19 July 2025

1300 794 893

The PM opened up the AFR’s Business Summit yesterday and his speech was an election pitch, giving us a running showcase of how great his Government has been and will be if we re-elect him. But he didn’t totally sugar-coat what lies ahead by saying: “Now I said at this event last year, you cannot run the economy on taxpayers' money forever. It’s not sustainable.”

And that’s fiscally true but we need to get a fast-growing economy to let the Government and the taxpayer off the hook. When the economy grows quickly, taxes roll in and government spending falls because more people have jobs and businesses invest, reducing the need for the public sector to create business and employment opportunities.

Right now, we’re growing well with the 2021 annual growth rate coming in at 4.2%. The latest December quarter was 3.4%. This was the strongest pace of growth since the third quarter of 2020, mainly boosted by a sharp rebound in household spending, as the economy emerged from COVID-19 lockdowns.

But there are headwinds, making it hard for the Government and taxpayers to be let off the hook.

The Ukraine war is pushing up the price of oil, which will slow growth. And the floods will reduce growth and demand for Government/taxpayer spending. It’s like we’re living through the seven curses or plagues of Moses. In recent years there have been mice, locusts, floods, fires, war and even a plague with the coronavirus!

All these problems hit economic growth and then the public purse, which then helps growth happen (with all the much-needed repairs) but it leaves a taxpayer bill.

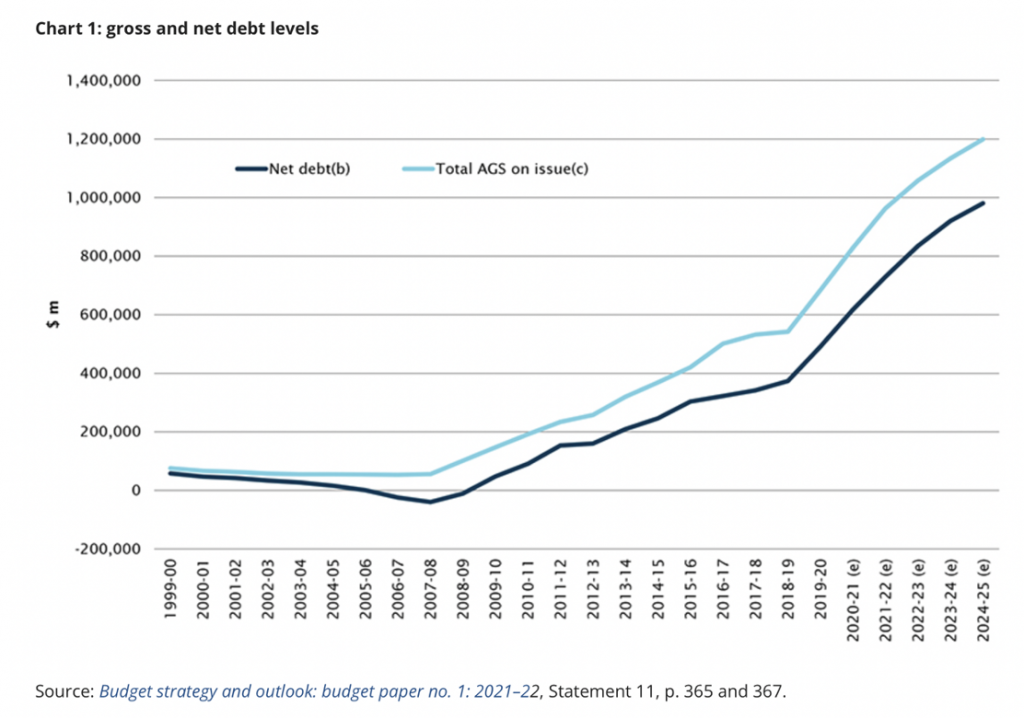

The latest Budget projections say that the Commonwealth government’s Gross Debt will be about $963bn at 30 June 2022. This is about 45.1% of GDP. It’s projected to increase to $1,199bn (about 50% of GDP) by 30 June 2025. This is huge by Aussie standards.

The more accurate measure of our real debt is Net Debt, which is expected to be $729bn (or 34.2% of GDP) at 30 June 2022 and peak at $981bn (or 40.9% of GDP) in 2024–25. Net debt is then projected to fall over the medium term to 37% of GDP at 30 June 2032.

