19 July 2025

1300 794 893

A big part of my job is to warn you when I think the stock market is ready to slide, or when it’s poised to go significantly higher. Forecasting/guessing where the market is going isn’t a precise science, but I can draw some guidance from the Arts, history in particular, and, of course, the social science of Economics to make my best calls.

I can’t expect to be right in the short term because there are so many speculative and overreactive factors that make getting it consistently right so hard. However, the medium term is easier and long term is easier again. It’s why I have a good feeling about the trajectory of stocks over 2024, despite headlines from the likes of the AFR’s Chris Joye, such as: “With saving buffers nearly exhausted, 2024 will be grim.”

More on Chris and his worrying call later.

The strongest pointer for me being right on stocks has been the November reaction for share prices since it looked like the US has probably topped out with its rate rise cycle, with the Nasdaq especially showing the relief that stock players have enjoyed since US inflation looked tamed by the Fed. The US has been getting better-than-expected inflation news from late October, and then on 14 November they got very good inflation news. “As expected, year-on-year headline inflation fell from 3.7% in September to 3.2% in October on the back of a 2.5% decline in energy prices,” said Shawn Snyder, Global Investment Strategist for J.P. Morgan Wealth Management. “Gasoline prices dropped by 5% during the month, providing the consumer some needed relief.”

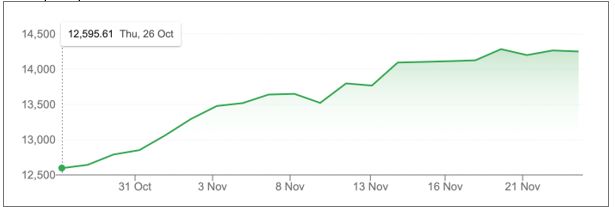

Nasdaq Composite

This was the first time that good potential inflation news from related indicators such as the labour market were backed up by good actual CPI data. I’ve been saying for months that stock prices would be governed by inflation data and November vindicated my predictions. This chart above of the Nasdaq with its 13.1% rise since 26 October graphically shows what I’m saying.

I’ve also argued that when it looks like the inflation dragon was tamed, small cap stocks that have been ignored and even smashed since November 2021 just before interest rates were hiked, have made a nice comeback. The Russell 2000 in the US is up 9% in a month, and I suggest that when we KO our inflation threat, that’s when we’ll see a nice rebound in stocks. That time is highly likely to be next year, though it looks like it has already started, albeit a lot slower than US markets.

The S&P/ASX 200 is up 3.1% over the past month, despite a Cup Day rate rise and a plethora of excessive negative talk about future rate rises, “homegrown inflation” and a lot of jawboning from RBA Governor Michele Bullock.

But how do we factor is Chris Joye’s “grim” outlook with a positive view for stocks?

First up, let’s have a look at what he’s saying.

In a world where inflation is falling, it looks like our rate of fall is slower than most. Chris shows us why with this observation: “Australia is the stand-out in terms of the breathtaking size of our consumer buffers, which peaked at $315 billion, or 13 per cent of annual GDP.”

He's talking about offset accounts and mortgage accounts where borrowers have overpaid their monthly amounts and so they have buffers that they can use to soften the blow of the RBA’s rate rises. This helps them not reduce their spending by as much as if they had no buffers, but it also de-powers monetary policy. This partly explains why the RBA’s assault on inflation has looked ordinary.

Those buffers are still big. Chris says this will force the RBA to do more rate rises. He’s predicting rising unemployment, more home loan defaults and the likelihood of a recession, but that will either force the RBA to stop raising rates or make them cut.

I also think no one has a true handle on the impact of the mortgage cliff that’s yet to be an issue for a large number of borrowers, who’ll go from low fixed rate loans to high variable loans.

While the first four months of 2024 will be critical for what the RBA does and what might happen to the economy, once the market thinks rate cuts are coming, stocks will spike. They’ll also spike if we get some surprisingly positive news on the CPI this week on Wednesday, and then on January 10 followed by January 31.

With US stock prices embracing a bounce-back, inflation on the slide here would be a great setting for our market. And if it can come with better news out of the Middle East, and China successfully stimulating its economy, then 2024 should deliver on its promise.

On the US market comeback, the AFR pointed to a note “…from Bank of America strategist Michael Hartnett, which reported that $US16.5 billion moved into equities this week, lifting the inflow the last two weeks to $US40 billion.”

While this big inflow could lead to a slight pullback as smarties take profit, the momentum says Wall Street will give us a lead higher in 2024. If we can nail our inflation problem, then our market will join the race for stocks.

What would I buy? Here’s what I like:

1. ETFs for the whole market, such as VAS, IOZ and A200.

2. IHVV, which gives you the US S&P 500 with hedging for a rising $A.

3. GEAR for the real risktakers and don’t think about it if you can’t stand losses!