6 July 2025

1300 794 893

Be afraid. Really, either be afraid or the Reserve Bank’s Michele Bullock will make you afraid. And if you don’t get scared ASAP, it could be your house or job that could be threatened. Some unlucky blighters could lose both important life achievements.

This is the message conveyed by both the newly released RBA minutes and what the new governor of our central bank put out there at the ASIC forum in Melbourne this week.

If you want to be optimistic, you could say that this is jawboning by the RBA boss. Central bankers like to do this to try and avoid too many potentially recession-creating interest rate rises. However, if you want to be pessimistic, you could say that the governor is really worried that inflation will stay higher than she and her board wants. So, if the inflation data doesn’t say we’re afraid and we’re not spending, then more rate rises are coming,

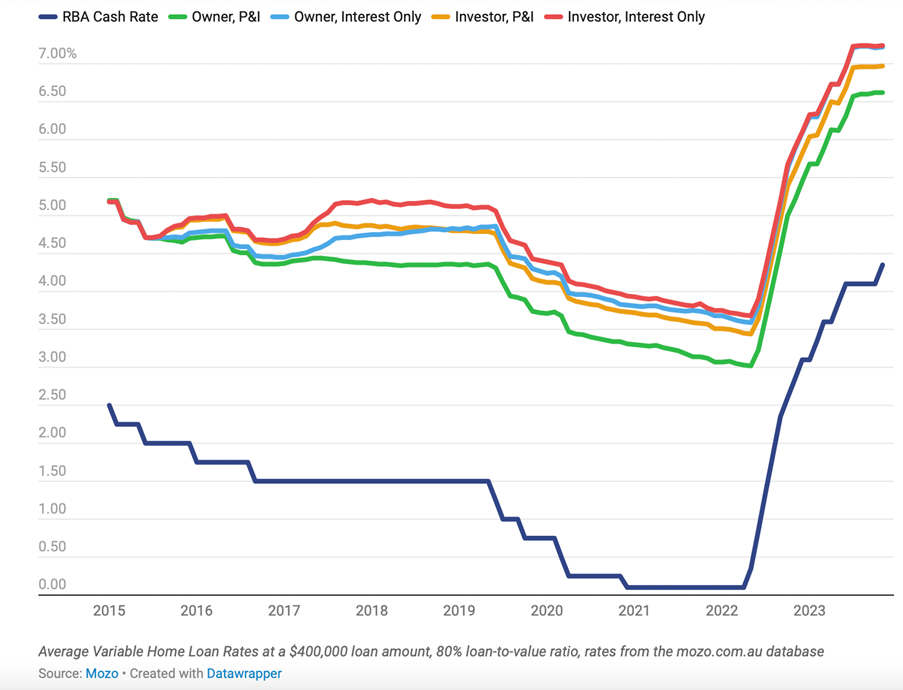

Some of us are afraid and are cutting back on spending as home loan repayments are rocking many borrowers. In case you need convincing, this from ratecity.com.au is sobering reading: “For a borrower with a $500,000, 25-year home loan that was paying the RBA’s existing average owner-occupier variable rate of 2.86% in April 2022, the last cash rate hike could mean your home loan repayments are $1,210 a month higher. It means someone with a $1 million home loan has to find an extra $2,420 a month (or $29,040 a year) to keep up with their repayments! This chart below from mozo.com.au graphically shows the pain home loan borrowers have endured since May 2022 when rates started to move higher.

Seven days ago, this is what we saw from the latest consumer sentiment reading: ““The Westpac-Melbourne Institute Index of Consumer Sentiment declined 2.6% to 79.9 in November, down from 82 in October.”

Melbourne University economist Dr Viet Nguyen made these observations: “The RBA’s November rate hike has put renewed pressure on family finances and reignited concerns about both the rising cost of living and the prospect of further rate rises to come…The weak November sentiment print is an ominous sign heading into the Christmas high season. Pessimism is having a major bearing on spending attitudes”.

AMP’s chief economist, Shane Oliver looked at these stats and said: “[This] consumer survey showed consumer confidence wallowing at recessionary levels and nearly 40% are planning to spend less on gifts this Christmas”.

However, there was a concern about the optimism that business is showing. Here’s Oliver again: “By contrast, business confidence remains far more resilient and business conditions are above average”.

Clearly, the businesses doing well are those not servicing the stretched home loan borrowers but it shows the problem the RBA has. Its rate rises are disproportionately hitting one third of the spending households who have a mortgage. The other two thirds must be helping business and not assisting in bringing inflation down.

At the ASIC forum, the RBA head did accept that some of the inflation is supply or cost-driven but added this: “...there’s this underlying demand component to it as well, that is actually something that central banks can do something about”.

While that’s true, how are her rate rises affecting others who aren’t borrowing?

CBA economist Belinda Allen looked at the RBA minutes and concluded that rates would rise if inflation didn’t fall sufficiently. That said, the CBA expects the cash rate to hold at this level – it’s 4.35%, but if inflation doesn’t come down sufficiently, then rates will rise.

The AFR surveyed UBS economist George Tharenou who “…declared the minutes so hawkish that he now sees the possibility of another two rates rises, as the central bank struggles to dampen demand driven by booming population growth and a record $145 billion paid in superannuation benefits in the year to September 30.”

So, even retirees, accessing their super via a pension, are spending and not helping the inflation fight. In fact, Ms Bullock’s rate rises actually make these people richer via better term deposit rates, which in turn helps them spend more!

We’re in a tricky situation and that’s why the RBA governor is trying to scare us into less spending, but she only really frightens those with big loans and no offset accounts.

Inflation data better come in better over December and January, where there are two monthly readings and one quarterly number, or else the RBA will raise again. That could lead to a recession, which will hit more people, because not only do jobs disappear but house and stock prices fall and then interest rate cuts follow, and these are aimed at repairing the damage from too many rate rises!

This is why we should get scared ASAP and its why Michele Bullock is wise to talk tough and scary because every future rate rise could be one spike too many, and she knows this.

The gift I want for Christmas is good data on inflation that will save us from the worst-case recession scenario I described above.