12 July 2025

1300 794 893

Could we have seen the last of the interest rate misery that has brought 13 rate rises to those now struggling to pay off their mortgage? This was the question that economists like me have had to ask after the October monthly inflation rate came in at a lower-than-expected 4.9% for the past 12 months.

The economics fraternity tipped the number would be 5.2% after it came in at 5.6% in September. And 4.9% compared to 8.4% (the maximum inflation rate we saw last December) looks like real improvement.

I’m someone who has been arguing that the past two rate rises were unnecessary because the mortgage cliff only got serious around June, so this surprise fall is something I’ve been expecting. Furthermore, the CBA economics team thinks there are still a lot of borrowers on low fixed rates who’ll be forced onto high variable rate loans in coming months. When that happens, they’ll be KO’ing their spending big time.

Putting all the above together with this lower-than- expected inflation reading, it’s reasonable to think that rate rises could be over.

By the way, I’m not alone in believing it makes sense for the RBA to ease up on rate rises. The AFR has reported that the Paris-based think tank, the Organisation for Economic Co-operation and Development (or OECD) says we’ve seen the top of the cash rate at 4.35%. These guys have calculated that our economy will dodges a recession but overall economic growth for 2024 will come in at 1.4% after chugging along at 1.9% this year.

To see why we miss out on a serious slowdown, this observation from the OECD puts China and overseas students into perspective: “Continued strong working-age population growth and higher exports as foreign student arrivals further recover will partly offset these headwinds.”

For those praying for rate cuts, the OECD crystal ball says that in the third quarter (July to September) we should see the cash rate fall and it will probably stop around 3.6%.

They’re talking about a 0.75% fall, which would be seen as a great relief for those who’ve borrowed heavily to get into the expensive housing market.

Of course, the next monthly reading for December, which comes out on 1 January and then the December quarterly figure out on 31 January will determine if this nice fall in October is the start of another leg down.

Helping this cause is the rise in the Oz dollar, which helps make imports cheaper and also lowers the overall inflation rate.

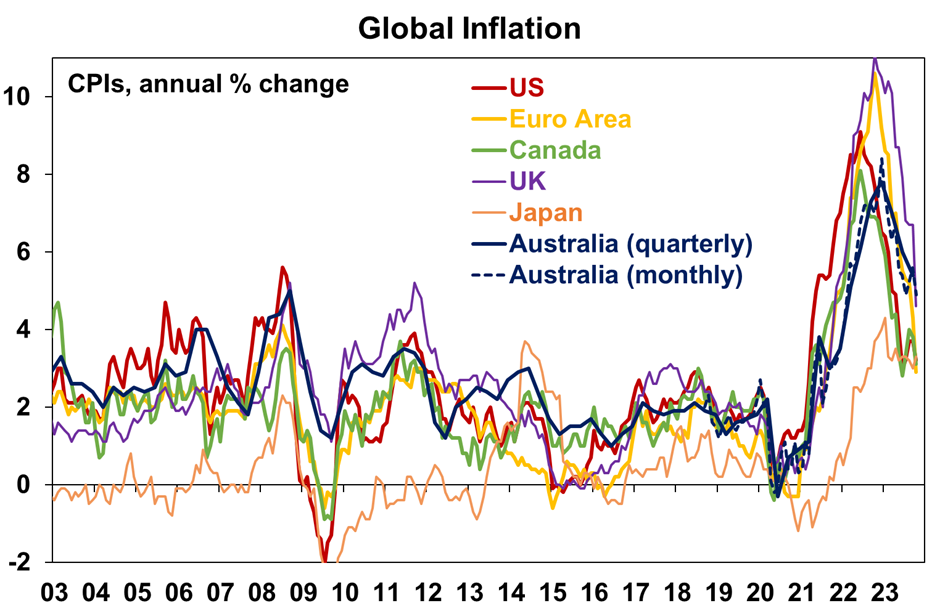

By the way, it has been pointed out that our inflation fall isn’t as good as many of the Western economies we compare ourselves to, but I like AMP’s Diana Mousina’s take on the subject. “Much has been said around higher Australian inflation data relative to our global peers (see the chart below),” she wrote this week. “However, Australian inflation peaked approximately 6 months after our major peers, so it’s only natural that the decline in inflation is also occurring later than our peers. We expect that inflation will fall faster than the RBA is forecasting over the next six months.”

Also slowing up the impact of rare rises on inflation was the record high percentage of 40% of borrowers who were enticed on to low fixed rate loans, which meant many borrowers were unaffected by the rate rises. Historically, only 15% of borrowers were on fixed rate loans, so when the RBA raised rates there was a much bigger bang for its buck.

The pandemic and what it did to the cash rate made the RBA and monetary policy less effective, but it looks like reality is starting to bite.