12 July 2025

1300 794 893

It’s a big day for home loan borrowers, with Dr Phil Lowe and his RBA board set to nail their interest rate colours to the mast. And what they do will not only take money off Aussies, it could KO a strong economy in order to beat inflation and even push us close to a recession, especially if the Governor gets it wrong today and in the ensuing months.

In a perfect world, Dr Phil has to raise rates enough times and by certain amounts so that he brings inflation down from its last reading of 5.1%, hopefully into the 2-3% band. In doing so, he slows down the economy enough to help lower prices without pushing the economy into recession.

This would not only steal jobs from Australians, but it could also come home to roost as foreign workers return, which would push up our unemployment rate. But the bad news wouldn’t stop there, because his recession would make PM Albo’s job of getting the budget deficit down from its guessed level of a high $78 billion very difficult.

Recessions take away taxes because the jobless don’t pay them. And they get unemployment benefits, so it blows out a budget deficit that’s big because of Josh Frydenberg’s economic rescue plan called JobKeeper.

So in saving us from a Great Depression with 15% unemployment (that’s what Treasury guessed the unemployment rate would get to without JobKeeper), we’ve ended up with a huge budget deficit that needs good economic growth for a number of years to bring it down to more manageable levels.

This puts a lot of pressure on Dr Phil to get his interest rate call right. What we really need is a Goldilocks play — not too hot with big rate rises to create a recession, but not too cold so inflation keeps running at high levels.

This is what 28 economists have told a recent Finder RBA Rate Survey:

1. A third of those surveyed expect a 0.4% rise.

2. Most of the rest think the rise will be 0.25%.

3. Some outliers tip a 0.5% rise.

4. Many think the cash rate will peak at 2.5% in 2023 from a current level of 0.35%.

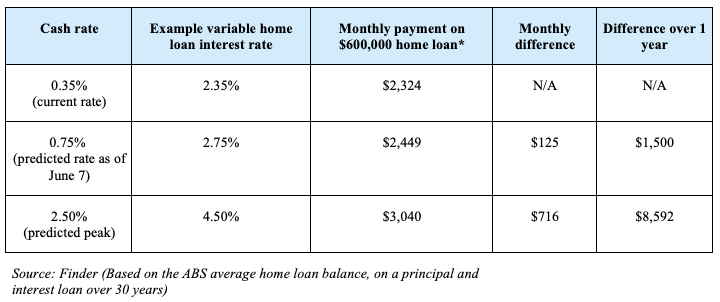

See the table below to see the impact of a 2.5% cash rate:

The big shock and awe story from this table is that someone who’s borrowed $600,000 is now paying $2,324 a month, but at a 2.5% cash rate, the jump in the variable home loan repayments goes to $3,040. This will mean that this borrower will have to find $8,592 a year to repay the loan.

And if they’ve borrowed $1.2 million, then they will have to give the lender $17,184 to cover their loan obligations!

This will KO spending on cars, holidays, renovations and retail shopping. It will beat inflation but smash the economy in the process.

Some economists think Dr Phil will stick to gradual 0.25% rate rises month after month, so he can pause if the big drivers of inflation i.e. China’s supply problems and the Ukraine war’s impact on oil/petrol/gas prices, as well as commodity prices, start to ease.

The RBA governor will be praying for a quicker-than-expected fall in the inflation rate so the cash rate might end up being about 1% or 1.25% by year’s end rather than the big calls of some economists of 2% or even higher!

The curious aspect of interest rate rises to kill inflation is that rate rises only work on demand-driven inflation, which is pretty small compared to the inflation pumped up because of rising costs.

Dr Phil will also watch how wages rise this year, and this is where our new Treasurer Dr Jim Chalmers has to pull off a big play. You see, Dr Jim wants wages to rise but doesn’t want interest rates to go sky high or else he and Labor will be accused of irresponsible economic management.

This adds pressure on Dr Phil’s decision today. If the rise is 0.25%, he could be unfairly called a misguided coward by some. But if he goes for 0.4% or 0.5%, he could be praised for possibly doing a stitch-in-time to save nine 0.25% rate rises because his soft interest rate policy kept inflation too high.

Playing the tough guy has some appeal for Dr Phil but he also knows that petrol price rises are actually like rate rises. Even with the 22 cents a litre cut in the fuel excise, households are forking out a lot more on petrol than a year ago, which makes Dr Phil’s job of raising rates even harder.

It’s a tough job but someone has to do it, and I reckon the good doctor is up to the task, but only time will tell.

Dr Phil and all home loan borrowers should be praying for the end of the Ukraine war — that would be a gamechanger for inflation, interest rate rises and the stock prices!