12 July 2025

1300 794 893

It’s the worst-case scenario for local interest rates with the chief economists of our major banks and other financial institutions piling in to tell us that we should expect up to five rises in the half-year after the May election! For those overborrowed, this could be worrying news and should make these people start doing their homework on how to prepare for a lower cash flow future.

Of course, these number-crunchers could prove to be wrong and we end up with three or four rate rises, but it would be foolish to not believe that you, as a borrower, will be paying a lot more to service your loan by year’s end.

Why? It’s simple. Inflation is on the rise and we don’t know how high it will go and how long it will rise for.

Why is inflation going higher? Try these causes:

1. The Ukraine war has taken oil prices up nearly 60% this year until recently and they’re still up 25%.

2. The war is restricting the supply of stuff worldwide, which adds to costs for producers.

3. The pandemic has hit Chinese suppliers to the world as evidenced by the lack of microchips, which has reduced the supply of new cars and increased their prices.

4. There’s a post-pandemic, economic rebound going on worldwide, and along with the war, this has pushed up the price of resources such as iron ore, copper and other mining products along with agricultural commodities.

5. Unions are starting to demand higher wages to help their members cope with rising inflation, which is set to get worse.

6. The post-pandemic world (with different attitudes towards working in the office versus doing it from home) is bringing extra costs onto businesses, and these will be passed on by those operators who have pricing power.

Today the SMH tells us that the economics teams of the big four banks now think our first rate rise will be on June 7 and because the RBA has a cash rate of interest of 0.1% (created for the abnormal Coronavirus-infected Aussie economy), the first bump up will be 0.24%.

If the bank economists are right, then we could see four more quarter per cent hikes from the RBA, which would be promptly passed on to borrowers by the banks. And it partly explains why bank share prices have done so well lately.

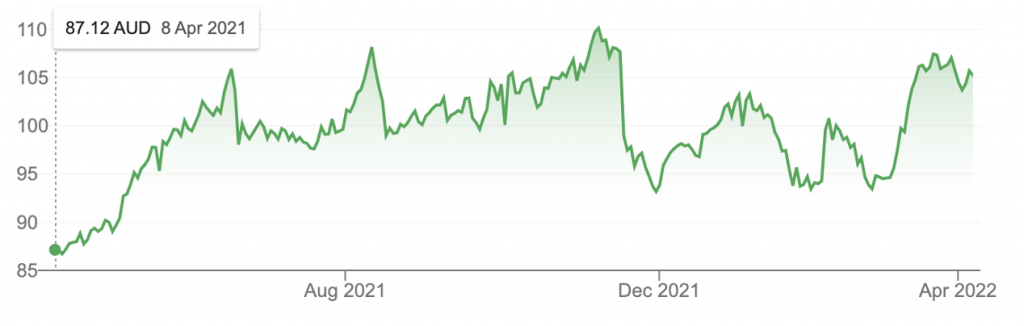

CBA one year

CBA’s share price is up 20% in a year and provided these rate rises from the RBA are not too ‘stupidly’ fast, and we don’t go into a serious economic slowdown (or even a recession as some have predicted), then bank share prices will go higher.

Regular readers know I never bought the RBA Governor’s story that rates might not rise until 2024, but I also don’t think he’s going to go mad raising rates this year unless he thinks the economy can take it.

The big worry is that those who locked in fixed home loan interest rates at 2% during the pandemic will have to renegotiate their loans in 2023 and 2024 and home loan rates for them could be 4% or higher!

Motivating the economists to get bullish on lots of interest rate rises sooner than was expected was a change in wording from the RBA Board’s statement on Tuesday. “Over coming months, important additional evidence will be available to the Board on both inflation and the evolution of labour costs to support the case for an interest rate hike,” the statement read.

It also noted inflation “has picked up” and “a further increase is expected”, but it still needs to see labour costs lift.

Economists especially noticed that the Board had dropped its intention to be patient in watching for inflation but there is one reference worth noting from the statement, that might hose down the fire that economists now have for expecting lots of interest rate rises this year.

The Board is saying it needs to see “labour costs rise” before they will be full-on committed to many interest rate rises to bring the cash rate back to about 2% or a tad higher.

I must admit I’m surprised that the economists have ignored the 22 cents-a-litre in the petrol price and the recent fall in the oil price after the US released barrels of oil from its strategic reserves.

The SMH reports that “Westpac and Commonwealth Bank are predicting five RBA rate rises in the next six months, while NAB and ANZ are predicting four rises”.

However, if peace comes to Ukraine sooner rather than much later, the oil price will fall quicker than expected.

And if China beats its pandemic problems quicker than expected, then we might see some supply chain costs subdue but these are longshot hopes.

Four or five rate rises are not a done deal for 2022, with wage rises being important for the RBA’s ultimate decision, but you’d have to expect by 2023, we could’ve seen seven or eight rises, especially if the economy is going gangbusters.

You have been warned.

This means you should be preparing your finances for a possible 2% rise in your home loan interest rate. If that will be hard for you, it might be time to get into a lower interest rate home loan now.

For those who want to fix, ratecity.com.au shows St George has a three-year fixed rate at 3.74%, which might be a benchmark to use to see if you can get the best deal possible. And remember, check out the comparison rate on all loans you take out, as this rate tries to add in any extra charges on top of the interest rate.

In fact, you should compare all your total costs of a loan per month, when comparing one against others. As interest rates rise, your prime goal is to have good cash flow so you can meet your repayments and fund your lifestyle.