Net Debt takes away what others owe the Government from what it owes, so it gives the true picture of our indebtedness.

The chart below shows how our indebtedness has spiked, first because of the GFC in 2008 and then 2019-20 with the Coronavirus.

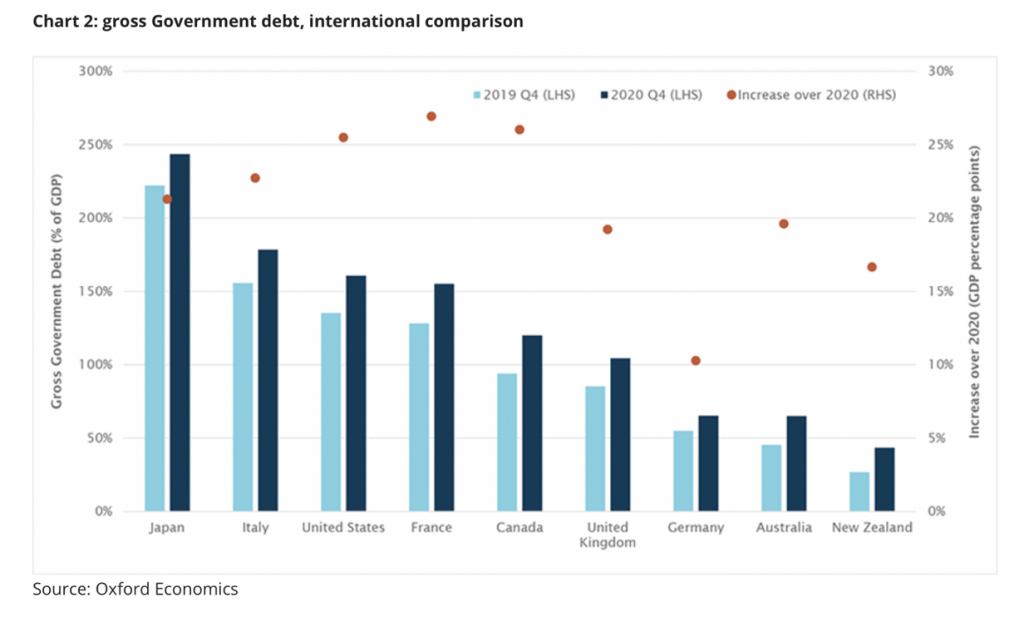

And while this doesn’t look great (and it isn’t), it’s miles better than countries we compare ourselves to.

Japan has Gross Debt of close to 250% of GDP, the US 150% and the UK at 100%, so their taxpayers are in for a belting one day when the world economy can avoid pandemics and Putin!

Our biggest wish has to be that the West can come up with an agreement to stop this war in Ukraine, so the loss of life, economic opportunities and oil prices can be reduced.

That will spark the stock market up and set the scene for strong economic growth. ScoMo is underlining how business-focused his Government will be and is trying to imply that Labor under Anthony Albanese won’t be.

Right now, Albo is not making Bill Shorten-type mistakes by threatening retirees and businesses with a tougher tax regime. This partly explains why he looks set to win the next election, expected in May.

All that lies ahead, but I have to share this with you and it’s a pearler from the PM, who understandably is looking for pre-election endorsements. And this one comes from arguably one of the greatest entrepreneurs and brains of all time!

This comes from ScoMo’s speech to the Summit: “We have one of the lowest death rates in the OECD - a performance nine times better than the OECD average. We have one of the highest vaccination rates in the world. Almost 95 per cent of Australians aged 16 and over are fully vaccinated. No country, of course, has got everything right - I’ve been very candid about that - when it comes to COVID. Nor could they claim to.

“But I think most of you will have noticed, in the audience, and would regard Bill Gates as a fairly objective and well-informed observer on these matters. And a couple of weeks ago, at the annual Munich Security Conference, he cited Australia’s COVID-19 response as the gold standard.

“In the context of future planning, Bill noted that: 'If every country does what Australia did, then you wouldn't be calling [the next outbreak] a pandemic. They [Australia] orchestrated diagnostics, they executed quarantine policies, and they have a death rate in a different league than other rich countries’.”

ScoMo added: “And while other countries ‘had the capability to do that’, as Bill pointed out, in Australia, we actually did it.”

This certainly is an election year, so get ready for more of this kind of stuff!