9 July 2025

1300 794 893

In case you haven’t worked it out, if inflation falls, then the interest rate rise scenario becomes less scary and stocks will go up. However, if the price rise story isn’t a positive one, where the consumer price index (CPI) numbers and the related indicators don’t scream that central banks are winning the war against inflation, then stocks will fall.

The most important battleground for stocks is the US, but for local interest rate worriers, the homeland economic data will be the big watch.

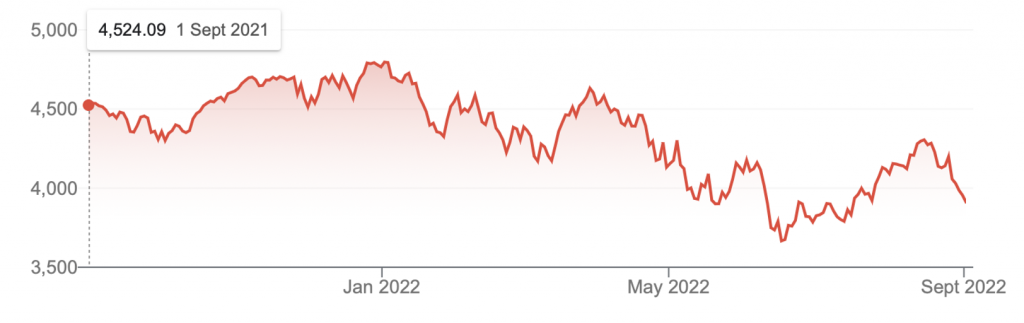

We’ve seen since mid-June that Wall Street has bought stocks whenever it thinks inflation is slowing and interest rates might be close to the top. This chart shows the rebound that happened when the market started to believe that the US central bank i.e., the Fed, was close to easing up on its aggressive rate rises.

S&P 500

That spike that started in mid-June was looking promising until the Fed’s chairman, Jerome Powell, basically said he’s not easing up on rate rises. He didn’t say that he might if the economic data says he’s winning the war against inflation but he’d be thinking it because he knows if he goes too hard he could cause a serious recession.

So he will be looking at two pieces of economic data over the following few data days that could help or hurt stocks in the US and then here.

The first comes tonight (Friday, US time) when the jobs report is released. A survey of economists forecasts that 300,000 new jobs should show up in August but if it’s bigger than this, it could be bad news for stocks, because big job creation indicates that the rate rises aren’t slowing the economy enough to beat down inflation.

A smaller jobs number will be cheered by Wall Street and the focus will go to September 13 (that’s Tuesday week) when the Yanks will get the August inflation number. The July reading was 8.5%, which was down from the 9.1% reading in June, so if we see a 7% or so reading on September 13, the market will like that.

Of course, every other economic reading from then will be assessed for what it says about inflation, but the number one number for stocks will be the US CPI out on Tuesday week.

On the subject of Tuesdays, next Tuesday our Reserve Bank has another crack at reducing our inflation rate. We economists will be surprised if Dr Phil Lowe doesn’t hit us with another 0.5% rise in the cash rate.

This will take the cash rate (that the RBA controls and which drives changes in home loan rates) to 2.35%. And this could be the last rise for a while if our economic readings continue to look negative.

Most economists think the cash rate will go to at least 2.6% or higher by year’s end, but like Jerome Powell in the States, Dr Phil will be influenced by what the economic data implies about what’s happening to inflation.

Looking at recent data, we are seeing indications that interest rate rises are starting to bite. These numbers show that:

1. The CoreLogic Home Value Index of national home prices fell by 1.6% in August, the fourth straight monthly decline, and the biggest monthly decline in almost 40 years (since January 1983).

2. Regional home prices fell by 1.5% in August – the biggest drop in 32½ years (since November 1989).

3. The value of construction work done fell by 3.8% in the June quarter – the biggest decline in 4½ years (since December 2017). Total construction fell by 4.3% on a year ago to a 5½-year low of $52.1 billion.

4. The weekly ANZ-Roy Morgan consumer confidence index fell by 0.7% to 85 points (long-run average since 1990 is 112.2 points).

5. New business investment (capital expenditure) fell by 0.3% in the June quarter.

6. The number of dwelling approvals fell by 17.2% in July to 13,595 units. It was the second biggest monthly percentage decline since December 2017. Approvals are down 25.9% on a year ago.

7. The total value of new home loans fell by 8.5% in July — that’s the biggest fall in new home loans in 26 months.

8. The AiGroup manufacturing index dropped by 3.2 points to 49.3 in August, indicating a contraction in activity (reading below 50).

I’m not sure the bad news above is enough to encourage Dr Phil to ease up on the rate rises, but if he goes for a 0.5% rise next week, I reckon the data flow will really start to show that his rate rise torture is working. He too doesn’t want a recession, but the RBA boss won’t see the official September quarter inflation here until October 26.

However, the ABS is now releasing a monthly reading on inflation, so that could help interest rate worriers believe that the RBA will soon be ‘done and dusted’ with rate rises.

By the way, if our rate rises end before the US, that will be a plus for local stocks. Our relatively low inflation rate at 6.1%, with the US at 8.5%, the EU at 9.1% and the UK at 10.1% (and going higher) is something that in part explains why our stock market has been outperforming Wall Street.

As you can see, every upcoming data day could be HUGE, because inflation has to fall or rates will rise, and that’s bad for stock and house prices.