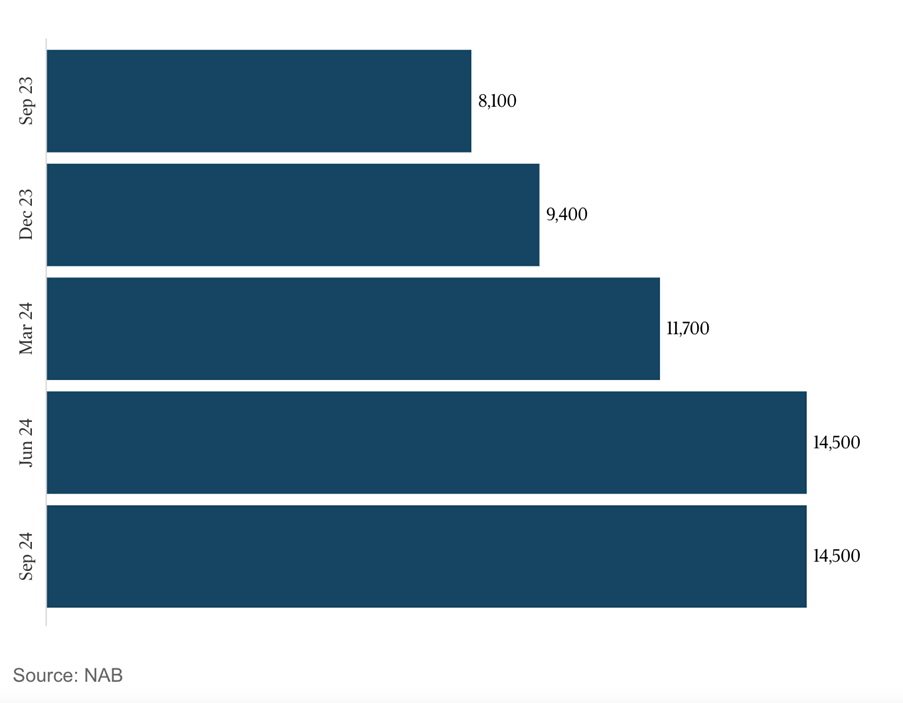

By the way, this is not to say NAB has not ignored all hardship cases as the chart below shows.

However, the failures covered here show they have a caring problem and as the old the proverb goes: “…fish rots from the head down”.

When there is a problem in an organization or system, it usually starts at the top with the leadership or those in charge.