11 July 2025

1300 794 893

The jobless rate has gone back to a level not seen since the Whitlam days of 1974. With 88,400 jobs created in June, the unemployment rate is now 3.5%. Of course, like then, we now have a Labor Government and it’s particularly relevant that Prime Minister Anthony Albanese draws his party’s inspiration more from other Labor days of Messrs Hawke and Keating, rather than the god-like Gough Whitlam.

While Mr Whitlam had political strengths that made him unforgettable in our history, economics was not one of them. That’s why this jobs figure, which is so good that it screams “look out for inflation and therefore higher interest rates from the Reserve Bank” needs to be both cheered and jeered.

Job creation of this magnitude (total employment hit a record high of 13.6 million in June) has to be cheered. A record high job vacancy number, higher pay packets and rising cost of living pressures are encouraging more workers to look for a job, increase their hours of work, or switch jobs.

This is all great but what we might want to jeer is what it means for interest rates if you’re a home loan borrower with a big debt after buying an overpriced home, or you’re a business owner trying to grow a business and pay wages.

On the other hand, savers (especially retirees) will cheer at the prospect of higher term deposit (TD) rates after nearly a decade of very low rates. These higher TD rates are bound to show up in coming months. That said, if you’re getting 4% on a million, which gives a retiree $40,000 a year to live on but inflation is running at 7% (as some are predicting), that $40,000 buys less because of the inflation effect on the retiree’s purchasing power.

Against that, the retiree would say $40,000 is better than the $10,000 they’ve been getting with TD rates at 1%!

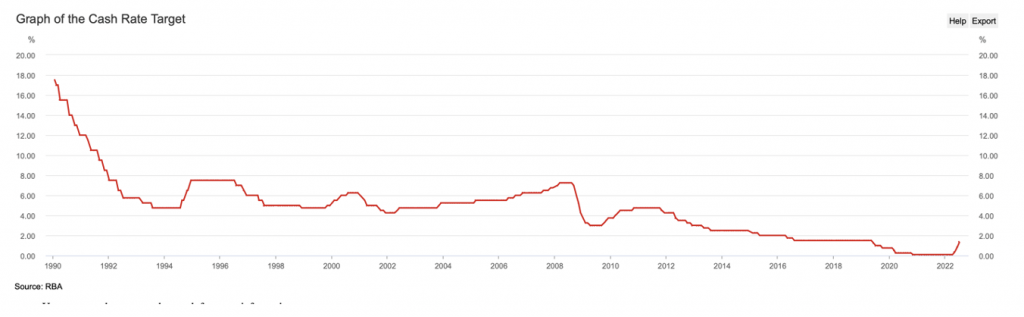

Importantly, if this tight job market that’s driven the unemployment rate down from a low 3.9% in May to 3.5% in June, generates too high inflation readings in coming months, the cash rate of interest will break 2% by year’s end. It will mean home loan rates will rise by 0.65% at a minimum. In all likelihood, I’d be expecting two 0.5% cash rate rises over the months of August and September.

This number tells us to forget a recession any time soon, but it puts the pressure on RBA Governor Dr Phil Lowe to get his interest rate rise plan right.

If he goes too soft, we could end up with Whitlam-style inflation, which was double-digit high. Significantly, this coincided with the OPEC oil crisis that saw inflation peak at, wait for it, 16.4%!

Clearly, Dr Phil wants to avoid this. He’d be keen to dodge the inflation results in the US this week, which came in at 9.1%. Our current inflation rate is 5.1% but a higher one is expected when the next number comes out on July 27, with this tight labour market really putting the pressure on both the inflation figure and Dr Phil’s response with the cash rate.

He does have to go hard for the next two months. I was expecting two 0.5% increases but he might even have to consider a 0.75% hit in August to really scare the pants off us.

But would that work? Over the next two years, it would certainly hurt and hit those overborrowed, who bought a property with record low interest rates. But others who bought and borrowed before might have enjoyed a couple of years on home loan rates of 3% when they borrowed originally at 5% or higher.

They could be sitting on big buffers in their home loan accounts after paying more off their loan in the low pandemic interest rate era or have big savings accounts being a part of those who saved in lockdown. The CBA’s CEO Matt Comyn recently referred to $260 billion of savings in Aussie’s bank accounts, which could make them largely unaffected by rising rates.

In fact, they could end up getting higher interest rates on their savings which could help them spend more!

Our best hope is that the July 27 inflation reading comes in better than expected. However, given the US 9.1% number was so heavily driven by gasoline prices, thanks to the Ukraine war’s impact on oil prices (nearly half of the rise in the month of June) that fall in inflation might have to wait until September quarter’s reading.

So it’s a waiting game, with July 27 a vitally important day for anyone worried about rising interest rates. And while you might be looking for someone to blame and Dr Phil is the obvious suspect, let me argue that interest rates were always going to rise back to normal levels.

The cash rate has been more often than not around 4% or 5%, but the digital era of online selling and disrupting businesses such as Airbnb, Uber and so on has introduced price competition from businesses globally but the pandemic has changed all that, for now.

I’m sure in 2023 inflation will fall when foreign workers and immigrants come back to Australia, the Ukraine war ends and oil prices fall, and China has overcome its pandemic lockdown problems, which will deliver its big supply of products to the world at much lower prices/costs.

But, as I said, it’s a waiting game. Until then, Dr Phil has the tough job of killing inflation without murdering the economy, jobs and consumers, as well as business confidence.

Good luck, Dr Phil!