5 July 2025

1300 794 893

The team of economic guess merchants called economists quoted by the media had recently switched their expectations of the first rate cut to May, until the National Accounts showed we’d been growing by 0.3% for the September quarter and 0.8% for the year.

That saw my economist buddies flip over to February for the first cut and the money market ‘bookies’ that set the prices on bets on when rates will move had a 70% call for a February cut.

However, that all changed when the Australian Bureau of Statistics delivered the latest jobs report. Low and behold, despite 13 interest rate cuts and an economy growing at an anaemic 0.8%, unemployment fell from 4.1% to 3.9%!

All this is timely as the Treasurer names the new team who’ll be on the board that sets rates going forward today.

In case you forgot, the Reserve Bank wants to see the jobless rate rise, not fall, to think about giving us a rate cut. As a consequence, economists have returned to their May rate cut call and the money market has February at 50:50.

Importantly, that 0.8% growth number was for the year to the end of September. We’re nearly at the end of the December quarter and it would be a surprise if we’re not growing even slower. But who knows in this crazy economy, when 13 rate cuts can’t KO the job market and slow down spending enough to bring core inflation into the 2-3% band?

I do think we’re in an especially ‘crazy’ economy following the impact of Covid lockdowns, big government spending to warn off a deep recession and record low interest rates, which helped unemployment fall to modern times record lows.

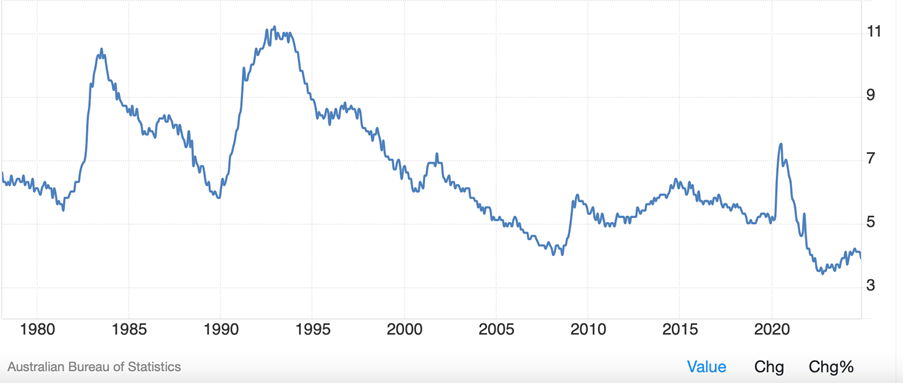

Australian Unemployment

Throw in the work from home trend, the spending to boost alternative energy and the high price effects on power bills, and we really do have a tough economy to predict.

We know economists are having difficulties because they’re always changing their forecasts around when rates will fall. And we know the RBA has been nonplussed by the current economy because it has failed to get inflation down to where it wants it in order to start cutting. Its failure to raise rates say 15 times might be the cause of its rate cut delay now. If you look around the world, the big rate raisers are now big cutters.

Here's AMP’s Shane Oliver on cutting all around the world: “Meanwhile, the drum beat of global rate cuts continues, with the Bank of Canada, the ECB and Swiss National Bank cutting rates again in the past week. The Bank of Canada cut by 0.5% to 3.25% and flagged a “more gradual approach” going forward. Nevertheless, with falling inflation, nearly 7% unemployment and threats to growth from US tariffs it’s expected to cut to 2.5% next year.

“The European Central Bank cut its rates by 0.25% taking its deposit rate to 3% and moved more dovish by dropping a reference to keeping policy ‘sufficiently restrictive’. It’s likely to cut to 1.5% next year on the back of low inflation and weak growth with Trump’s tariffs not helping.

“The Swiss cut by 0.5% to just 0.5%, but it’s doubtful other central banks will get that low! Of global central banks latest decisions, around 45% have been to cut, around 50% have been to hold and only around 5% have been to hike.”

Oliver thinks the RBA should cut sooner rather than later for these reasons:

Oliver thinks when rates start to fall the cash rate will go from 4.35% to 3.6% by year’s end, so that’s a 0.75% fall. But given how badly economists have ‘guessed’ this crazy economy, I can’t suggest you put your money on his best guess!

On January 29, we get the next quarterly CPI for December and the next jobs report on January 16. If these indicate falling inflation and rising unemployment, the RBA could surprise and cut in February.

Given the RBA’s history, of “being late to the party” (as Paul Keating once said) to raise and cut rates, I wouldn’t be putting my dough on a February cut, despite the fact they should!