9 July 2025

1300 794 893

I’ve learnt in this business I’m in that I prefer to be gracious when critics get stuck into me. But today I’m going to lower myself to the level of some of my dumb doomsday merchant critics and I’m doing this for purely educational reasons.

I don’t want to call my critics ‘dopes’, but when you look at the history of intelligent investing, the doomsday mob (who think of themselves as ‘smart’ because a Coronavirus came along to stop them looking wrong again) have simply got lucky via the world’s bad luck.

Let me say, the person who decided to bet that the stock market cycle was near an end, and was prepared to get out of stocks for the past few years, can now afford to crow.

However, let’s see if being a bear on stocks is rewarding in the long term. I always told my bear critics that one day they’d be right — and if it wasn’t for that damn virus I was thinking 2021 was going to be the more worrying year but I was beaten by the economic infection from hell!

But if you only invest to, hopefully, be right in the short term, you really are a trader, speculator or punter. Some people are good at this but most of us are better off being long-term investors. For me, I’ve decided that it’s dumb to punt short-term but it’s smart to invest long-term.

Let me lay down the case for being a long-term investor.

A contributor to CNBC showed that over the past seven years for US stocks, if you missed the best 10 days, your overall returns would be halved. And that’s why getting in and out, and trying to time the market, is a risky play.

It’s why financial experts say “it’s time in the market, not timing the market” that’s important for wealth-building. I like to add that if you can get lucky or smart with your timing, say when you start investing and when you add to your investments when markets crash or heavily correct, you can do very well — but it’s still risky timing those entry points.

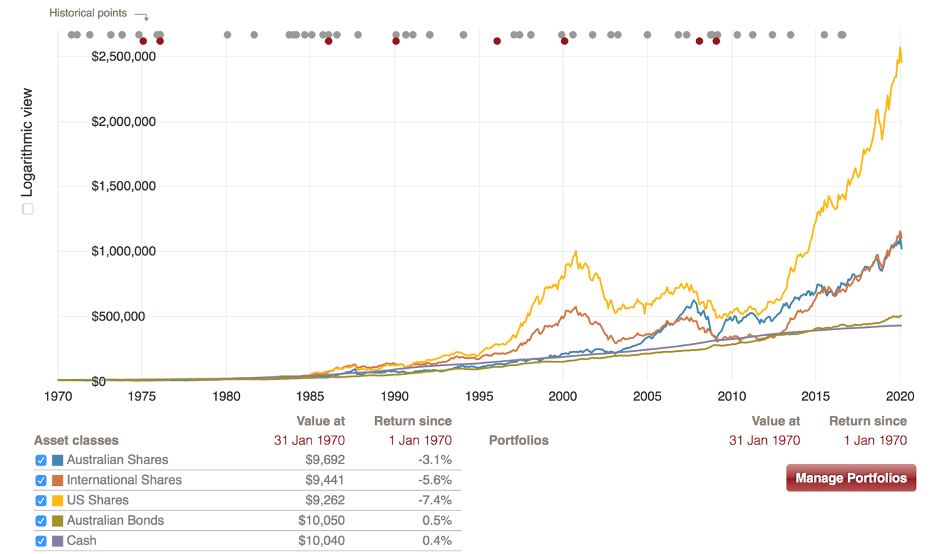

This Vanguard chart makes my best case for being a long-term investor.

The yellow line is what a US share market index exchange traded fund (ETF) for the best 500 companies could have delivered if the dividends were re-invested.

$10,000 becomes $2,500,000 plus! For Australia, the blue line has given you over a $1 million for simply being a long-term believer.

Those big drops and smaller drops on these curves are crashes and corrections when doomsday merchants felt good about themselves but few of them ever put on display the riches they’ve made over time being a contrarian doomster.

Sure, some have done really well but they’re either really smart punters or have got lucky. As someone who’s charged with the job to educate or advise others about how to build wealth over time, writing a piece like this is compulsory.

Right now, the Harry Dents and other negative celebrities out there can crow but they’ve been wrong for a long time. And if the uneducated listened to them, they could be well out of the money.

Let’s say in 2009 you were left $1 million in a will and you continually heard about how a crash and recession was coming because the GFC had created debt levels and financial market imbalances that would come back to bite us.

I fought these people (graciously and respectfully) on my Sky Business show from 2008 to 2019. If doomsters scared potential investors away from stocks and property, instead they remained invested in term deposits.

Let’s say you averaged 4% in a term deposit, after 11 years (2009-2019) it would have grown to about $1,539,000. On the other hand, if you’d bought CBA shares in 2009, you would’ve paid $34 — and for your $1 million, you’d have 29,411 shares. They’d now be worth, even after the Coronavirus crash, $1,770,000. And you can throw in 11 years of dividends that would average around at least 7% or higher, which means your dividends would’ve been $70,000 a year and over 11 years, in simple terms, that’s a colossal $770,000!

In total, your CBA investment would equal $770,000 plus roughly $1,765,000, which is the princely sum of $2,535,000!

If you were more diversified for safety reasons and you put your money into an ETF like STW, you’d be up about $2.1 million. And that’s after the stock market has fallen 36% and then come back about 12%!

The scaredy cat who has been spooked by doomsters has $1.5 million, while the long-term investor has $2.5 million. Sure, the scaredy cat has to punt on a crash but that takes risk and insights all connected to timing.

So far, your long-term support for the CBA and stocks over being a scaredy cat in cash has shown you to be pretty damn well smart!

The doomsters do get it right about two to three years out of 10. And really, many of those bad years are simply corrections. Crashes only come along about 9-10 years on average, so the real pay-offs are for the optimists. The optimists and market believers nail it 7-8 years out of 10 and if they go for a diversified portfolio of stocks, with returns close to the overall stock market index, they will net 10% return a year over a 10-year period.

I can live with being criticized two years out of 10 to be right 8 years out of 10. And with my wealth-building curve (the S&P/ASX 200 Index curve) on a rising trend of about 30 degrees (for those who think geometrically), it means you’re better off ignoring doomsday merchants most of the time, unless you want to be a punter.

I prefer the long-term safety of being an investor.

I’d love to always be right, but I’d prefer to be right in the long term, and help someone build their wealth in doing so. If any doomster wants to argue with me on this, I’ll be ungracious, only for today, and simply call them a 24-carat gold dummy!