2 July 2025

1300 794 893

RBA boss Dr Phil Lowe has done it again and raised interest rates by 0.5%, but there’s a growing chorus of economists who are thinking it might be time to pause and let the economic effects of his previous rises sink in. This is set to create a drama over the rest of September ahead of the next meeting of the Reserve Bank board on October 4.

Adding to the plot are very important revelations coming out of the US economy on September 13, with the August inflation reading, followed by the next meeting of the Federal Reserve’s interest rate setting committee on September 21-22.

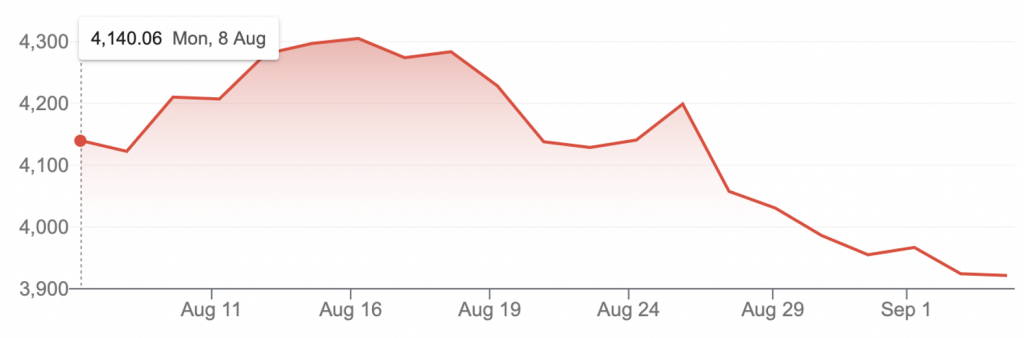

Right now, following the Jackson Hole speech of the Fed’s chairman Jerome Powell two weeks ago, the market was spooked into believing another 0.75% interest rate rise was in store for the Yanks. That has led to the recent sell-off of US stocks, shown in the chart below, which then impacted our share market.

S&P500

That speech took 4.2% off our stock market and we could see more losses if the Fed keeps playing hardball on rates and Dr Phil plays follow the leader.

Some economists think our central bank governor moves in lockstep with Jerome Powell, but if our economic data justifies it, I hope he’s got the good sense and guts to pause on his rate rises (if as I say the data justifies it).

Interestingly, a number of respected economists are posing the question: “Is it time to pause on these rare rises?”

Before the RBA bumped up the cash rate from 1.85% to 2.35% on Tuesday, Coolabah Capital’s Chris Joye tweeted this important point from the CBA economics team: “There is on average a three-month lag between an RBA rate hike and when CBA borrowers on variable rate mortgages experience an increase in their repayments. This explains why official spending data has remained strong but consumer sentiment sits at levels associated with a recession.”

This is the fastest increase in rates since a total increase of 2.75% over five months from August to December 1994. The speed of the rate hikes compared to the last three tightening cycles reflects the extent of the blowout in inflation and the low starting point for the cash rate.

Looking at the fifth rate rise in a row, Dr Shane Oliver of AMP had another take on how monetary policy works: “Given ‘long and variable’ lags in the way monetary tightening impacts the economy, there is a strong case for the RBA to now slow the pace of rate hikes in order to better assess their impact so far. Failure to do so risks recession and overkill in taming inflation.”

Oliver and Joye are looking at the data (which I also pointed to last week), which was showing some pretty notable developments, which suggested these rate rises are biting many aspects of the economy, that could help slow down inflation.

Remember, that’s why the RBA is raising interest rates. Our inflation is 6.1% and this is what the central bank’s economists are predicting: “Inflation is now the highest it has been since the early 1990s and is forecast to increase further in the second half of this year. Consumer price inflation is expected to reach around 7¾ per cent around the end of the year before starting to decline in early 2023.”

This is pure guesswork and no one can convincingly argue that the RBA is a great forecaster, as it once thought interest rates wouldn’t rise until 2024. And they didn’t change that view until early this year!

Shane Oliver is pondering how high the cash rate has to go. That would be a function of him looking at how the data is reacting to the past interest rate rises. “We expect the RBA to so slow the pace of hikes in the months ahead and we will watch Governor Lowe’s speech on Thursday for any guidance in this direction,” he explained. “But it's looking like our assessment for the cash rate to peak at 2.60% around year-end is now too conservative so we have revised it up to 2.85%.”

That said, Oliver and his economists think interest rates will be cut in 2023! I hope he’s wrong because it will imply a recession is happening or is threatening to show up.

Beta Shares chief economist David Bassanese thinks the cash rate will get to 3% sometime in 2023, while many market experts think it will get to 4%, which Bassanese doesn’t think is necessary.

Given we are at 2.35% and we don’t see our next quarterly review of the Consumer Price Index until October 26, the news out of the US on inflation and interest rate rises could be very important to what Dr Phil and his board decide to do on interest rates next month.

Watching the data drama play out will not only be important for those who are overborrowed and are suffering with every interest rate rise (which is undermining the value of the homes these people borrowed for), but also for anyone who doesn’t want to see a recession and would like stock prices to rise.

The point Chris Joye made about the lag between rate rises and when it actually smacks an economy, needs to be thought through by Dr Phil before the next interest rate meeting.

The best news for us would be a nice drop in the US inflation rate next week from the last reading of 8.5% and then Mr Powell opting for a lower rate rise in late September than the expected 0.75% the market is tipping.

Who said economics and statistics are boring? Not me, nor should anyone worrying about their share portfolio, their business or their job!