8 July 2025

1300 794 893

The past 12 months has been a great year for investors who weren’t frightened about the war in Ukraine, the tragedy in Israel and Palestine, the relentless rise of interest rates, China’s eyeing off Taiwan and the prospect that Donald Trump could again be the leader of the Western world.

I had a client go to term deposits when the Middle East hostilities broke out and lost $70,000 in making a unilateral decision to sell her stocks and bunker down. There was no discussing the matter. All of a sudden, with no track record of successful investing, decided she could be her own adviser.

I know of people who’ve been scared since Covid and have remained term deposit bound and lost hundreds of thousands of dollars in recent years because they gave into fear and loathing of what the stock market might do.

Mind you, given the fact that the media makes its relevance by focussing on negative, scary stories (and, apparently, psychology says humanity seems to take the worrying news more seriously than the blue sky stuff), it makes sense that some people turn tail and run when the world is in crisis.

The value of honest advisers comes via a number of valuable money-making channels. The first comes when the adviser can help you deal with short-term bad news and then encourage you to stay invested in a time-proven way of growing wealth through stocks, term deposits, bonds, property and other assets.

Some advisers can be suburban Warren Buffett’s and make better investing decisions than others, but most get advice from good callers of markets and smart asset consultants, who more times than not create good money-making portfolios.

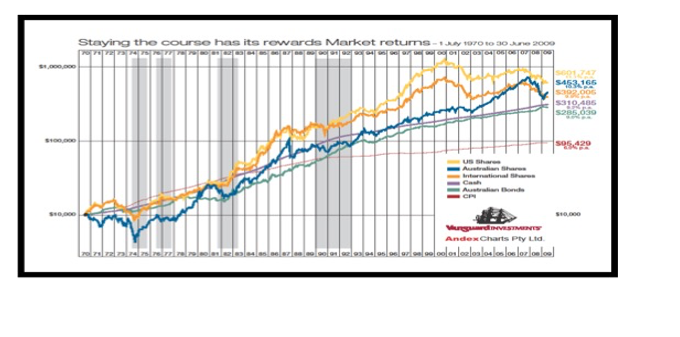

Of course, shock events such as Covid or the GFC can rock clients and advisers, but that’s where the latter should take control of their clients’ emotions and show them charts like the one below.

The blue line shows that if someone invested $10,000 in 1970 in something like an exchange traded fund for the All Ords or S&P/ASX 200 Index and kept the gains reinvested, by 2009, one year after the 50% collapse of the market with the GFC, that $10,000 snowballed into $453,166.

This shows the magic of compound interest, when you believe in and invest in quality assets, such as the top 200 companies that make up the S&P/ASX 200 Index. Effectively, you’re investing in Australia’s best-listed businesses, which isn’t a bad idea given our economic track record.

Lots of people go to financial advisers to hopefully get better annual returns than they would get. I have to say the returns we’ve got for our clients have ranged from 10% for the conservative types to 23% for a real growth player.

However, this isn’t an every-year achievement. We always tell our clients that we aim for around 7% but try to make decisions that could better this return.

That means we might hedge investments for a rising dollar, which we’ve been doing lately as we expect the Aussie to head towards 70 US cents plus in coming years. We have been taking 5% plus term deposits now because we think these rates will fall in the years ahead. We figured that the Nasdaq would do well a year or so ago, once US interest rates topped out and we liked both the overall US and Australian stock markets, so we played them via two exchange traded funds.

Right now. We’re looking to invest in small caps because they tend to do well when interest rates fall and so do emerging economies.

All these considerations go into our views on what our clients should be invested in. But some of an adviser’s best work is knowing the clients’ goals and then the super and tax rules that can make a huge difference to how much money someone might have in super when they retire.

It surprises me that many people don’t know the contribution rules for super so they have money outside of super on which they pay tax rates much bigger than the 15% or 0% that can apply to super earnings.

And then there are those over 55 who don’t know that they can sell their house they’ve owned for 10 years and put a lump sum each into their super. Meanwhile, some couples are unaware that the partner with a too big balance, if retired, can draw out money and put it into the other partner’s super fund. This combined approach can maximize the amount the couple gets into super, upon which the tax rate on earnings is the best rate of 0%!

What I’m saying is, if you’re not super savvy or someone who’ll become an expert on the super, tax and other investing issues, it might be false economy to try and do it yourself.

Even if you have your super in a good industry fund, my history talking to clients has shown that too many people don’t get the right advice or simply haven’t heard about opportunities that would maximize their super and retirement nest eggs.

One last example, and this shows even younger people, who want to buy a property, can gain from guidance.