4 July 2025

1300 794 893

This isn’t news but economists are split on whether the RBA is done and dusted with interest rate rises. It’s not news because economists seldom find it easy to agree on anything, with some even thinking Dr Phil Lowe did a good job and shouldn’t have lost his gig.

In fact, Dr Phil is a good economist and a good man but made a fatal mistake with his call on interest rates not rising until 2024. Economists on the RBA board and many professional economists didn’t get stuck into him for a silly prediction, showing that economists aren’t to be over-relied on.

I will concede that occasionally I do get it wrong. Recently my incorrect call will cost me an expensive dinner in a Melbourne restaurant! Why? Well, I told a Queenstown conference of mortgage and financial brokers at Mark Bouris’s Vow and Yellow Brick Road groups, that I thought the RBA wouldn’t raise rates again. However, the June rise brought me undone, though I think one day that rise will be seen as unnecessary. What I’m saying is 12 rate rises since May last year will be seen as excessive by year’s end because the mortgage cliff effect will be an inflation crusher over the next few months.

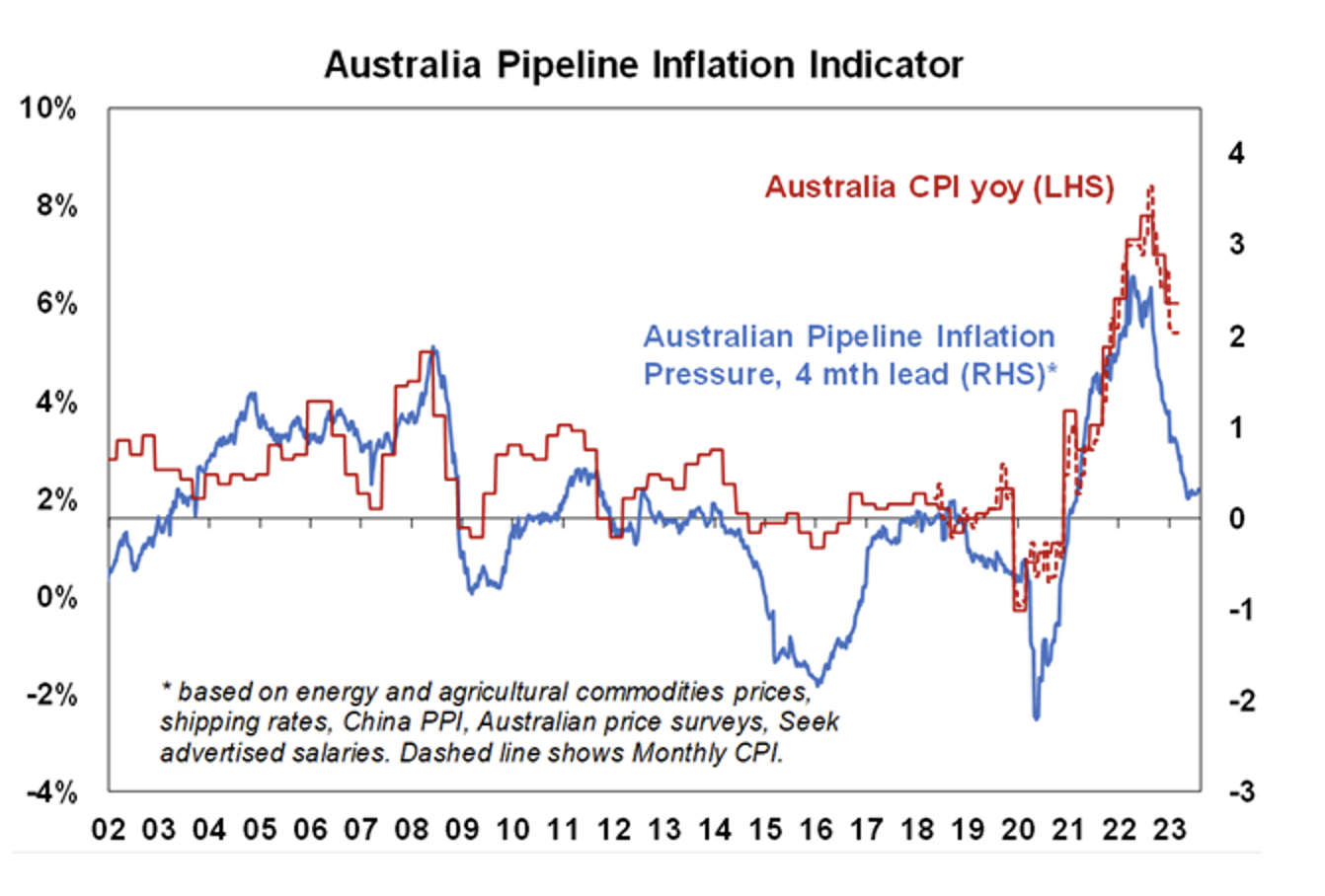

Last week I identified this chart from AMP’s Shane Oliver as the “Chart of the Week” for my subscribers to our investment newsletter called The Switzer Report.

The blue line is the Pipeline Indicator. See how it has fallen rapidly, while the red line for the official Consumer Price Index (CPI) is following it, though a few months behind.

When it comes to getting inflation down to between 2% to 3%, as Rachel Hunter said in the famous Pantene TV ad: “It won’t happen overnight, but it will happen.”

We learnt yesterday from economist Carlos Cacho of Jarden that “…$32 billion in fixed loans would expire in each of the three months to September – the peak rate of a roll-off to variable loans that would total nearly $550 billion over the 15 months to March 2024.”

One of my work colleagues said yesterday that she rolls off her low fixed rate loan in October and isn’t looking forward to it. Neither will be the businesses that are set to suffer when smart borrowers stop buying coffee and start making it themselves with their Nespresso machines. They’ll start taking their lunch to work and many businesses will feel the pinch, which will push unemployment up.

For the record, the AFR’s Michael Read surveyed about six economists and this is what he found:

Ultimately, future data drops will decide what happens but the combined effect of the mortgage cliff and the lag that monetary policy always comes with but was stretched out because 40% of borrowers were on fixed rate loans, compared to the usual 15%.

I partially blame myself and other smarty pants commentators who told borrowers during the horror years of the pandemic that if you were going to lock in a fixed rate loan, do it for the longest period possible because you’ll never see fixed rate loans as low as this again!

Provided we don’t see another Great Depression, I think that call will be absolutely right.